An unusually placid summer in the financial markets

The economic revival rekindles risk appetite

In a context of a revival of economic activity and support for the recovery from economic policies on the one hand, but with the emergence of new outbreaks of COVID-19 and a moderation in the improvement in mobility on the other, during the course of July and August investor sentiment was generally optimistic and led to a relatively calm summer in the financial markets. The recovery in risk appetite favoured the performance of risky assets (with widespread gains in the stock markets, a recovery in commodity prices and a reduction in both sovereign and corporate risk premiums), and it also reduced the pressure that safe-haven assets had endured with the outbreak of the pandemic (such as the US dollar, which appreciated significantly in the spring, or US and German sovereign bonds). However, in the closing days of August and with the holiday season coming to a close, investor sentiment became more cautious and susceptible to news of new cases of COVID-19, and there were several sessions of volatility and setbacks among risky assets.

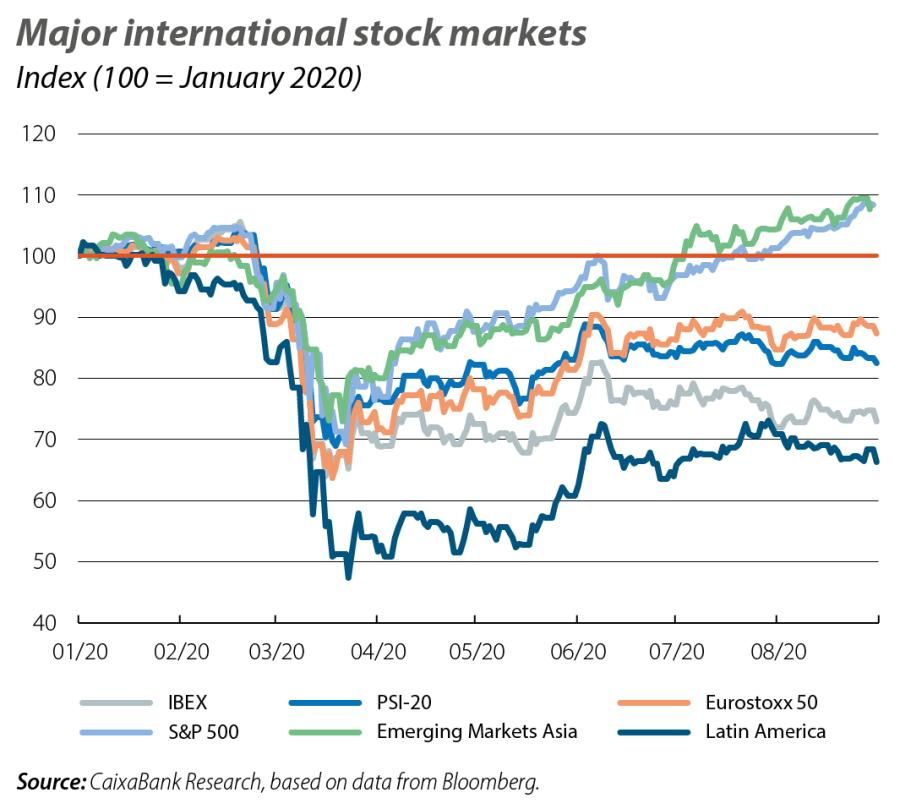

Stock markets on the rise, especially in the US, where pre-pandemic levels were recovered

Investors’ optimistic tone was well reflected in the widespread recovery of the major global stock markets throughout July and August. In general, the improvement was led by sectors more sensitive to the business cycle, while, by region, significant gains were registered in China (where economic activity has rebounded significantly) and the US (favoured by the stock prices of technology and e-commerce companies). In both countries, the trading floors closed August having comfortably exceeded pre-pandemic levels and registering new highs for the year. By contrast, while stock market gains were also registered in Europe as a whole, at the end of August they showed more disparity and still amassed significant losses compared to the end of 2019. At one extreme, the decline of the Spanish Ibex 35 index since the beginning of the year was close to –30%, while at the other, the German DAX ended August just 2% below its 2019 close. In the middle of the spectrum, losses still accumulated in Italy, France and Portugal at the end of August stood at around –15%. Similarly, emerging markets experienced a general upward trend, but performed much better in Asia (MSCI index +12.5% since the end of June and +7.2% in the year to date) than in Latin America (+3.7% and –33.7%, respectively). Among the more fragile emerging markets, meanwhile, Turkish stock prices performed particularly poorly (Istanbul stock market –7.4% in July-August as a whole).

