The financial conditions behind the economic scenario in 2026

The conflict in the Middle East has caused the financial environment to take a step backwards. Although it has not experienced significant tightening overall, it is less favorable to the performance of economic activity in the coming quarters. The risks are high, and while a swift resolution of the conflict could ease financial conditions, the prolonged blockade of the Strait of Hormuz threatens to exponentially increase economic and financial costs if oil and derivative product stocks fall too low and can no longer cushion the contraction in energy supply. It is also important not to overlook market monitoring of public debt dynamics in several advanced economies, nor the financial risks associated with AI, both in terms of its ability to live up to expectations and its potential to disrupt established economic structures.

The war in the Middle East has altered the economic outlook for the coming quarters and the financial conditions that underpin it.1 The blockade of the Strait of Hormuz and the damage to the region’s infrastructure have led to a surge in the cost of energy commodities, various derivative products (such as fuels and fertilisers), and other products where the Middle East plays an important role as a producer or transit region (e.g. aluminium). All this has led to a global rise in inflation and, combined with the significant uncertainty regarding how long the conflict will last, an increase in volatility.

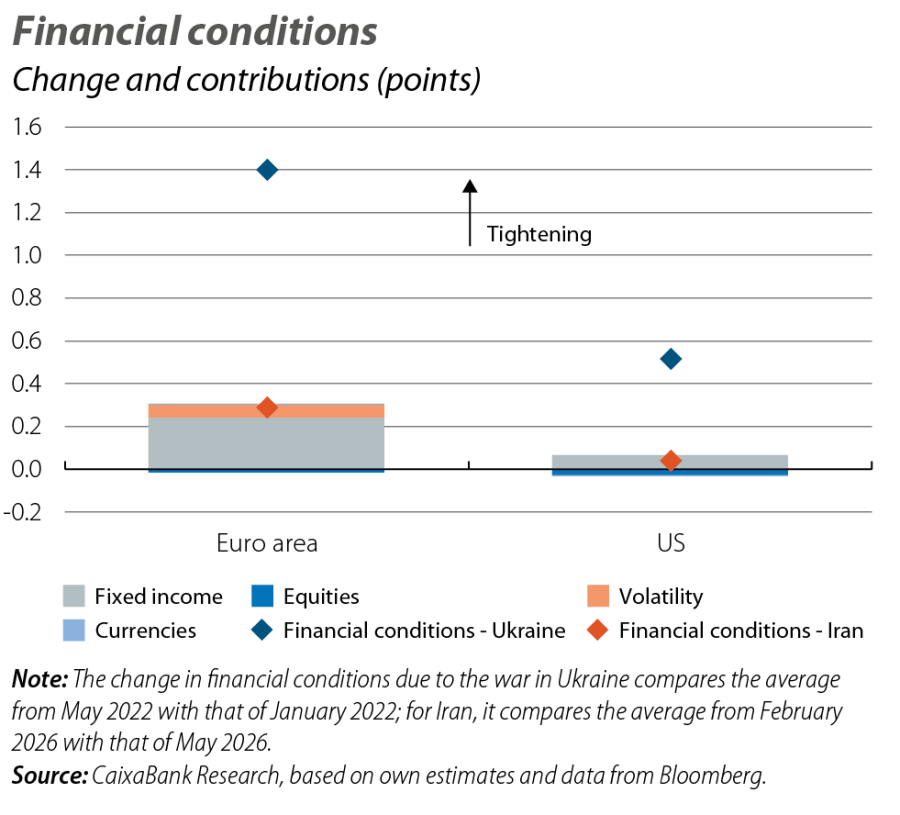

This context has led to financial conditions that are less favourable for economic activity in the coming quarters, characterised by increased volatility, higher interest rates, and a narrower path for corporate profits and stock market performance. However, the tightening of financial conditions has so far been moderate, as shown in the first chart, and has been mainly due to the rise in interest rates and increased volatility. In contrast, equities have helped to ease tensions, supported by a strong corporate earnings season so far this year (due to both reported profits and future expectations), optimism around AI, and the view that the energy shock will impact inflation more than economic activity. Among advanced economies, the euro area has experienced greater tightening than the US, reflecting its relative vulnerability to the new shock (in fact, in the US, financial conditions indices show a very modest net tightening).2

- 1

See the Focus articles «International economic outlook» and «Macroeconomic outlook for Spain: resilience in uncertain times» in this same report.

