A promising summer harvest for Spain’s tourism

The situation in the tourism sector improved considerably during the summer season. Vaccinations have represented a clear turning point, leading to the lifting of restrictions and the recovery of travel in Europe, as well as keeping the pandemic under control. The indicators for demand, supply and even prices confirm a radical change in the situation, not only in Spain but also in the countries around us. This good summer harvest encourages us to be optimistic about the coming months, when we expect to see a consolidation in the recovery that should ensure 2022 will once again be a good year for Spain’s tourism industry.

Higher tourist demand in the summer months

The situation of the tourism sector improved considerably during the summer months, outperforming the projections of many of the companies in the sector. The vaccination of the population at risk, the implementation of the EU Digital COVID Certificate, the large pent-up demand for tourism and easing of restrictions for the hospitality industry have been the compendium of factors that have supported this significant and necessary recovery for the sector. However, among the factors mentioned above, the one we believe has been most crucial is vaccination, as this has minimised the number of severe cases of COVID-19, helping to relieve the pressure on the healthcare system. This not only opened the door to a recovery during the summer season but has also laid the foundations for travel to get back to normal in the medium term, as predicted.

All the indicators show a clear turning point in the second quarter of the year, coinciding with the end of the state of emergency at the beginning of May. This led to the restrictions on travel between regions and curfews being lifted in almost all the autonomous regions except for the Balearic Islands, Valencia and Basque Country, where they were kept in place for a few weeks longer. This turning point was further supported in July with the approval of the Digital COVID Certificate, which boosted travel by international visitors to Spain. As a result, in July and August, the most important months of the year for the sector, tourism demand was much more dynamic than in the summer season of 2020. Even so, international and domestic overnight stays by tourists were 27% lower than the same period in 2019.

Tourism demand indicators show a clear turning point in Q2 2021 with the end of the state of emergency. The traditional destinations for Spanish tourists managed to recover their pre-COVID level of activity in August thanks to the excellent performance by domestic tourism

This improvement in the figures was down to the extraordinary performance by domestic tourism demand, which reached a level 11% higher than that recorded in the months of July and August 2019, as shown in the chart below. The reason was captive demand: a large number of Spanish tourists who usually travel abroad on their holidays opted for national destinations that were closer, safer and with fewer travel complications.1 International demand continued to be sluggish, although it picked up appreciably between May (when foreign overnight stays were 90% lower than the same month in 2019) and August (down by 48% compared with August 2019). Across the different source markets, tourism originating from the EU performed relatively better (–37% compared with August 2019), while non-EU tourist arrivals remained very moderate (–69%).

- 1According to the most recent figures from the resident tourism survey (FAMILITUR) by the National Statistics Institute, only 10% of the expenditure by Spanish residents was made abroad last June, compared with 32% in June 2019.

At a regional level, the situation is very disparate due to big differences between autonomous communities in terms of their dependence on international tourism, whose level of activity is still moderate compared with the marked recovery in domestic tourism. Consequently, the traditional destinations for domestic tourism, such as Asturias, Cantabria and the Region of Murcia, achieved levels of activity that are very close and in some cases higher than those recorded in the summer of 2019. On the other hand, those communities more focused on international tourism, such as the Balearic Islands, Canary Islands and Catalonia, also improved their levels of activity but are still far from their pre-COVID levels. Nevertheless, one common feature of those regions most dependent on international tourism has been their ability to attract a larger volume of domestic tourism, in some cases growing by more than 20%.

