Spanish households’ finances improve thanks to job creation and a reduction of debt

The strengthening of Spanish households’ finances has exceeded expectations and is good news for the Spanish economy, as the challenging context looks set to continue over the coming quarters.

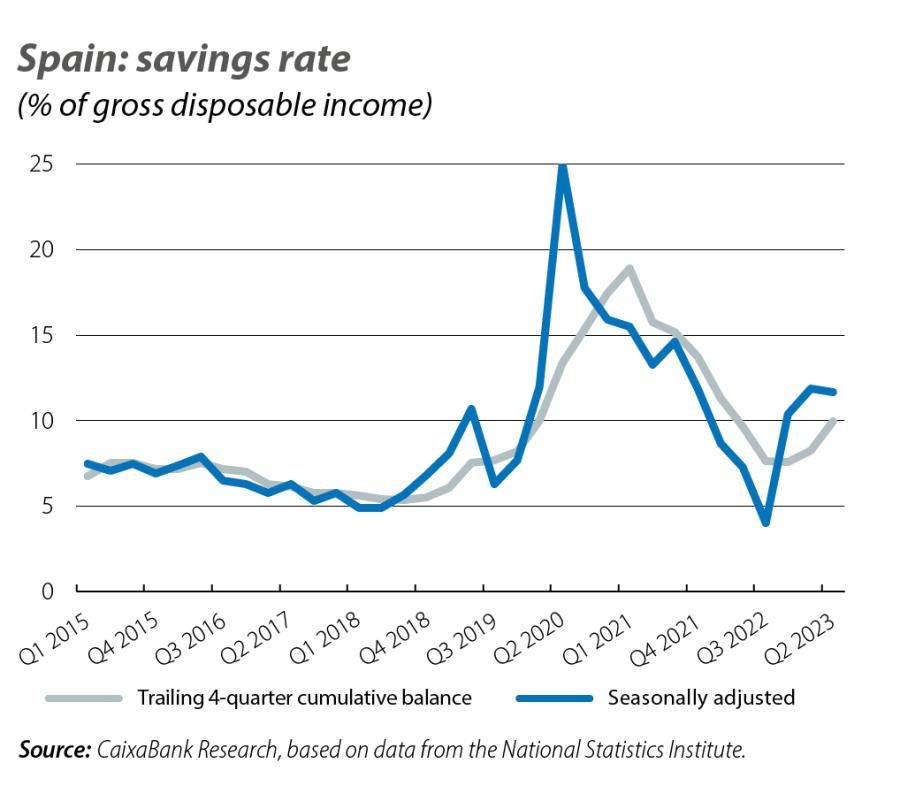

In Q2 2023 there was a sharp rise in the Spanish household savings rate, accentuating the change of trend initiated in the previous quarter. Specifically, having peaked at 19.4% in Q1 20211 due to the collapse in consumption during the pandemic, we witnessed how the savings rate steadily declined, reaching as low as 7.9% by the end of 2022. This downward trend in savings was truncated in Q1 2023 (savings rate of 8.5%) and the rebound intensified in Q2, when the savings rate in the cumulative last twelve months rose to 10.2%, placing it well above the pre-pandemic average (7.2% on average in 2015-2019).

The savings rate is also high in seasonally adjusted terms (11.7% in Q2 2023 in static terms, after bottoming out at 4.0% in Q3 2022).

- 1. Savings as a percentage of disposable income, trailing four-quarter cumulative balance.

The rebound in the savings rate was driven by the fact that the total gross disposable income of all households grew by a spectacular 12.2% year-on-year in Q2 2023 (static figure), the highest rate in the entire historical series. The main factors behind this growth were: the increase in total wages (+8.7% year-on-year), reflecting the rise in employment (growth of +3.1% year-on-year in the number of employees) and greater buoyancy in wages (growth of +5.2% in remuneration per worker), the increase in social benefits (+9.7% year-on-year, driven by the pension revision), self-employed workers’ income and income from assets thanks to the increase in the payment of dividends and other investment income. All this has more than offset the increase in net interest payments, which have risen to 3.3 billion euros (an increase of 1 billion versus the static figure for Q2 2022).

This growth in gross disposable income offers greater scope for an increase in consumption over the coming quarters, and this in turn would translate into higher GDP growth. This can be illustrated with a simple calculation: if the savings rate were to fall by 1 more point than expected next year, then the impact on GDP growth would be around +0.4 pps.2 As for the level of disposable income per household, growth remains at 5.8%; although high, this is a more moderate growth rate as there has been a sharp rise in the number of households. Specifically, in the last year some 275,000 households were created in net terms (+1.4% year-on-year), largely due to migratory flows.

