What to expect from the international economy in 2026

The global economy demonstrated notable resilience during 2025, providing a good starting point for 2026, such that the global economy could continue to grow at a rate of around 3%, with globally stable inflation. However, the risks to the baseline global scenarios have increased significantly following the joint US and Israeli attack on Iran, which has triggered a surge in oil and gas prices and turmoil in the financial markets.

The global economy demonstrated notable resilience during 2025, providing a good starting point for 2026. Going forward, there is sustained growth due to a more neutral monetary policy, as well as a fairly neutral tone in fiscal policy, albeit constrained by large deficits and high debt in the major economies. The dynamism we continue to anticipate for investment in technology, especially in artificial intelligence (AI), is also crucial. Under these assumptions, the US will continue to grow at a steady pace, with the euro area consolidating the momentum it achieved at the end of 2025. China will continue to experience a slowdown (4.5% in 2026 and 4.0% in 2027), reflecting the persistence of the residential sector adjustment and the impact of tariffs, with investments in AI as the main growth driver. In the rest of Asia, technology-intensive economies will continue to benefit from the global investment cycle, and India’s growth will outpace China in the coming years. Therefore, the global economy could continue to grow at a rate of around 3%, with globally stable inflation.

However, these projections are based on the environment anticipated before the outbreak of the war in the Middle East. That is to say, it relies on gas and crude prices determined by supply and demand fundamentals, which in recent quarters have been characterised by an oversupply of oil and stability in gas. As we note at the end of the article, the latest events highlight the risks to this hypothesis, the validity of which will depend on the duration and scope of the conflict.

The euro area will continue to grow slowly but surely

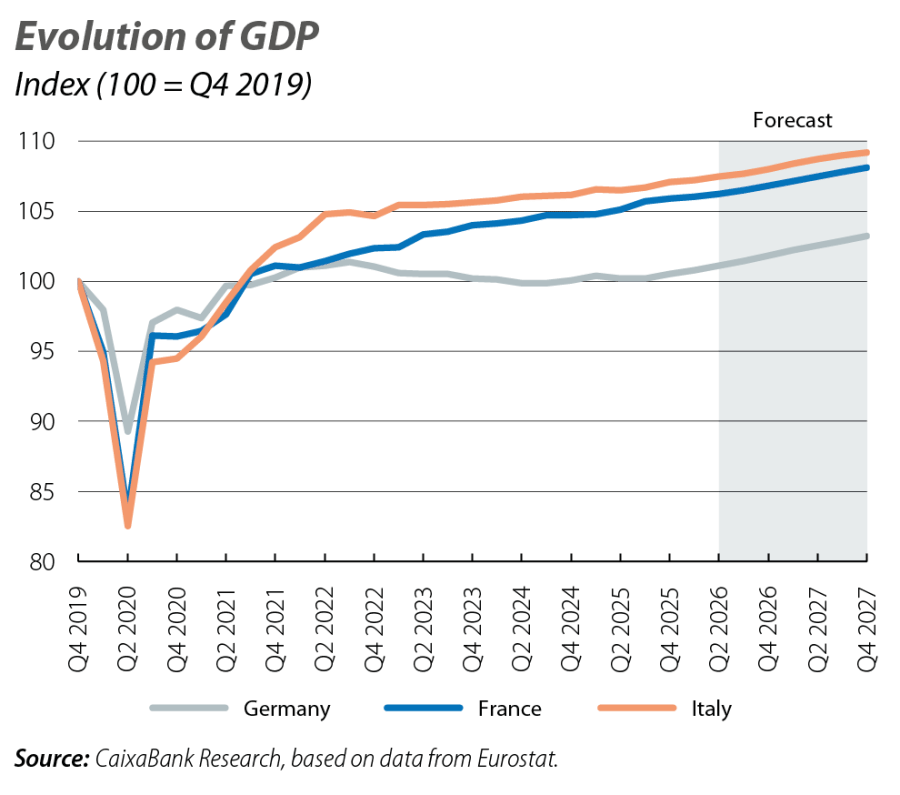

The euro area will maintain modest growth rates (slightly above 0.3% quarter-on-quarter on average), reaching 1.3% in 2026, following 1.5% in 2025. This apparent slowdown reflects the normalisation of growth in Ireland to rates of around 3.0% (13.3% in 2025). Excluding Ireland, the euro area would grow by 1.2% in 2026, following 1.0% in 2025. As for inflation in the euro area, it will remain sufficiently close to the 2% target throughout the forecast horizon.

