What do high-frequency data tell us about international tourism in Spain after the outbreak of the war in Iran?

International tourism spending accelerated slightly in March 2026, driven by the redirection towards Spain of tourist flows from the main European source countries. This upturn offset the decline in tourism from East Asia, which, although intense, represents only a small portion of tourist arrivals in Spain.

The outbreak of the war in Iran has opened an uncertain chapter for international tourism in Spain. Although, historically, episodes of geopolitical instability in the Middle East have boosted tourism to Spain,1 both the disruption at airport hubs in the Persian Gulf and the sharp rise in oil prices and the possibility of fuel shortages for air transport have raised doubts about the net impact of the conflict on the sector’s growth.

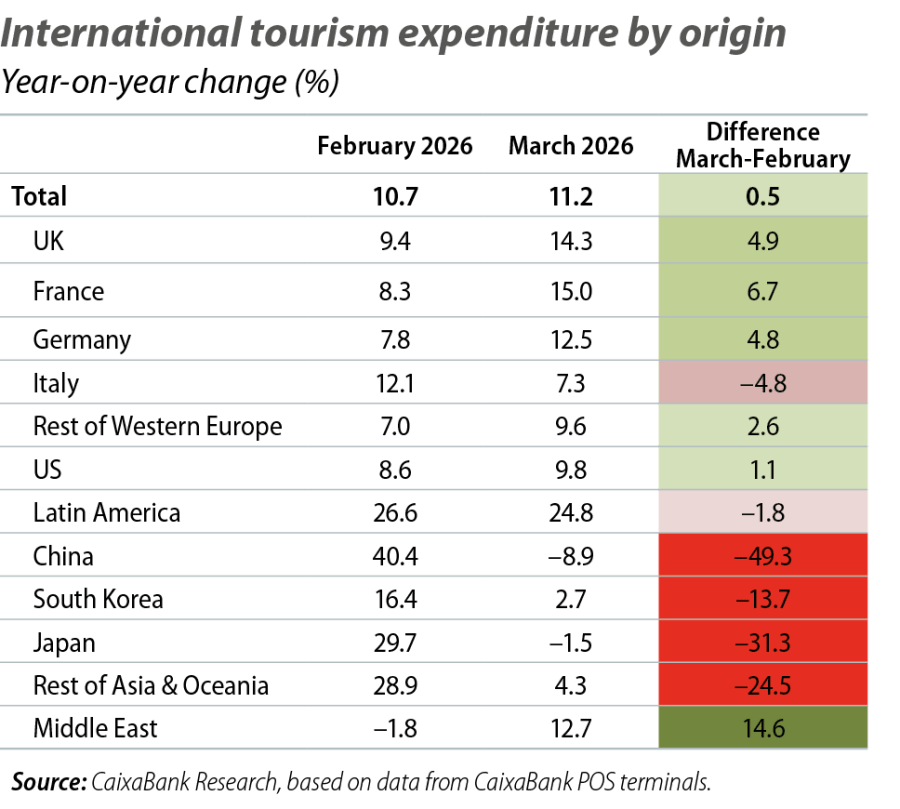

For now, data from international cards used on CaixaBank point-of-sale terminals show that the growth of spending by international tourists increased from 10.7% year-on-year in February 2026 to 11.2% in March. This acceleration is mainly explained by the greater buoyancy of tourism from the United Kingdom, France and Germany, the three main source markets for tourists visiting Spain. Overall, tourism spending from these three countries accelerated by an average of 5.5%, placing the growth of all of them at double-digit rates.

This progress offset the decline in spending by tourists from East Asia, a region particularly affected by the disruptions to air transport. Tourism spending from China, Japan, South Korea, and the rest of Asia and Oceania went from growing at an average rate of 28.9% in February 2026 to falling by 0.9% in March, representing a deceleration of nearly 30 pps.

- 1

See the article «What are the trends for international tourism in Spain in 2024? A sensitivity analysis based on macroeconomic factors» in the Tourism Sector Report S1 2024.

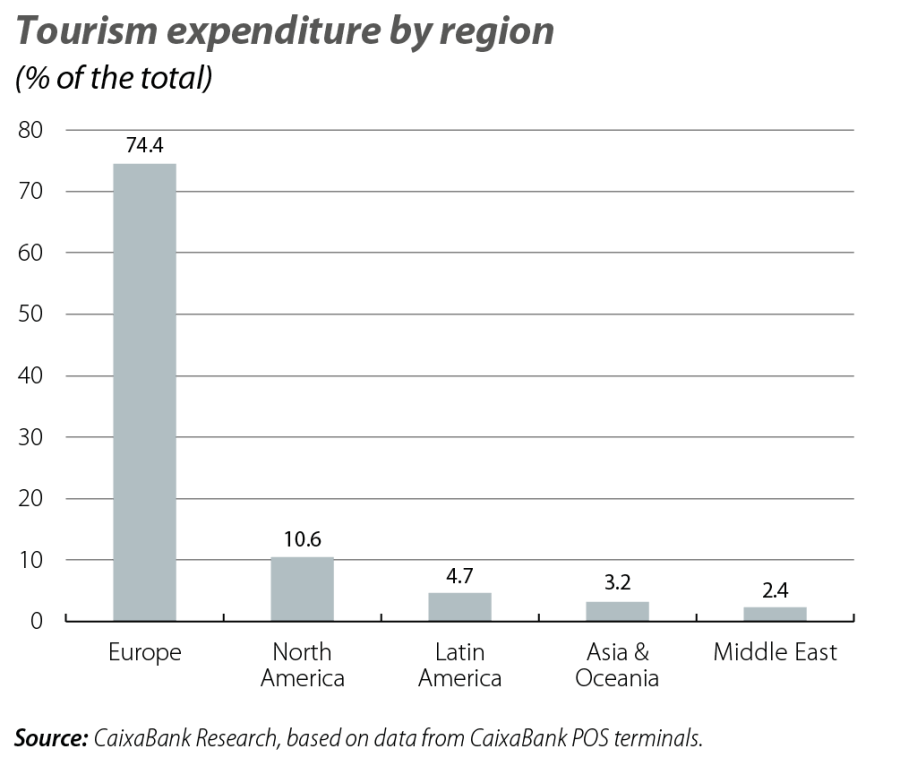

Although this decline, in absolute terms, was much greater than the acceleration observed in European tourism, its overall impact was limited by the small share that Asian tourism represents for the sector as a whole. In the last 12 months, Asia and Oceania accounted for just 3.2% of international tourism spending in Spain, compared to 74.4% in the case of European tourism. Thus, the resilience of European tourist flows to Spain, which was partly due to the redirection of these flows in favour of our country, more than offset the sharp slowdown in Asian tourism.

More striking was the evolution of tourism spending from the Middle East, which went from contracting by 1.8% in February to growing by 12.7% in March. This improvement, of 14.6 pps, seems to be due to the temporary relocation of residents from Gulf countries who fled the areas affected by the conflict.

Taken together, these data reinforce CaixaBank Research’s forecast that the redirection of tourists from the Gulf and the eastern Mediterranean will contribute to a slight acceleration of Spain’s tourism sector in 2026. There is, however, an important caveat: this scenario is consistent with a short-lived conflict. If, in a scenario with a prolonged conflict, this were to reduce the growth of gross disposable income in source countries by more than 2.5 pps, then the net effect of the conflict on international tourism in Spain would no longer be positive.

Geopolitics

We analyse the major geopolitical trends and thier effects on the financial markets and the economy.

Real-Time Economics

Follow the evolution of the Spanish economy with our real-time indicators and our published articles.