Macroeconomic outlook for Spain in 2026: resilience in uncertain times

The macroeconomic landscape is once again constrained by a geopolitical conflict. The crisis between the US and Iran, which began over three months ago, remains under a fragile truce. However, the Strait of Hormuz remains closed, which is currently the most damaging factor for the global economy. Spain is facing this episode from a position of strength, but rising energy costs and the deteriorating international environment will reduce economic dynamism and increase inflation. Therefore, we have revised our GDP growth forecast to 2.1% for 2026 and to 1.8% for 2027, compared to 2.4% and 2.0% previously. This is a moderate revision and it does not change the diagnosis of a dynamically growing economy.

A solid starting point

At the outbreak of the conflict, the Spanish economy was enjoying positive momentum. In Q1 2026, GDP grew by 0.6% quarter-on-quarter, 0.1 pp more than expected. Its composition was favourable too: private consumption remained the main growth driver, service exports remained strong, and investment consolidated the gains of previous quarters.

The less positive note once again came from goods exports. Their weakness aligns with a context marked by the US’ protectionist shift and the disruptions associated with the conflict in the Middle East. Even so, the balance of the quarter was positive: the economy continued to grow at a rapid rate and with a range of supports.

The initial indicators for Q2 point to a moderation, not a change of trend. Employment continues to grow rapidly, and consumption is maintaining a positive – albeit more restrained – trend. In contrast, some qualitative indicators, such as the services PMI, show signs of a deterioration in activity and confidence. Overall, we expect the economy to continue growing, albeit at a slower pace than at the start of the year.

The assumptions underpinning the new outlook

The new scenario assumes that the conflict will gradually be brought under control in the coming months. This hypothesis aligns with what energy futures markets are anticipating: high prices in the short term, but with a gradual moderation. This does not rule out occasional episodes of tension, but it does assume that such episodes will be short-lived.

The conflict is affecting the Spanish economy through three main channels.1 The first is inflation, mainly due to rising oil and gas prices. The second factor is external demand, due to slower growth among our trading partners and disruptions to some trade flows. The third avenue involves macro-financial conditions, through increased uncertainty and the expected tightening of monetary policy. In addition to these channels, there are buffers such as fiscal support measures, household savings, and tourism.

The energy channel is the most significant. The scenario encompasses an average oil price of 90 dollars per barrel in 2026, easing to around 79 dollars in 2027, which is still some 20% above what was forecast prior to the conflict. In the case of natural gas, the assumptions have also been revised upwards: approximately 43 euros/MWh in 2026 and 37 euros/MWh in 2027, around 40% above the previous forecasts.2

The impact through the external channel ought to be more contained. The growth forecast for the euro area has been lowered from 1.3% to 0.7%, although 0.2 pps are due to a weaker starting point following the publication of the GDP figure for Q1. Furthermore, Spain’s direct trade exposure through goods exports to the Persian Gulf region is limited, accounting for just 0.5% of GDP. The scenario assumes a 10% loss of these flows, which, together with the revision of the international environment, would reduce growth by around 0.1 pp.3

Regarding macro-financial conditions, uncertainty rose in March according to the Bank of Spain’s index, but the increase was moderate and was corrected in April. As for interest rates, in recent weeks markets have been anticipating that the ECB may raise benchmark rates two to three times this year, bringing the depo rate to 2.5%-2.75% by the end of 2026; indeed, at times a fourth rate hike has even been anticipated. In any case, the impact of higher interest rates will be more noticeable in 2027 than in 2026.

- 1

For a more detailed discussion, see the article «The crisis in Iran: how much could it affect the Spanish economy?» in the MR04/2026.

- 2

See the article «The new (im)balances in the oil market» in this same report for further details on the oil forecast.

- 3

See the article mentioned in footnote 1 for further details about the plausibility of the 10% assumption.

Buffers mitigating the shock

The forecasts incorporate several support factors. The first is fiscal policy. The measures announced in March were estimated to have an impact of 0.3 pps on growth, although the early expiration of some of them reduces the anticipated effect to around 0.2 pps.4 However, if pressure on fuel prices persists, some measures could be extended.

The second buffer is household savings. The savings rate stands at 12.0% of gross disposable income, well above its historical average of around 8.5%. This financial cushion could mitigate the impact of inflation on consumption. The experience of 2022 is illustrative: the price increases triggered by the war between Russia and Ukraine were entirely absorbed by a reduction in savings, which allowed real consumption to continue to grow. In this instance, we assume that consumers will have greater flexibility and will be able to adjust their spending decisions to some extent, such that savings will absorb half of the increase in consumption costs.

The third factor is tourism. The situation in the Middle East could redirect some international tourist flows towards alternative destinations, including Spain – a trend already observed in March.5 This momentum could be constrained by disruptions to international flights or by the loss of purchasing power in source markets. However, based on the available information, we anticipate that the first effect will prevail.

- 4

The reductions in VAT and certain excise duties on electricity and gas is expected to expire at the end of March.

- 5

See the article «What do high-frequency data tell us about international tourism in Spain after the outbreak of the war in Iran?» in the MR05/2026.