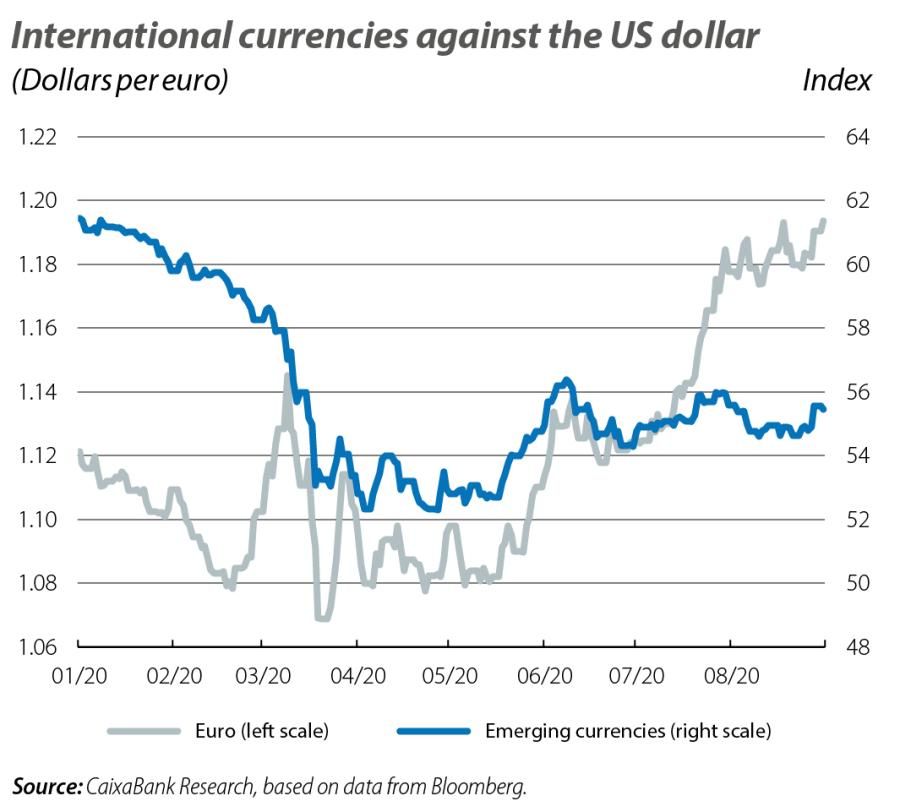

Currencies recover against the dollar

With the notable exception of the Turkish lira (which depreciated by around 7% compared to the end of June), the overall tone of the currency markets was positive and the improvement in sentiment led to a recovery of most currencies against the US dollar. This advance was widespread among emerging-economy currencies, albeit relatively moderate, while advanced-economy currencies registered a sharp appreciation (euro +6%, pound sterling +8% and Japanese yen +2%). In fact, while these advanced currencies were at annual highs, at the end of August emerging currencies were still well below their rates of the beginning of the year.

