What's happening in Europe's property market?

The European real estate market has seen several years of strong growth. In fact, since early 2016, house prices in the EU have risen by 4.6% year-on-year on average, outperforming wages and GDP growth. This upward trend has been widespread across countries and also large cities. This article examines the factors underpinning this trend and whether it poses any risks.

House prices have risen markedly across all European countries bar Italy and have now exceed pre-crisis levels in most cases, while some countries prices are growing well above the EU average. This is the case of Hungary and Portugal, where prices have risen by more than 9.0% year-on-year on average since 2016.

House prices have risen considerably in European countries

Cumulative change between Q1 2016 and Q2 2019 (%)

In part, the rise of house prices in Europe is due to a synchronised economic recovery. The european recovery began in 2013 and gradually consolidated, particularly from 2016 onwards when growth speeded up in most member states. This upswing has been accompanied by a notable rise in employment, with the EU's average unemployment rate falling from 11% at the beginning of 2013 to 6.3% in Q3 2019. The positive evolution of the labour market, together with a favourable economic outlook translated into higher household disposable income and greater consumer confidence. Likewise, the strengthening and restructuring of the european banking sector also helped to improve credit availability. All this has increased demand for housing, in turn pushing up prices in several european residential markets.

On the other hand, the environment of accommodative financial conditions propitiated by the monetary stimuli of central banks in main advanced economies has also contributed to the synchronized rise of house prices1. First, because it has resulted in a generalised reduction of financing costs to historically low levels2. For example, in the eurozone, the average interest rate for mortgage loans stood at 2.0% in 3Q 2019, compared to 5% in the years before the financial crisis. Secondly, because the low interest rate environment has pushed down bond yields and the return of some financial savings products and that has encouraged demand for property as an investment asset. This is shown by the fact that international and institutional investors, in their search for greater profitability, have intensified their participation in some real estate markets (including residential markets) over the past few years3.

- 1. IMF (April 2018). «Global Financial Stability Report. Chapter 3: House price synchronization: what role for financial factors?».

- 2. Global financial conditions (those prevailing in the world's major financial centres) tend to be passed on through capital flows, which can affect credit availability and mortgage interest rates in the receiving country (irrespective of whether the capital flows are aimed at property). See Bernanke, B. S. et al. (2011), «International Capital Flows and the Return to Safe Assets in the United States, 2003-2007». Federal Reserve Board.

- 3. Hekwolter, M. of Hekhuis, Nijskens, R. and Heeringa, W. (2017). «The Housing Market in Major Dutch Cities». Netherlands Central Bank.

The synchronised growth in EU house prices is explained by both economic and financial reasons, including the economic recovery and accommodative financial conditions, boosting demand for both housing and property investment

In this sense, an IMF study shows that the tendency for house prices in different markets to move in tandem and in the same direction (particularly in the advanced economies) is getting stronger due to financial factors (more accommodative financial conditions and greater financial integration)4. Specifically, these factors currently explain for 30% of the growth in house prices in many advanced economics, well above the 10% explained in 19715.

Both the upward movement of real estate prices and the phenomenon of synchronization of housing markets are more pronounced in main cities of advanced economies. In the case of Europe, this is especially evident when comparing house prices in the largest cities with the average house price in the rest of the cities of a given country (see the next chart).

House prices in large cities tend to be higher than the national average

Ratio of house prices in large cities to the national average for cities

The higher growth in property prices in large cities compared with the national average reflects a generalised trend towards greater urbanisation, an important stimulus for demand for residential property in cities, especially in dynamic locations that attract more talent6.

On the other hand, this phenomenon also responds to the fact that large cities tend to attract more investment per se. For example, within the real estate sector, cities tend to be the most liquid sub-markets with the least uncertain outlook. Also, cities are attractive from an investor point of view for other reasons, such as their excellent location or because they are popular tourist destinations. In addition, in some specific areas, idiosyncratic factors, such as legal and tax systems, can play an important role in attracting foreign investment.

