On the uncertainty of the neutral interest rate

The neutral interest rate is a key indicator for the orientation of monetary policy, the evolution of the financial markets and, in general, the formation of economic agents’ expectations. We delve into its definition and the level at which it stands today.

The intensification of inflationary pressures, in the context of COVID-19 and Russia’s invasion of Ukraine, has resulted in the sharpest tightening of monetary policy seen in advanced economies since the 1980s, with official rate hikes of around 300 bps and the cessation of net asset purchase programmes.

Despite what has already been announced, the truth is that there is still a lot of uncertainty surrounding what level official rates will settle at, both in the current cycle of rate hikes and in the long term. In the euro area, the ECB has stated that it will continue to raise official rates until they are in «restrictive territory», that is, above the level which would neither stimulate nor contract the economy, or the neutral rate, as it is usually called. In the US, meanwhile, it is estimated that official rates are already at these restrictive levels, and the Fed is expected to continue to raise them in the coming months, albeit at a slower pace.

Given the important role it plays in the financial markets and in the economy in general, in this Focus we pose the question: what is this so-called neutral rate and at what level does it lie?

According to economic theory, the neutral interest rate is that which balances an economy’s aggregate demand with its aggregate supply. Put in other words, it is the interest rate set by the central bank which would allow the economy to operate at full employment and with price stability.

Delving deeper into this definition, it is worth pointing out that price stability is usually associated with inflation fluctuating at around 2.0% year-on-year, according to the statutes of advanced countries’ central banks. In addition, achieving full employment would require using all the resources available in the economy, which in other words means that GDP would grow in accordance with its long-term potential rate and the output gap would be non-existent.

Thus, the definition of the neutral interest rate is closely linked to each economy’s productive capacity and, therefore, to the evolution of the factors of production (such as labour, capital and technological progress) which determine potential growth.1 Thus, countries with a higher potential growth (e.g. due to greater technological innovation or more favourable demographic dynamics) can be expected to have a higher neutral rate.

However, unlike other macroeconomic variables, potential GDP and, therefore, the neutral interest rate are not observable, so they have to be estimated. For the US, the median FOMC voter places the neutral (nominal) rate at around 2.5%, albeit with an estimate range between 2.3% and 3.3%, according to the latest forecasts in the dot plot.2 The implicit rates in the money markets, meanwhile, reflect a (nominal) rate converging towards 3.0% in the long run. However, these estimates are slightly lower than the rate suggested by a model used by the New York Fed, known as the Holston-Laubach-Williams (HLW) model, which allows short-term fluctuations in the real neutral rate to be captured.3 Using the open-source code of this model,4 we estimate that the real neutral rate in the US ended Q3 2022 at 1.4%, which would be compatible with a nominal equilibrium rate of around 3.5% (see first chart).

- 1. For further information on potential GDP and its determining factors, see the article «Potential GDP and the output gap: what do they measure and what do they depend on?» in the Dossier of the MR05/2013.

- 2. See the «Summary of Economic Projections» of December 2022.

- 3. This model uses a Kalman filter based on estimates of potential growth and of the output gap. The model uses quarterly series of real GDP, core inflation and monetary interest rates as a starting point. For further details, see K. Holston, T. Laubach and J. Williams (2017). «Measuring the Natural Rate of Interest: International Trends and Determinants». Journal of International Economics.

- 4. See https://www.newyorkfed.org/research/policy/rstar.

For the euro area, meanwhile, the members of the ECB have alluded to estimates of a neutral (nominal) rate of around 2.0%, although its president Christine Lagarde herself has warned about the high level of uncertainty involved in estimating it. Indeed, some voices within the Governing Council have pointed out that the neutral rate is likely to have increased this year, reflecting a positive output gap in the face of the imbalance between demand and supply against the backdrop of the war in Ukraine. In this regard, the implicit rates in the money markets reflect a long-term nominal rate converging at around 2.5%.