- 2

The analysis is based on the financial conditions indices developed by CaixaBank Research (see, for example, the article «The ECB’s holistic approach» in the MR06/2021). Other indices, such as those by Bloomberg and Goldman Sachs, convey a similar message, with moderate tension in euro area financial conditions due to the conflict in the Middle East and little impact on those in the US.

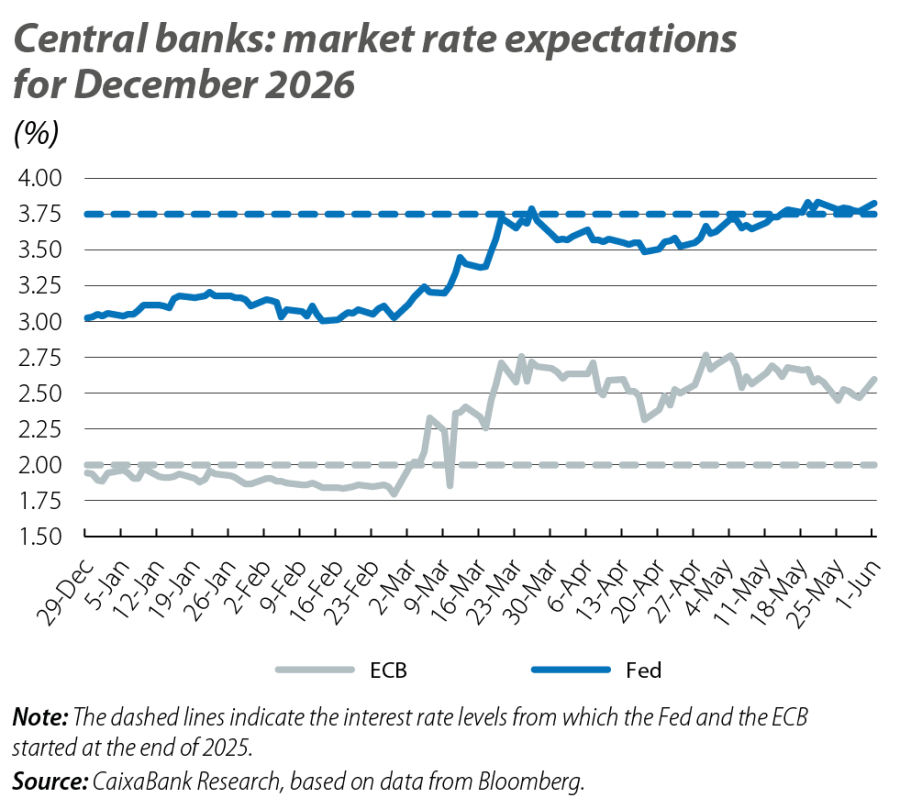

Setting energy aside,3 the main change in the financial environment is the direction of monetary policy. In a scenario in which the energy shock is significant enough to directly push inflation above 3% for 2026 as a whole, the main central banks have signalled their intention to adopt a moderately restrictive monetary policy. Our new economic forecasts are thus based on the view that the ECB will raise its official rate to 2.50% in 2026 and maintain it at this boundary between neutrality and restriction for much of 2027 (vs. a pre-conflict expectation of stable rates at 2.00%). The Fed will put its planned rate cuts on hold, and keep the fed funds rate stable in the 3.50%-3.75% range (the 2025 year-end level). With this measured hawkish shift, both central banks will help mitigate the risk that rising energy costs could lead to indirect and second-round effects.4 On this basis, our scenario anticipates that both the ECB and the Fed could resume their pre-conflict interest rate paths by the end of 2027.5