This outlook is supported by Germany’s recovery after five years of virtual stagnation. The deployment of the fiscal bazooka1 approved last year will be key for Germany’s growth. The 2026 budget includes a 3.5% increase in public spending, investment growth of nearly 10% thanks to the deployment of the Infrastructure Fund (1.3% of GDP through to 2029, compared to 0.9% in 2025) and defence spending of 2.8% of GDP (2.0% in 2025).2 However, the budgets forecast a fiscal deficit of 3.25% in 2025 and of 4.75% in 2026, but delays in their approval and execution explain why the fiscal deficit in 2025 was 2.5%, following the –2.7% of 2024: this means that there was no fiscal stimulus in 2025. This circumstance reinforces doubts about the utilisation of the fiscal stimulus.3 Overall, the increased growth compared to a scenario without this fiscal stimulus would be between 0.4 pps and 0.8 pps4 in the coming years, supporting the forecast of German growth of 1.0% in 2026 and of 1.4% in 2027.

In France, growth is expected to remain around 1% in 2026 and 2027. The budget for 2026, approved earlier this year after arduous negotiations, envisages a fiscal deficit of 5.0% of GDP (5.4% in 2025) and it includes tax hikes for large corporations and delays the implementation of the pension reform until 2027. The fiscal situation in France remains rather delicate, and this will put pressure on financing costs, influencing the investment and consumption decisions of households and businesses.

In Italy, growth will be constrained by apathetic private consumption and the lack of momentum in foreign demand. Investment will be the main driver thanks to the NGEU funds still available before the programme expires in August. Financing conditions will remain favourable, supported by a neutral fiscal policy (the deficit is expected to be reduced by 0.2 pps to 2.8% of GDP). Furthermore, Italy may exit the Excessive Deficit Procedure in the first half of the year, potentially activating the escape clause that would allow defence spending to be increased for four years up to a maximum of 1.5% of annual GDP. Consequently, growth in 2026 would be 0.8% and could exceed 1.0% in 2027.

- 1

In March 2025, a modification to the constitutional debt brake rule was approved in order to fund an infrastructure plan (SVIK, by its German acronym), with a budget of 500 billion euros for the next 12 years, and to increase defence spending from 2.0% of GDP in 2024 to 3.5% by 2029, according to NATO criteria. Investments financed by the SVIK fund do not count for the purposes of the debt brake.

- 2

NATO's definition of «defence spending» is broader, as it considers all expenses incurred to cover all the needs of the armed forces, regardless of the ministry in which they are generated (pensions, R&D expenditure, transport, cost of overseas missions, etc.). The defence spending that appears in the budgets is lower, as it uses internal criteria and, for example, excludes spending by other ministries and military pensions.

- 3

Some criticisms of the plan are: that it does not serve to fund new investment projects but rather pre-existing ones, that part of it is allocated to funding current expenditure, and that investments have been removed from the ordinary budget in order to be financed with SVIK funds. See «German Council of Economic Experts», Annual Report 2025/26, chapter 2.

- 4

Given the behaviour of the public accounts in 2025, and assuming that the magnitude of the increase in the structural fiscal deficit outlined in the 2026 budget is maintained, the fiscal stimulus in 2025 and 2026 would be around 1.0 pp, almost half of what it would have been had the 2025 forecast been met. Assuming multipliers of between 0.4 and 0.8, the boost to growth would be between 0.4 pps and 0.8 pps.

The US faces another year with a positive outlook

The US economy will accelerate its growth rate in 2026, kicking off the year with a rebound as part of the loss of activity experienced in Q4 2025 due to the shutdown will be offset. Investment will continue to drive growth thanks to the development and deployment of AI. The dynamism of spending among higher-income households will more than offset the restraint shown among lower-income households, consolidating the narrative of a K-shaped growth pattern in private consumption. Overall, growth in 2026 is expected to reach 2.6% (2.2% in 2025). Inflation, meanwhile, will continue to resist falling to the 2% target, sustained by tariffs and economic dynamism. Thus, both headline and core inflation will remain closer to 3% than 2% on average in 2026, following a rate of 2.6% in 2025.

