International economic outlook

At the close of this report, the conflict in the Middle East remains unresolved and continues to exert pressure on the price of energy and its derivatives. The duration of the conflict will be crucial in assessing its economic impact. The region produces nearly 30% of the world’s crude oil and 20% of its gas, the latter being a key input in the production of fertilisers and helium, which are essential for semiconductor manufacturing. Additionally, it contains two of the world’s major maritime routes: the straits of Hormuz and Bab-el-Mandeb (in the Red Sea). Moreover, there are factors that could hasten a resolution to the conflict, such as Trump’s declining popularity (which could affect him in the mid-term elections) and the high economic cost of the war. Given the uncertainty of the environment, our economic forecasts are anchored in quoted market energy prices.

Specifically, our forecast scenario is based on futures traded by financial markets over an average of 14 trading days (to reduce their volatility). Based on this data, the Brent barrel will remain above 100 dollars up until July, before gradually easing to around 85 dollars by the end of the year. This will place the average Brent price at approximately 90 dollars in 2026 and almost 80 dollars in 2027, well above the levels anticipated prior to the conflict (some 25 and 15 dollars higher, respectively). Furthermore, prices are not expected to return to pre-war levels until at least 2030. In the case of gas prices, the impact has been much less severe than that triggered by the outbreak of the war in Ukraine. Overall, the futures underpinning our forecasts anticipate an average gas price of just under 45 euros per MWh in 2026 and just over 35 euros per MWh in 2027, which is 10-15 euros more expensive each year than expected before the conflict.

In other words, energy futures seem to be factoring in a gradual resolution of the military conflict that would lead to the reopening of the Strait of Hormuz, while acknowledging that this does not mean economic activity will immediately recover to pre-conflict levels.1

In this context of higher energy prices, economic growth will be lower than expected before the conflict, especially in countries more dependent on energy imports (Europe and Asia, particularly India, which is especially affected). Inflation will rise across the board, causing the main central banks to adopt a more hawkish stance.2

- 1

See the Focus «The new (im)balances in the oil market» in this same Monthly Report.

- 2

See the Focus «The financial conditions behind the economic scenario in 2026» in this same Monthly Report.