Growth: slower, but still dynamic

In 2026, the Spanish economy will retain many of the characteristics that defined 2025. Domestic demand will remain the main support, driven by consumption and investment, while service exports – both tourism and non-tourism – will continue to perform well. In contrast, goods exports will play a more modest role amid global trade weakness and tensions in the Middle East. Furthermore, the increase in imports required to meet domestic demand will reduce external demand’s contribution to growth.

Private consumption will continue to be supported by demographic growth, driven by immigration, and by the strength of employment. Investment will continue to benefit from the deployment of NGEU European funds. Since 2026 is the final year of the programme, the forecast anticipates that these funds will be executed in full before the deadline.

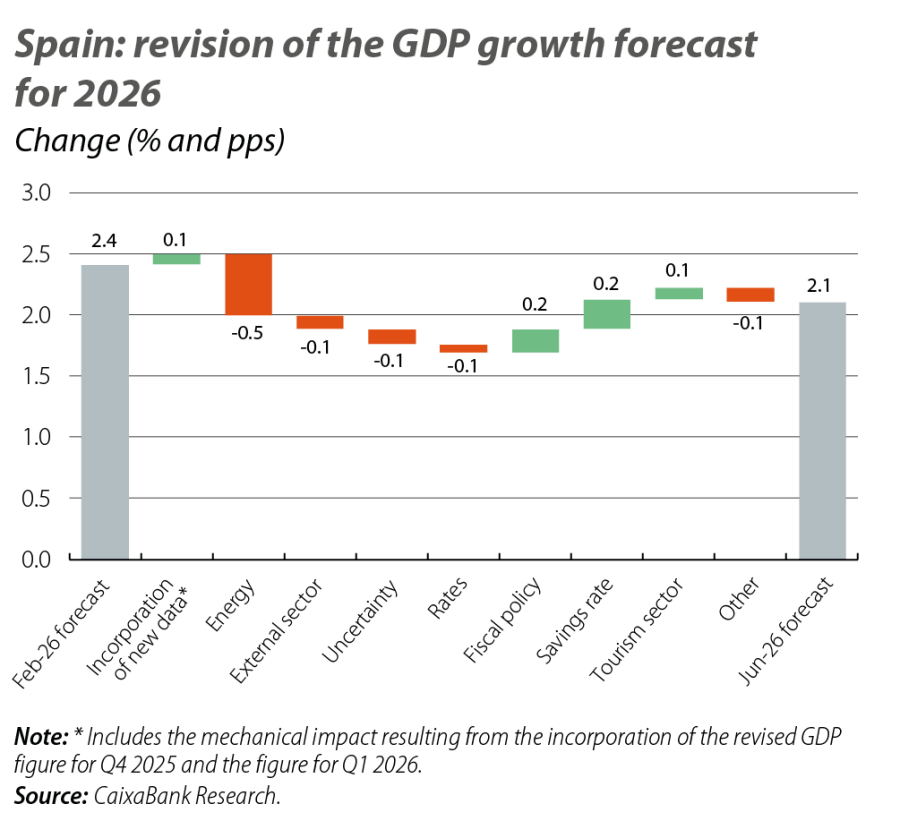

The revision of GDP for 2026 reflects the balance between the negative channels of the conflict and the supporting factors (see chart). The rising cost of energy is by far the biggest burden. Added to this are the deterioration of the external sector, increased uncertainty, and the impact of higher interest rates. Conversely, fiscal policy, the partial use of savings, and the improved tourism outlook limit the adjustment.

Overall, we have revised the GDP growth forecast downwards by 0.3 pps in 2026 to 2.1%, and by 0.2 pps in 2027 to 1.8%. The revision for 2027 is almost entirely explained by the impact of higher interest rates. Nevertheless, we expect the economy to continue to grow at an average annual rate of around 2%.

The most visible impact of the conflict will be on prices. The inflation forecast for 2026 has been revised from 2.4% to 3.5%, mainly due to the rise in oil and gas prices. This estimate also incorporates the effect of the temporary reductions in VAT and excise duties on fuels, gas and electricity, which partially moderate the impact on the CPI.

In 2027, inflation is expected to be 2.7%, compared to the previously forecast 2.2%. That year, the indirect effects of rising energy costs are expected to become more evident, as producers pass on part of the increase in energy costs to other goods and services. Industrial goods and food will be the components most affected. In addition, the reduced global supply of fertilisers, particularly urea from the Persian Gulf, could also have an impact.

The scenario does not encompass any significant second-round effects. The temporary nature of the shock, the absence of intense underlying inflationary pressures, and the anticipated actions of the ECB should prevent a substantial acceleration in wages.

Risks: greater than usual uncertainty

Uncertainty is high and the risks are skewed to the downside. The main factor will be the duration of the blockade of the Strait of Hormuz. If it were to last several months, the implications would be substantial: higher inflation, further deterioration of external demand and a possible blow to tourism. Furthermore, in that context, the ECB might be forced to raise rates further, and household and business confidence would suffer more.

There are also upside risks. If the blockade were to be lifted in the coming weeks, energy prices could moderate more quickly and confidence could recover sooner than expected, leading to a better performance in economic activity. Similarly, fiscal support could exceed what is considered in the scenario, and the household savings rate could absorb a larger portion of the consumption shock.