- 6. According to United Nations projections, while two thirds of the world's population was rural in 1950, by 2050 two thirds will be urban.

These factors, which could be called «traditional», have been complemented recently by some of the aspects we've already mentioned. such as accommodative global financial conditions and a larger number of international investors. These factors are especially relevant in large cities that are more open to international capital flows, either because of their integration with global financial markets, or because of their attractiveness to investors looking for greater profitability7.

- 7. Moreover, the aforementioned IMF report shows that the role played by global financial conditions in house price synchronicity is considerably greater when there are regulatory or physical constraints on the supply of housing.

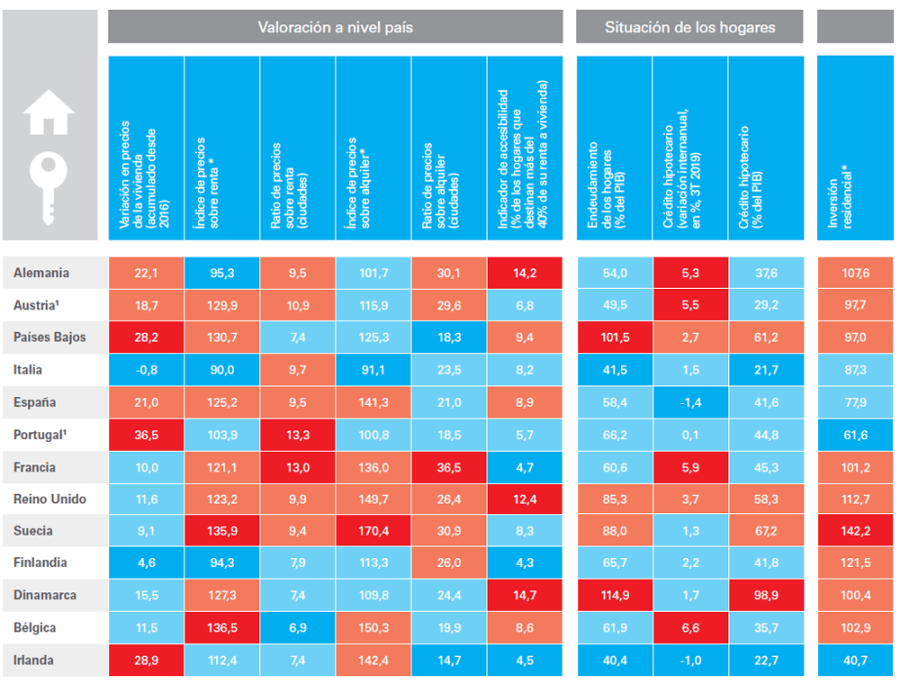

The recent evolution of house prices in several European regions could be a cause for concern. To determine whether house prices are overvalued and detect tensions in the market, we can compare these prices with other indicators of the purchasing capacity of domestic demand. In this sense, a first step to assess whether house prices are too high and detect tensions in the market is put prices in relation to other indicators that show the purchasing capacity of domestic demand.

Risk map for Europe's real estate market

In general, the main for housing affordability indicators do not show, any signs of increasing tension for the local population, although there are some exceptions. The share of European households allocating over 40% of their disposable income to housing costs (a common affordability indicator) stood at 9.9% at the end of 2018, lower than the 2007 average (11.0%). This indicator does suggest, however, that households in Denmark, Germany and the UK are slightly overburdened. For the euro area as a whole, the affordability ratio (house prices compared with household disposable income) is slightly higher than the historical average8, with some differences between countries. In particular, in some countries (such as Belgium, the Netherlands and Austria), residential prices are close to an all-time high and affordability is particularly low (see the table below).

Another benchmark indicator for the financial situation of households is their level of debt, which is at a comfortable level for the euro area as a whole (57.8% of GDP) but of more concern in some European countries, such as the Netherlands and Denmark (above 100% of GDP), although this figure has been falling in recent years. Lastly, except in Sweden and Denmark, similar excesses to those occurring in the mid-2000s have not been observed, such as a boom in property investment and mortgage loans.