The euro area faces another energy shock

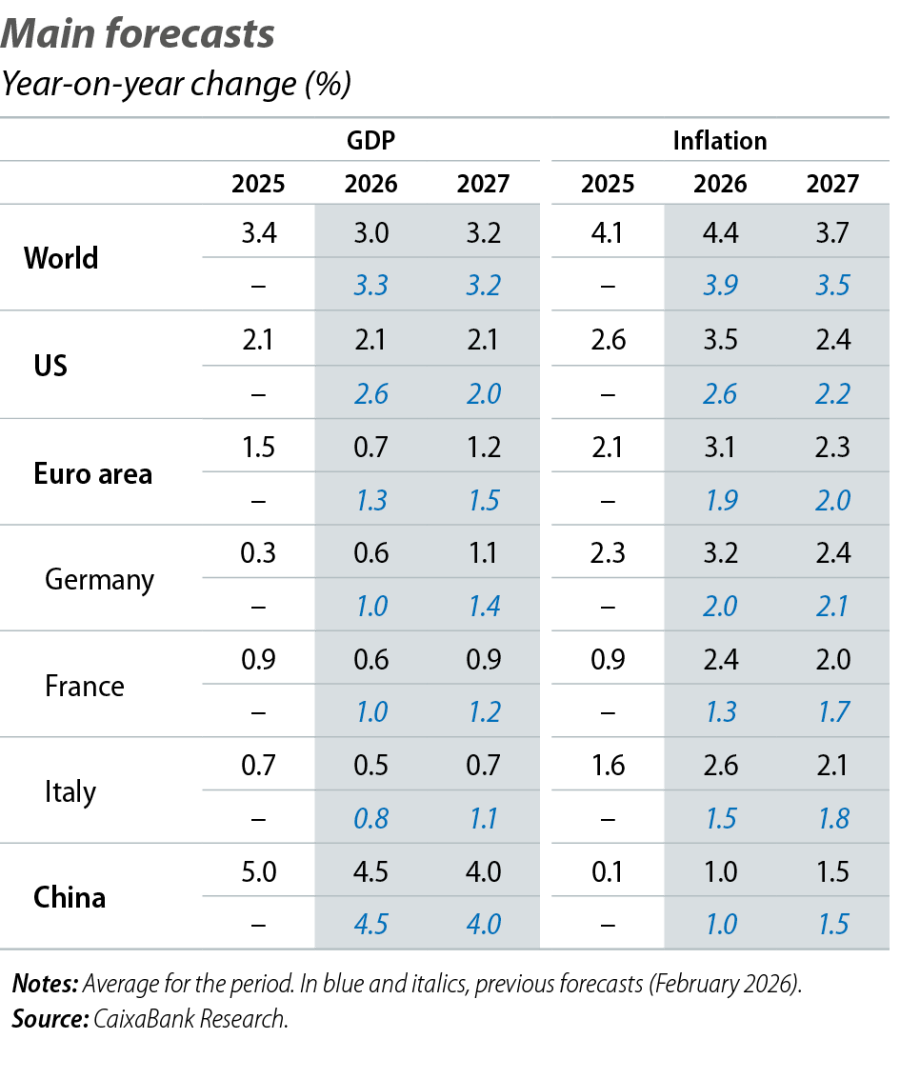

The region’s direct exposure to the Middle East is limited. However, despite efforts in recent decades to improve energy efficiency and promote the use of renewable energies, there remains a high dependency on fossil fuels: they account for nearly 70% of all the energy consumed by the entire economy, and they are practically the only type of energy used in the transport sector.3 The impact of higher energy prices will result in increased inflation over the coming months, averaging above 3.0% in 2026, approximately 1.0 pp higher than expected before the war. Therefore, household purchasing power will be squeezed and private consumption will slow in the coming quarters, but it will not contract, thanks to the substantial savings buffer (more than 14% of gross disposable income) and a still resilient labour market (the unemployment rate has been around a historic low of 6.2% for over a year). It is also important to note that the end of 2025 and the beginning of 2026 in the euro area were weaker than expected, which explains the substantial downward revision we have made: –0.5 pps in 2026, to 0.7%, and –0.3 pps in 2027, to 1.2%. On the other hand, this slowdown in activity will mitigate indirect and second-round effects and, together with various fiscal measures already approved, it will help contain the inflationary impact of the war. For now, the euro area will avoid entering recession, but such an outcome cannot be ruled out if the conflict drags on and more adverse scenarios materialise.

- 3

See the Focus «Europe faces another energy crisis» in the MR04/2026.

US, the impact of higher inflation on a growth model heavily reliant on technology investment

The US is the world’s largest producer of crude oil and gas and a net exporter, but this does not mean that its consumers are unaffected by rising energy prices. In fact, inflation is already reflecting this impact (petrol is above 4 dollars per gallon), in a context in which service prices were already showing significant resistance to moderation. As a result, the direct impact of rising energy costs will cause headline inflation in 2026 to be almost 1.0 pp higher on average than it would have been without the conflict, reaching 3.5%. This inflation pattern will dent household consumption, as indicated by the significant deterioration in the main household confidence indicators, although they will still maintain dynamic growth rates. Furthermore, we remain confident that investment in technology will remain strong due to the boost from the deployment of AI, so the US economy should continue to advance at a steady pace. However, since Q4 2025 and Q1 2026 were weaker than expected, we have reduced our growth forecast for 2026 by 0.5 pps to 2.1%, a rate which will be maintained in 2027.

China will benefit from the boost provided by its high value-added exports

The Chinese economy faces the impact of the war in the Middle East with some ambiguity. As a net energy importer, it is adversely affected by the sharp rise in energy costs, while its exports to Europe (accounting for around 16% of its total) are hindered by trade disruptions in the region. However, the rise of AI and the development of green energies in much of the world are boosting its high-value exports, sectors in which China has already become a global leader. In the short term, this greater diversification of Chinese exports will help sustain the growth of its economy. This, combined with the tariff cuts prompted by the US Supreme Court and a slightly better than expected start to the year, reinforces our growth forecast of 4.5% for 2026 and 4.0% for 2027. The measures implemented by the government to contain the impact of the energy shock will keep inflation under control, which was very low before the conflict. We thus expect it to be in the 1.0%-1.5% range in 2026 and 2027.

In short, it seems we are heading towards a world with lower growth and higher inflation. Uncertainty remains high and the most adverse scenarios cannot yet be ruled out, with highly uneven regional impacts and inflation reaching higher for longer, as the IMF already warned in its April report. Nevertheless, it is important to emphasise that the situation differs from 2022, when significant disruptions still affecting global supply chains after the pandemic drove global inflation to nearly 9.0%.