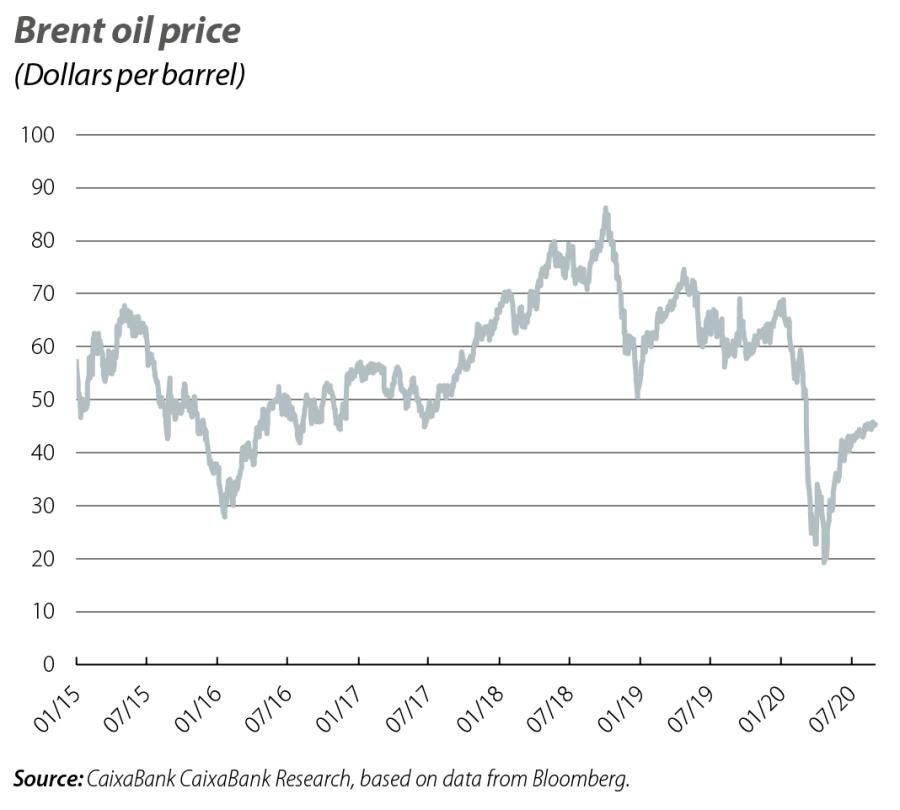

The improvement in sentiment boosts commodity prices

In the same vein, the commodity markets experienced a widespread recovery in prices over the summer, both in the case of energy commodities and among agricultural products and metals. In the oil market, the barrel of Brent also benefited from the cuts by OPEC and its allies (as agreed, in order to accommodate the global economy’s recovery, in August the cuts were relaxed from 9.7 million barrels a day to 7.7 million) and its price rose to around 45 dollars. Furthermore, in combination with the revival in demand, accumulated oil inventories have begun to decline. Nevertheless, they still remain high (for instance, in the US they remain 15% above the average for the last five years) and should serve to cushion any potential spikes in demand and thus mitigate their impact on prices.