- 8. Average between 1980 and 2019.

In general, the main housing affordability indicators show no signs of widespread tension in Europe's property markets, the exceptions being the Netherlands, Austria, Denmark and Belgium

In short, most European countries do not show any evident signs of overvalued property prices compared with domestic demand. However, some countries such as the Netherlands, Austria, Denmark and Belgium could be at risk should house prices continue to grow at the same rate or even faster, as their prices are already at an all-time high. The case of Sweden and the UK warrants particular attention since, after several years of booming house prices and some overheating in the sector, growth has now eased due to factors such as political uncertainty, problems with affordability and fewer tax breaks when buying a home.

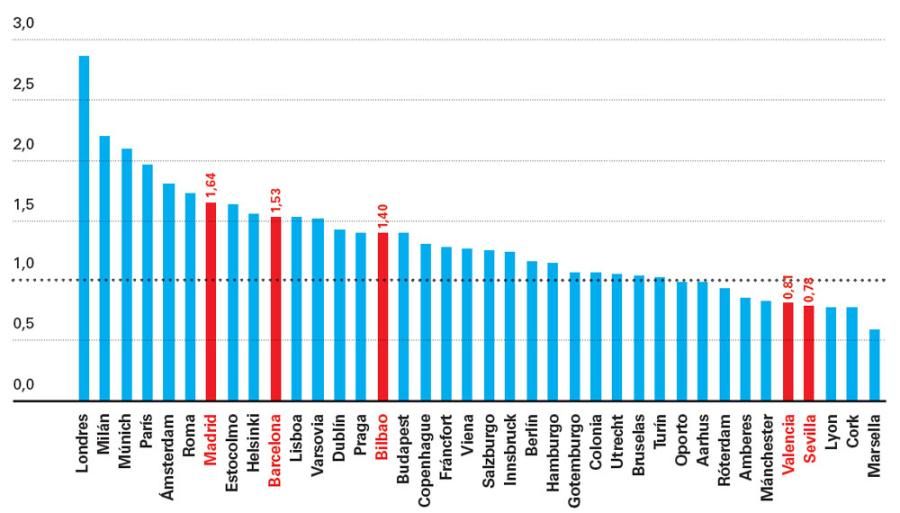

In large cities there are clear symptoms of house prices decoupling from local income and the affordability ratio is particularly high (above 15) in several European metropolises such as London, Paris, Milan and Munich (see the map).

The affordability ratio is particularly high in several European cities

In other cases, prices seem to be slightly higher than those justified by domestic demand, such as in Vienna, Oporto and Barcelona (the article «A widening gap between Spain's house prices» in this Sector Report analyses the trend in house prices and affordability ratios in Barcelona and Madrid). As we've already noted, this is due to several factors, such as the influence of foreign buyers and global and institutional investors, generally with a greater buying capacity than the average local population. Such dynamics mean that a close eye should be kept on the trend in housing markets at a local level (compared with the rest of the country but also with other countries).

The affordability ratios of large cities are getting tight, a reflection of the decoupling of house prices and local income. The ratio is particularly high in London, Paris, Milan and Munich

In short, with the exception of some particular cases, there are no clear signs of overvaluation in European property markets. Also the financial situation of European households is relatively comfortable. However, in large cities there is a certain decoupling between house prices and the income of the local population, partly because of the greater weight of foreign demand. Given the current economic slowdown in many European countries, greater house price synchronicity across countries and cities raises doubts about the consequences of an eventual correction in prices as closer links (exposure of local markets to global financial and economic conditions) may transmit or amplify financial and macroeconomic shocks. In this regard, because of the increasing importance of foreign demand and greater vulnerability of the housing market to the world's financial and economic cycles, the capacity of local authorities to manage imbalances in the property market (through national policies, such as macroprudential, or locally) could now be more limited than in the past.