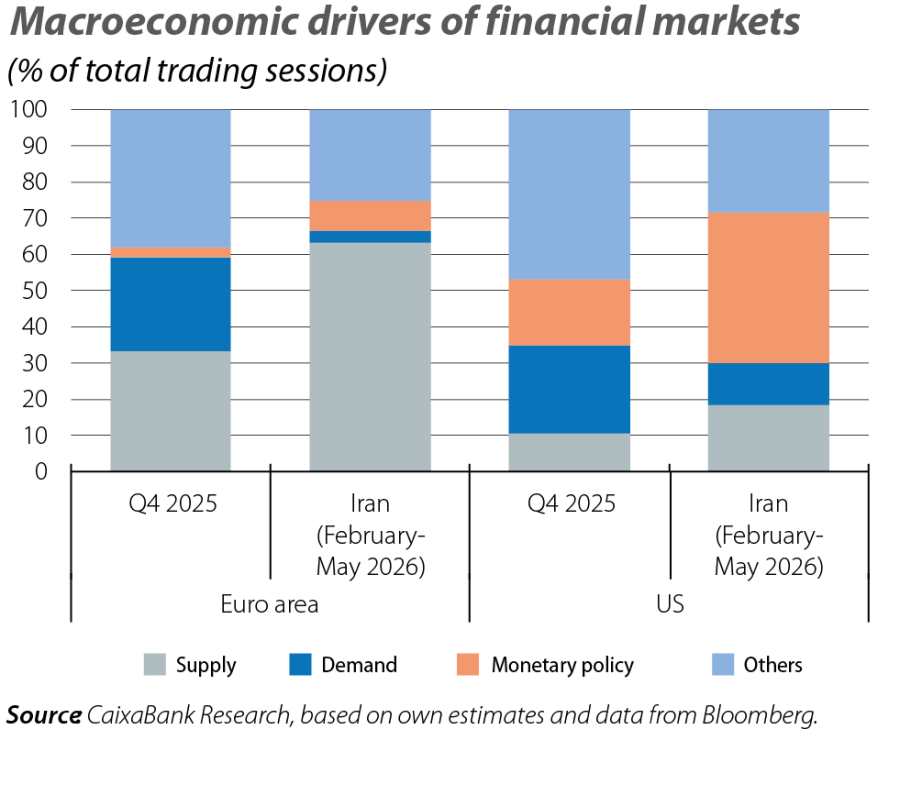

The differing reactions of the ECB and the Fed not only reflect their different starting points (inflation at the 2% target in the euro area and neutral monetary policy vs. greater inflationary inertia in the US and moderately restrictive rates), but also the fact that the shock derived from the Middle East is of a different nature in each region. Europe’s reliance on energy imports significantly exposes the euro area to rising energy commodity prices, even though the Middle East is not a major supplier to Europe. In contrast, the US’ energy autonomy gives North American economic activity better protection from the direct shock. This has been reflected in a differential performance between the European and US financial markets: the third chart shows how, since the bombings between Iran and the US and Israel, European markets have been dominated by a narrative of a «negative supply shock», while trading sessions in US markets have been characterised by a «monetary policy tightening shock».6 Despite this, the euro exchange rate has remained relatively stable against the dollar, which has gained little (in terms of appreciation) from its role as a safe-haven asset despite the renewed spike in uncertainty. Thus, we maintain our forecast of relative strength for the euro, and see the exchange rate edging towards 1.20 dollars in 2027.

- 3

See the Focus «The new (im)balances in the oil market» in this same report for an overview of the impact and state of the oil market three months after the outbreak of the conflict.

- 4

Indirect and second-round effects should also be mitigated by the absence of significant imbalances between aggregate supply and demand (as indicated by the modest GDP figures for the euro area in recent quarters or the cooling of the US labour market), as well as by the deterioration in business and consumer confidence reflected in the latest indicators, stemming from the conflict in the Middle East. On the other hand, a prolonged conflict, increased energy tensions, and/or the influence on inflation expectations of the recent memory of the inflationary crisis triggered by the war in Ukraine could lead to higher inflation and encourage a more aggresive monetary tightening.

- 5

In other words, the ECB will return the depo rate to 2.00% and the Fed will resume a path of moderate cuts (fed funds rate at 3.00%-3.25% by the end of 2027).

- 6

The characterisation of market sessions between demand, supply or monetary policy drivers is based on the co-movements of the various classes of financial assets. For example, we associate a negative supply shock (which depresses activity and raises prices) with stock market declines and higher interest rates (with expectations of monetary tightening to combat inflation); a positive demand shock is linked to stock market gains (higher corporate profits), higher inflation expectations, and higher interest rates; and a restrictive monetary policy shock is associated with rises in sovereign rates, an appreciation of the domestic currency, and a decline in stock markets and inflation expectations. For more details on this extraction of economic narratives from financial markets, see the Focus «What markets tell us about macroeconomics» in the MR05/2026.

Overall, the conflict in the Middle East has caused the financial environment to take a step backwards. Although it has not experienced significant tightening overall, it is less favorable to the performance of economic activity in the coming quarters. The risks are high, and while a swift resolution of the conflict could ease financial conditions, the prolonged blockade of the Strait of Hormuz threatens to exponentially increase economic and financial costs if oil and derivative product stocks fall too low and can no longer cushion the contraction in energy supply. It is also important not to overlook market monitoring of public debt dynamics in several advanced economies, nor the financial risks associated with AI, both in terms of its ability to live up to expectations and its potential to disrupt established economic structures.