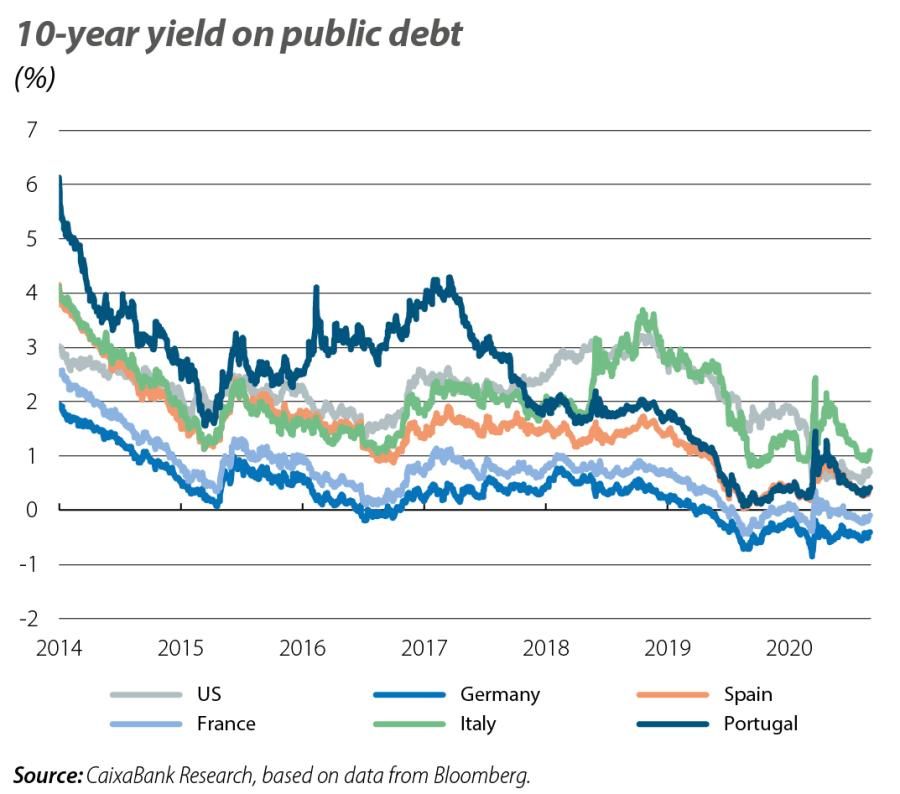

Interest rates remain anchored at low levels

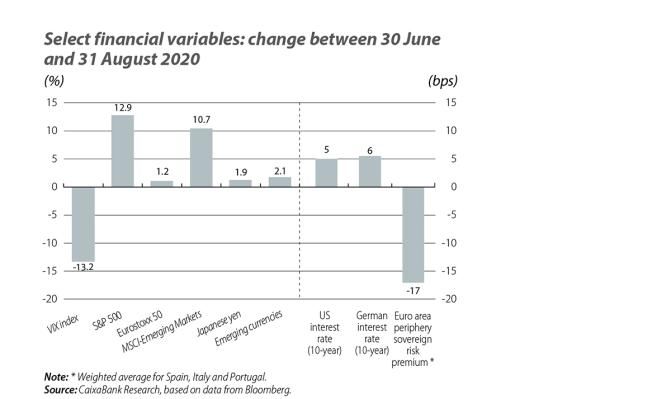

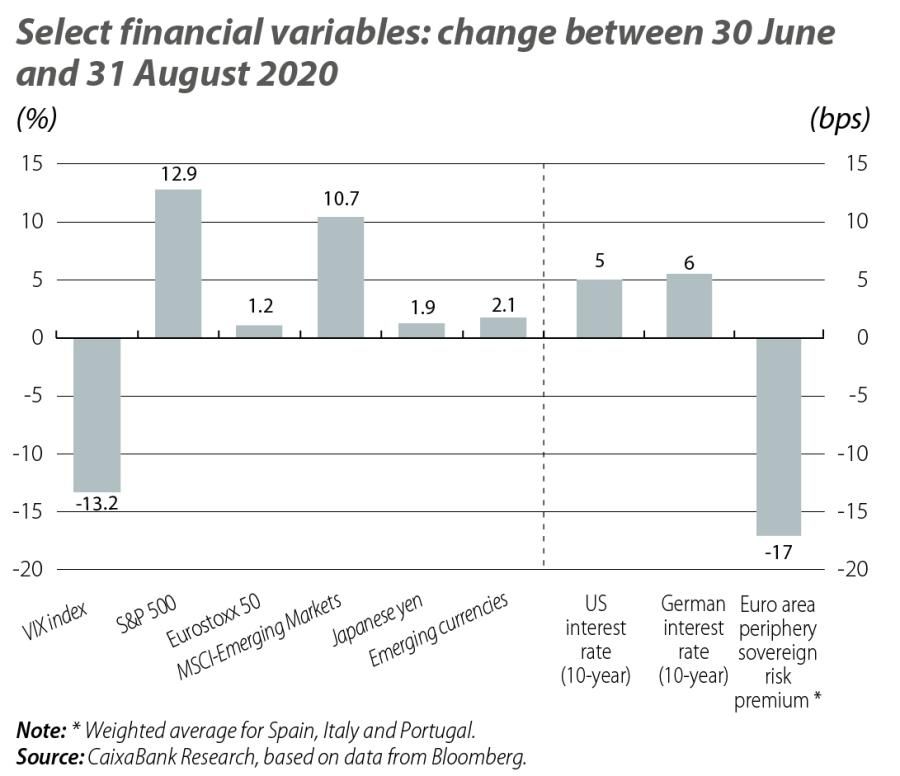

The improvement in risk appetite led to a certain recovery in the yields of «safer» sovereign debt, such as that of the US and Germany, and the yield curves became somewhat steeper. In any case, interest rates remain well below their levels of the beginning of the year (US and German 10-year yields closed August 122 and 21 bps below their 2019 year-end levels, respectively). Furthermore, euro area risk premiums continued to narrow and approached their low point for the year to date (in spring they had surged by more than 90 and 110 bps in Spain and Portugal, respectively, and by around 150 bps in Italy).

Monetary policy locks in accommodative financial conditions

The expectations implicit in the low market interest rates point towards a long period of dovish monetary policy (at the end of August, implicit rates did not price in any rate movements from the Fed before 2023 or any from the ECB before 2024). Indeed, after stabilising the financial environment, at their July meetings the major central banks did not change their monetary policy, but rather reiterated that it must be very accommodative in order to support the economic recovery. Thus, while no significant announcements are expected at their September meetings given the scale of the measures already implemented, both the Fed and the ECB reminded the markets that they are prepared to redouble their efforts if the economy should need it. For the time being, however, the central banks have parked their role as «fire-fighters» and have set their sights on longer-term goals. A sign of this was the fact that, at the end of August, the Fed announced a recalibration of its long-term objectives and of the strategic framework that governs its monetary policy. On the one hand, the Fed will pursue an inflation rate of 2% on average over time, meaning that it will tolerate periods of inflation slightly above 2% if they are preceded by periods with figures slightly below 2%. On the other hand, from now on it will assess the labour market from an asymmetrical perspective: in terms of shortfalls from maximum employment (to date, it had done so in terms of deviations, which could be either down or up). It also emphasises the importance of adopting an «inclusive» approach when considering maximum employment. In the current context, all of this suggests that the Fed will keep rates low for longer than it would have done under its previous strategic framework.