Tourist overnight stays in the autonomous regions in August 2021

Change compared with August 2019

Flight departures and arrivals registered in Mediterranean destinations

Change compared with the same period in 2019

The recovery in tourism has not only occurred in Spain; it has been widespread in all the markets of the Mediterranean basin, including countries outside the EU. This is confirmed by our analysis of high-frequency flight data, which aggregates domestic and international operations and helps us to estimate tourist movements. As can be seen in the chart, the most successful cases this summer were those of Greece and Croatia, recording a similar level of air travel in August 2021 as the same month in 2019, thanks to the fact that the country opted very early for an open policy, eliminating restrictions on travel and hospitality even before the Digital COVID Certificate was approved. Meanwhile, the more traditional markets such as France, Spain, Italy and Portugal recorded similar air traffic levels, with drops in August of around 25% compared with the same month in 2019. Finally, Morocco and Turkey performed particularly well. These two countries, non-EU but traditionally receiving European tourism, managed to recover a large part of their activity thanks to their decision to accept the Digital COVID Certificate for the entry of European tourists, together with the fact that they have achieved relatively high vaccination rates (over 50% of their populations have been completely vaccinated).

Reactivation of Spain’s hotel industry

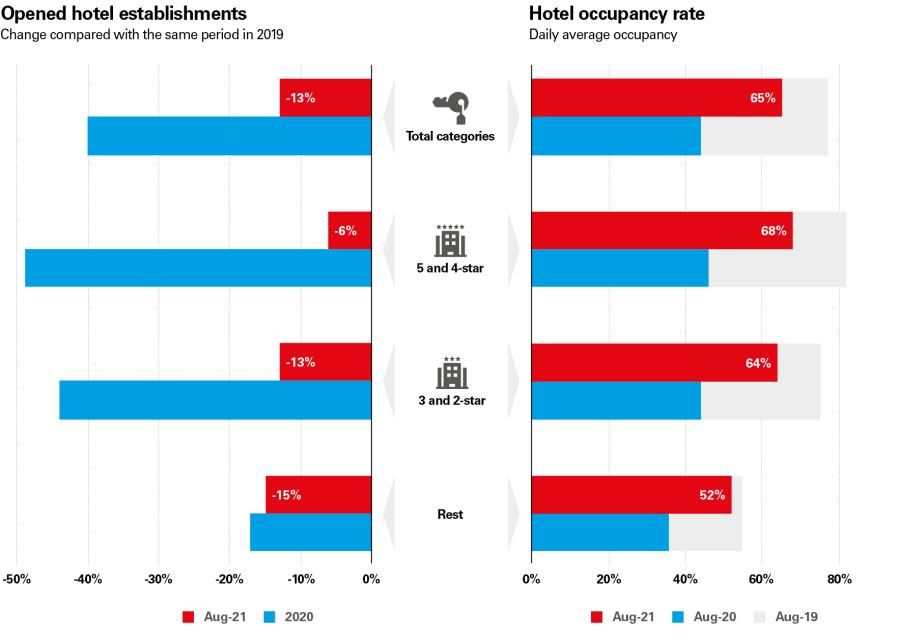

Spain’s good demand figures have been accompanied by a significant decrease in the number of tourism businesses remaining inactive or closed, especially in the hotel sector, one of the hardest hit by closures during 2020. According to hotel occupancy survey data, 13% fewer hotel establishments were open in August 2021 than in August 2019, which implies a very strong recovery when compared with the 40% drop in the number of open establishments on average in 2020. Despite the fact that the best figures are widespread, there are important different across hotel categories.

The higher category hotels (5 and 4-star), which include a larger number of more personalised services, managed to get back to a level of activity similar to 2019, with just 6% fewer establishments open last August. In addition, the occupancy rate for superior hotels was 68% in August, a rate similar to the one recorded in June and September 2019 (although far from the 82% achieved in August 2019), indicating that occupancy did not particularly suffer in spite of the large number of establishments reopening.