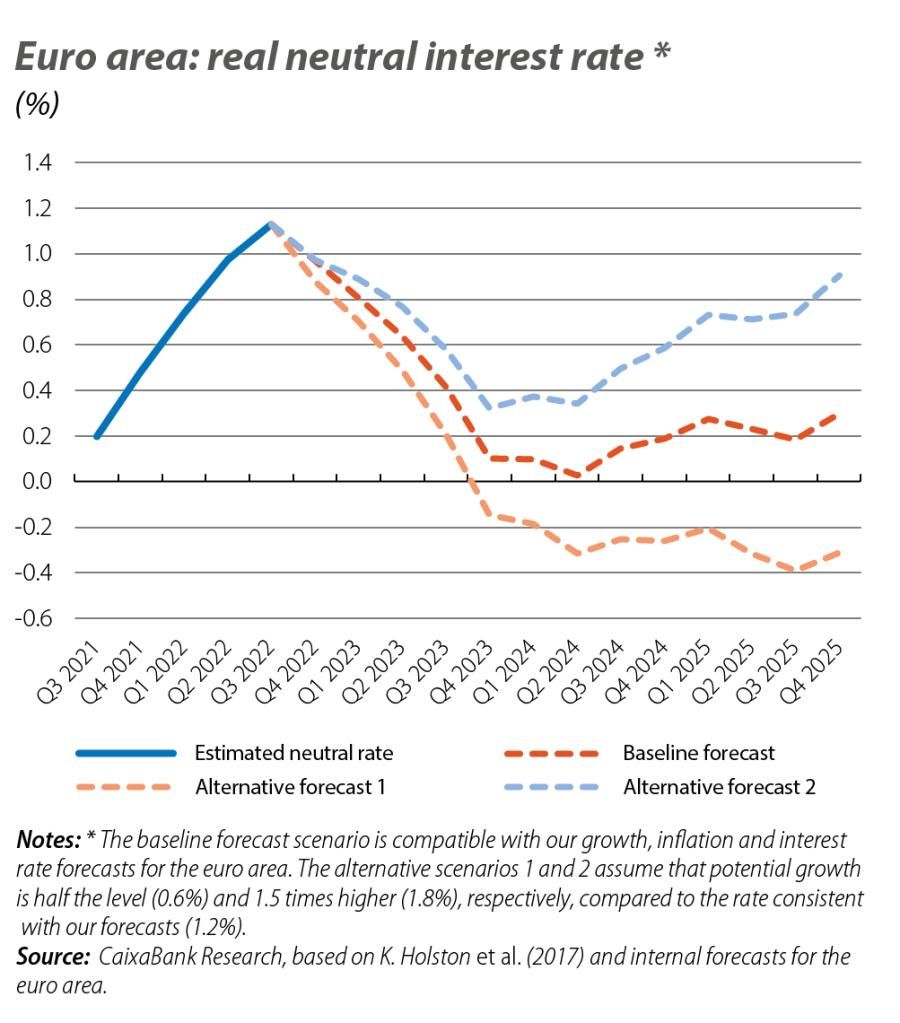

To test this hypothesis, we replicated the HLW model for the euro area, based on the algorithm published by the Fed. The model suggests that the real neutral rate in the euro area has risen from approximately 0.0% in the run-up to the pandemic to 1.0% in Q3 2022 (see first chart), which is consistent with a nominal equilibrium rate of 3.0%. According to this model, the output gap in the euro area economy has been widening, reaching around 3.0% of potential GDP in Q3 2022, its highest level since the beginning of the series (1972).

As its authors themselves point out, the usefulness of the HLW model is based on its ability to estimate the real neutral rate that would be necessary to balance aggregate supply and demand in a given period. In other words, it can be used to estimate the real interest rate at which, in theory, GDP would operate at its potential (output gap = 0) and with price stability.

However, rather than operating according to their potential, economies tend to fluctuate according to the business cycle, with periods in which their unused capacity is absorbed and they grow above potential, and others where the opposite occurs. In this regard, a relatively high estimated neutral rate for the US and the euro area this year is an indication of the interest rate that is required in order to resolve the current mismatch between supply and demand and thus curb the upward pressure on prices. It should come as no surprise that, in this context, the central banks have decided to raise rates so abruptly.

However, while these estimates are particularly useful for understanding monetary policy measures in the current context, the fact is that in such volatile times they are not indicative of the long-term equilibrium interest rate, once economic growth converges on its potential. In fact, if we extend the estimates using our forecasts for the euro area (for growth, inflation and interest rates), the model suggests that the real equilibrium rate would converge to the 0.0%-0.5% range, that is, between 2.0% and 2.5% in nominal terms.

The key factor in these estimates is what is assumed about the evolution of potential growth, and this, in turn, incorporates assumptions about the labour force (demography and participation in the labour market), the stock of capital (and, therefore, investment) and technological innovation, among other factors. Thus, in an alternative scenario in which potential growth is half that of our baseline forecast (0.6% versus 1.2%), for instance due to a permanent destruction in physical capital or a structurally lower labour participation rate, the real neutral rate would lie at around –0.3%, or 1.7% in nominal terms. In contrast, with a potential growth 1.5 times higher (1.8% versus 1.2%), as a result, for example, of more rapid technological development or more profound structural reforms, the neutral rate would be higher (see second chart).

In short, the neutral interest rate is a key indicator for the orientation of monetary policy, the evolution of the financial markets and, in general, the formation of economic agents’ expectations. Estimating it, however, is subject to great uncertainty, linked, among many other factors, to assumptions about the evolution of each economy’s productive capacity. Today, the current economic environment has caused the neutral rate to be higher than has been observed in recent years. Looking further ahead, however, the level at which these rates converge will depend on how optimistic one is about the outlook and the structure of growth in the long term.