Risks

The risks to the baseline global scenarios have increased significantly following the joint US and Israeli attack on Iran, which has triggered a surge in oil and gas prices and turmoil in the financial markets. The final impact of this conflict will depend on its duration and geographical scope. If the energy price increase currently reflected in the futures market materialises (a short-term risk premium, buteasing over the following quarters), then the forecast growth for the euro area would be reduced by a few tenths of a percentage point, but there would not be any change of narrative that would alter the medium-term trends. Inflation could experience a temporary uptick, but without deviating from the target in a concerning manner, so this would not affect the strategy of the ECB, which feels comfortable with the depo rate at 2.00%. In the US, higher energy prices have an asymmetric impact: they increase inflation but also improve the trade balance and growth (the US is a net exporter of oil and gas). This combination would favour a somewhat more restrictive bias for the Fed, reinforcing the view that it is in no hurry to cut rates again.

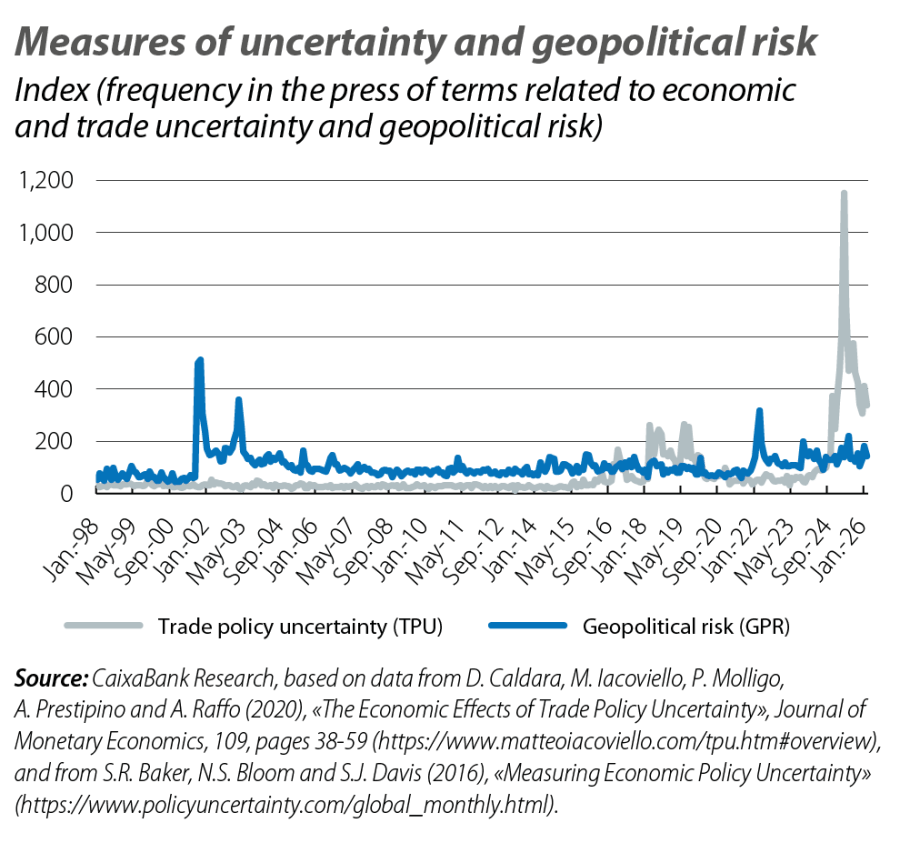

The conflict in Iran adds to the existing ones: Ukraine, limited fiscal space in industrialised economies and a risk of sharp corrections in financial markets due to high expectations and valuations linked to AI companies. Also, the intensification of trade uncertainty following the Supreme Court’s blow to many of the tariffs implemented by Trump should be noted as a significant risk to the scenario (see «10 questions about the US Supreme Court’s tariff ruling» in this same Monthly Report).