- 2. To understand this calculation, it must be taken into account that the savings rate captures the level of savings relative to gross disposable income, and gross disposable income stands at 60% of nominal GDP. Therefore, a 1-point reduction in the savings rate would, in theory, lead to an increase in GDP growth of around 0.6 points through increased consumption. Considering that the portion of consumption which corresponds to imports is 30%, we calculate that the impact on GDP growth would be 0.4 pps.

Following the upward revision of the historical series of gross disposable income and the strong figures for 2023, real disposable income per household already recovered its pre-pandemic level back in Q1. Total disposable income in real terms, meanwhile, was already 3.5% above the pre-pandemic level by the end of Q2.

In contrast, household spending relating to consumption has been losing steam as inflation has moderated and interest rates have risen. Indeed, in Q2 there was a significant gap between the growth of total wages and that of household spending. Whereas these two variables were growing at relatively similarly rates in Q1 (8.6% and 7.3% year-on-year, respectively), in Q2 total employee wages grew well above household expenditure (8.7% year-on-year vs. 5.2%).

For 2023 as a whole, following such strong data we anticipate that the growth of gross disposable income will far exceed 6.0%, and this should allow aggregate household consumption in real terms to end the year well above its 2022 level, despite the increase in interest rates and inflation remaining high.

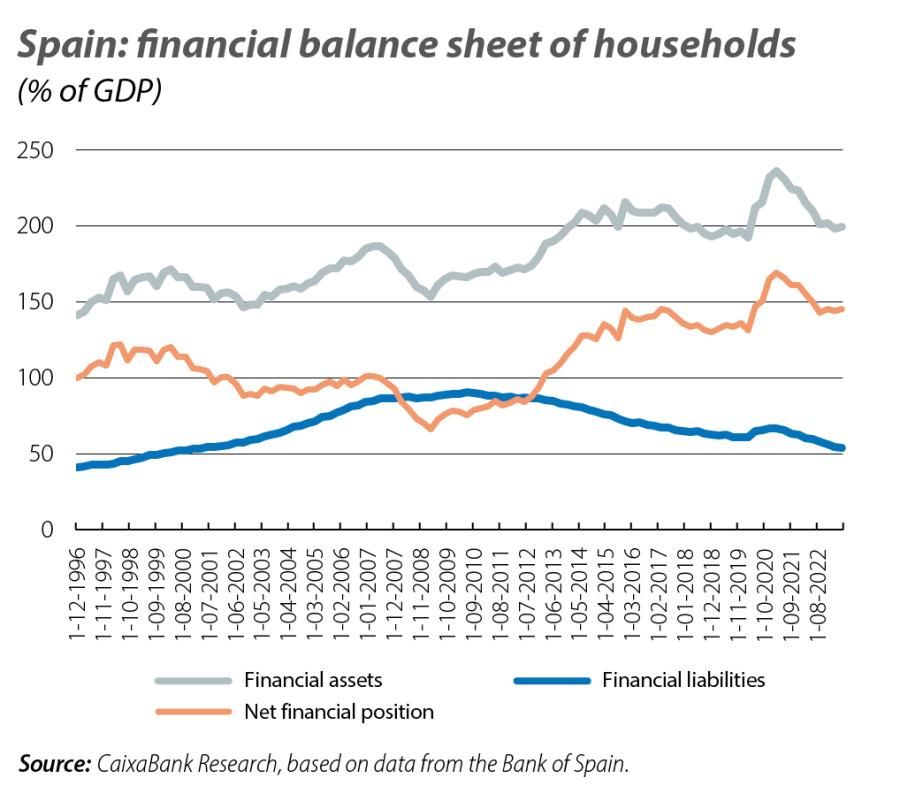

Households’ net acquisition of financial assets in Q2 2023 amounted to 41 billion euros, very similar to Q2 2022 and above the Q2 average of 32.6 billion between 2015 and 2019. Households increased their bank and cash deposits (+7 billion euros vs. 21 billion in Q2 2022) and invested in debt securities, equities and investment funds (6.7 billion and 4 billion, respectively, well above Q2 2022). The acquisition of assets was accompanied by a sharp rally in their valuations (29 billion euros), mainly due to the gains registered in equities and investment funds (increase of 27 billion). As such, the stock of households’ gross financial assets grew by 70 billion euros, reaching a total of 2.81 trillion.

Household debt, meanwhile, rose by just under 7.4 billion euros (essentially due to seasonal factors), although it stood at 49.9% of GDP, −0.5 pps compared to Q1 2023, placing it in line with the level of mid-2002. The debt ratio of Spanish households thus lies 5.5 pps below the Euro area average.

Given that the growth of financial assets has outstripped that of financial liabilities, there has been an increase

in net household financial wealth of 61 billion euros compared to the previous quarter, placing it slightly above 2.05 trillion euros (145.4% of GDP).

In short, the strengthening of households’ finances has exceeded expectations and is good news for the Spanish economy, as the challenging context looks set to continue over the coming quarters.