The number of open hotels has gone from falling by 40% in 2020 to just 13% lower this August compared with the same month in 2019. Superior hotels have returned to a similar level of activity as in 2019

On the other hand, the recovery was not so buoyant in the lower category hotels, more focused on purely accommodation services. As can be seen in the chart, the number of intermediate category hotels (3 and 2-star) open in August was 13% lower than in the same month of 2019, while the figure for the rest of the hotel establishments (1-star and hostels) was 15% lower. Nevertheless, occupancy rates for these establishments reached relatively high levels, suggesting that those establishments that were open managed to do good business. Specifically, in the case of intermediate category hotels, the occupancy rate was far from the one posted in August 2019 but very similar to the performance of June and September 2019, while the occupancy rate for the rest of the hotel establishments was very similar to the rate in August 2019.

Hotel business indicators

The recovery in tourism prices, crucial for the recovery of the tourism industry

In addition to demand and activity, the recovery of the tourism industry also involves the recovery of prices, which in 2020 saw very sharp adjustments across virtually all related sectors of activity except hospitality. These adjustments, which attempted to boost demand but without any great success, undermined the tourism sector’s revenue-generating capacity.2 However, we could also say that what demand takes away with one hand, it gives back with the other.

The recovery in travel and consequent improvement in tourist flows prompted many tourism businesses (mainly hotels, the sector that was hardest hit in 2020) to get back to price levels more similar to those of 2019. As can be seen in the chart, this August the ADR3was 5.2% higher than the same month in 2019. The explanation for this upturn could be solely the fact that more premium establishments, whose prices are higher, have reopened, leading to an «artificial» rise in the average price published by the National Statistics Institute. This is not the case, however, as hotel prices increased compared with August 2019 across almost all hotel categories, especially in the cases of 5-star (+10.9%) and 3-star (+6.2%).

Looking at other activities that make up the tourism value chain, the results are very heterogeneous. According to data from the National Statistics Institute’s consumer price index, the catering sector as a whole has not adjusted its prices at any time since the COVID-19 pandemic started. This may be due to the fact that the catering sector, when not affected by the restrictions, has been more than able to replace tourist demand with local demand without the need to appreciably adjust its prices. On the other hand, the air transport sector still carries out a remarkable price adjustment since the beginning of the pandemic; in the case of international flights, the prices charged this August were 15% lower than in the same month of 2019.

What big data can tell us about the state of the tourism industry

Given the changing and uncertain nature of the current situation, it’s becoming increasingly important to be able to carry out analyses with large databases that provide information in real time. Consequently, at CaixaBank Research we study card payments made via CaixaBank point-of-sale (POS) terminals using big data methodology in order to develop real-time, highly granular indicators for tourist spending.

Looking at the CaixaBank POS card usage indicator by branch of activity, shown in the chart below, the main conclusion of the official statistics previously analysed in this Report is confirmed: consumption at tourism establishments improved considerably during the summer months. However, thanks to both the temporal and sectoral granularity of the indicator, some nuances can be found.

Real-time analysis of CaixaBank’s internal data confirms that the recovery during the summer occurred in all branches of tourism activity, albeit with some disparity based on card payments

In terms of spending on accommodation (hotels, campsites and similar), consumption rocketed in August, reaching a level 6% higher than in August 2019.4 Much of this improvement was a consequence of the strong recovery in spending via Spanish cards (i.e. domestic tourism), exceeding the expenditure recorded in August 2019 by more than 50%. However, spending returned to negative figures in September, standing 16% below the 2019 level. This may be due to the fact that the recovery in holiday tourism, very predominant in August but somewhat less so in September, is moving at a faster pace than the recovery in leisure tourism or weekend trips.5 Nevertheless, we still believe the upward trend in tourist accommodation business is very robust.

The data also reveal that the restaurant sector has managed to weather the difficult situation experienced during the first quarter of the year. In fact, since May card payments in restaurants are comfortably above the level of the same period in 2019, which suggests that, since May: (i) a large pent-up demand for this type of consumption has been released (spending via Spanish cards in restaurants increased by more than 50% in some weeks in August), accumulated over a long period of restrictions, and (ii) the sector has shown a great capacity to adapt and make the most of outdoor terrace space given the relatively strict indoor limitations.

The rising trend is clear for the rest of the businesses linked to tourism, although the extent of the rise varies greatly, as shown in the chart below. Of note is the case of payments to travel agencies which, despite the improvement recorded since the first few months of the year, remained very low during the summer season, posting falls close to 60% compared with the same period in 2019.

- 4It should be noted that the consumption indicator based on CaixaBank POS card payments suggests a more positive trend in consumption than that indicated by real consumption, due to the effect of the greater use of cards as a means of payment following the outbreak of COVID-19. For example, according to the turnover data published by the National Statistics Institute for July, accommodation and restaurants recorded, respectively, a drop of 32% and 20% compared with July 2019 while, over the same period, CaixaBank POS payments for accommodation fell by 26% and restaurants rose by 24%.

- 5In this case, holiday tourism would be related to the season for tourists who are on holiday from their work, usually characterised by higher-range trips and longer stays. On the other hand, leisure tourism would be associated with weekend trips, of a lower range, less regular and shorter.

Another extremely important point to understand the situation, and for which we can use CaixaBank’s internal data, is the analysis of the source markets for Spain’s tourism. This summer, the different recommendations, restrictions and controls imposed on tourists who wanted to visit Spain have determined part of the tourist demand. A very clear case of the effect of restrictions during the summer season has been that of the United Kingdom. Britain only lifted its restrictions on travelling to Spain in July for tourists who had been completely vaccinated and also had to present a negative PCR test before they returned to the UK, carried out maximum 72 hours before their arrival, and another negative PCR test after arriving. This limitation meant that visits by British tourists to Spain took much longer to recover, pushing those people who were more impatient to plan their holidays to look for alternative destinations, including "staycations". On the other hand is the case of the EU countries that opted to allow travel supported by the use of Digital COVID Certificate, a homogeneous system, very simple and easy to use, applied throughout the EU which has helped intra-EU tourism to rebound quickly.

Domestic tourism and source markets in the EU have been the major supports for the recovery in Spain’s tourism sector this summer

CaixaBank’s POS card payment data also give us a broad and up-to-date overview of all the source markets for tourists visiting Spain. Depending on the source market, as can be seen in the table below, there are four different rates of recovery:

- Domestic tourism accelerated sharply after the end of the state of emergency in the first week of May.

- EU source markets saw their card expenditure achieve levels close to those recorded in the same period in 2019, even exceeding this in some cases. The exception was Italy, which decided to encourage domestic tourism, as it did in 2020, using a tourist voucher scheme.

- At a third level, we can see the UK, along with the US, Canada and Latin America. The UK recovery is slower than expected due to the restrictions imposed until well into July. In contrast, US markets are recovering faster than expected, with tourist card expenditure in September around 25% lower than in the same month of 2019.

- Finally, there is Russia and the Asian source markets, grouped under the heading «Rest of the world» along with the rest of the smaller source markets. For these countries, the recovery is still considerably weak as a result of the severe travel restrictions still in place.

Tourist card expenditure by country of origin*

Change compared with the same period in 2019

From an analysis of payment card data, we can discern that the recovery in international tourism during the summer was mainly supported by domestic tourism and EU source markets. Moreover, the upward trend in the UK and Americas supports the hypothesis that the path to a more widespread recovery in the coming months will be conditioned by the recovery in these mid-range markets, given that the scope for improvement via EU tourist arrivals is more limited.

To test this hypothesis, we studied the interest of international tourists in travelling to Spain by analysing travel-related searches on Google containing the word «Spain», carried out in six source countries. In our analysis, we compared the number of searches carried out with a baseline defined as the number of searches that would be expected in a normal pre-pandemic year. As can be seen in the chart, tourists from the Netherlands and Germany are the most interested in travelling to Spain, in line with our card data, with a search volume 32% and 50% above the baseline, respectively. Searches from the UK are in slightly positive terrain (+6.2%), which would suggest they could potentially recover in what remains of the year. Searches from the US have remained 20-25% below the baseline since August, which may indicate that the potential for improvement in the US is not so high and may be affected by the recent rise in severe cases of COVID-19 in the country, blamed on the Delta variant.

Weekly searches in Google for trips to Spain

Deviation from the baseline level* or expected searches

CaixaBank Research forecasts for the tourism industry in Spain

Our analysis of all the indicators, both official and internal, has led us to construct a relatively positive forecast scenario for the remainder of the year and for 2022. We expect international tourism expenditure to continue improving gradually over the remainder of 2021 and end the year up 70% year-on-year; i.e. at 36% of 2019’s level. In terms of domestic tourism expenditure, we expect pre-COVID levels to be maintained for the rest of the year, with spending growing by 50% year-on-year, reaching 84% of the level in 2019. However, the degree of uncertainty surrounding our projections remains very high due to the potential risks associated with new vaccine-resistant variants of COVID-19.

Looking ahead to 2022, we expect international tourism expenditure to double to around 79% of the level of spending seen in 2019. In this scenario, we envisage that, together with the normalisation of EU tourism, a key factor will also be the recovery in the UK market, with a large pent-up demand also generated in 2021, and in the Americas, mainly the US and Canada, which will boost demand, thereby continuing to support the recovery in international tourism. As far as domestic tourism is concerned, we expect captive demand to continue keeping Spanish tourism expenditure at similar levels to 2019, which would take annual domestic tourism expenditure to slightly above its pre-COVID level (3% higher).

Tourist expenditure in Spain

Change compared with the same quarter in 2019

In terms of tourism-related GDP, the indicator that measures the total economic activity generated by the tourism sector, we expect this to stand at 54% of the 2019 level in 2021 and to grow by 55% annually. However, as can be seen in the data published up to September, it is worth noting the big difference between the business carried out in the first half of the year, at 27% of the 2019 level, and that forecast for the second half of the year, namely 74%. In other words, the annual activity figure for 2021 will be relatively subdued due solely to the poor performance in the first half of the year.

Our forecast scenario for the remainder of the year and for 2022 is relatively positive: we expect tourism GDP to pick up strongly and grow by 55% in 2021 and 57% in 2022

As far as 2022 is concerned, the good figures for domestic and EU tourism are expected to consolidate. This, together with the gradual recovery in the British and American source markets should result in a progressive improvement in activity throughout the year. We therefore expect tourism GDP to reach 88% of the level recorded in 2019, up by 63% annually. While our tourism GDP projections for 2022 will be very positive for the sector (it will be between the level reached in 2016 and 2017), we still expect an appreciable gap compared with its performance in 2019. This will be due to a still very incomplete recovery of long-range and less traditional tourism. We also expect business tourism (8.2% of total tourism expenditure), which has been somewhat more resilient than its holiday and leisure counterparts during 2021, to improve more gradually during 2021 due to the impact of the digital transformation witnessed during the pandemic, which has reduced physical attendance at meetings and conferences.

With this outlook, we expect 2022 to be a profitable year for a vast majority of the sector, placing the long-term sustainability of the tourism industry beyond doubt. Nevertheless, it’s important to stress the important role that will be played by economic policy over the coming months, which must continue to adapt responsively and effectively. We believe the recent extension of the furlough scheme to be crucial, given the more positive but, judging by the evolution of the pandemic at a global level, still unstable situation. Additionally, the Solvency Support Fund for Strategic Enterprises, managed by SEPI and totalling 10 billion euros of which 1.08 billion have already been allocated, continues to be very important for the stability of key tourist businesses, as in the case of Globalia and Avoris. Finally, the Next Generation EU (NGEU) funds will also be important when it comes to supporting improvements in digitalisation, sustainability and infrastructures, investments which are currently difficult to undertake for a hard-hit tourism industry but vital in order to survive this crisis whilst also maintaining our status as the most competitive tourist destination in the world.