Artificial intelligence: a supply-side perspective

While the development of artificial intelligence dates back to the 1950s-60s, advances in the past decade have driven more recent developments in so-called generative AI, capable of producing text, code and audiovisual material based on patterns learned from large datasets. The deployment of AI can be divided into four key phases: innovation, development of new infrastructure, diffusion and widespread adoption of the new technology, and adaptation of business models and markets to the new technology.

Artificial intelligence (AI), in a broad sense, is the ability of machines and computational systems to replicate human intelligence in the perception, synthesis and inference of information, thereby performing tasks which previously could not be carried out or traditionally required human cognitive abilities, such as language comprehension, pattern recognition and decision-making.

While the development of this technology dates back to the 1950s-60s, advances in large language models (LLMs) over the past decade, along with improvements in processing power and mass data collection, have driven more recent developments in so-called generative AI, capable of producing text, code and audiovisual material based on patterns learned from large datasets.

The AI value chain: complex and heterogeneous from country to country

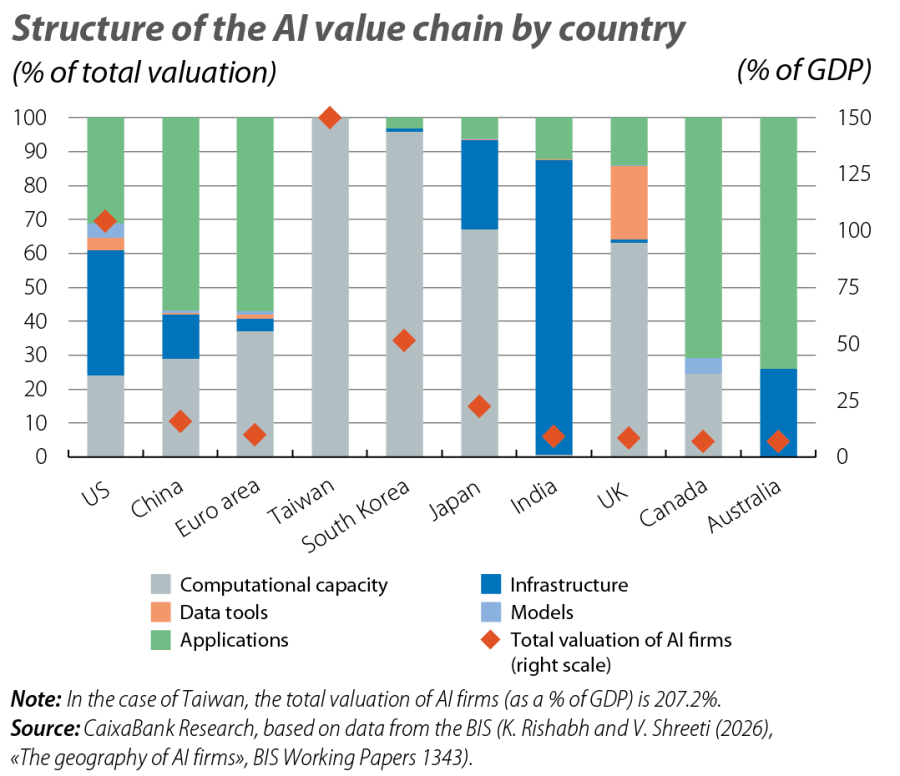

The development of AI relies on a complex value chain composed of several interdependent links.1 At its core lies access to critical minerals used in the manufacture of semiconductors, the «physical brain» of AI. These components are integrated into a broader computational infrastructure comprising data centres, communication networks, power grids and cloud computing services, together forming the «body» that enables large-scale data processing. On top of this infrastructure lies access to large volumes of data for training models. The development of so-called foundational models represents in itself the next link in the chain and requires sophisticated algorithms and neural networks for deep learning. Finally, the value of generative AI is realised in the development of specific applications built on foundational models, such as virtual assistants or content generation systems, and in its integration into digital products and services, which are the main point of contact with the end user.

Currently, AI value chains vary widely across the major economies (see first chart). On one hand, in the US and several Asian nations the sector plays a significant role in the economy, measured in terms of AI firm valuations as a percentage of GDP. Among these, Taiwan and South Korea are highly specialised in computational capacity, while the US has a more diversified value chain. On the other hand, in China and several advanced economies, AI plays a somewhat smaller role in the economy and they also have different specialisations. Japan and the United Kingdom show greater specialisation in computational capacity (and data tools, in the case of the latter), while in China and the euro area there is a greater emphasis on applications.

- 1

See O. García Retuerta and D. García Retuerta (2026), «La cadena de valor de la inteligencia artificial: estrategias de autonomía para España», IEEE Opinion Document 03/2026, Spanish Ministry of Defence, Spanish Institute for Strategic Studies; and McKinsey & Company (2023), «Exploring opportunities in the generative AI value chain», QuantumBlack, AI by McKinsey.

AI deployment, from innovation to adaptation

The deployment of AI can be divided into four key phases: the innovation phase, the development of new infrastructure, the diffusion and widespread adoption of the new technology, and the adaptation of business models and markets to the new technology.

In this context, the global economy is still immersed in the first two phases of AI deployment. There is ample evidence of an investment boom related to innovation and infrastructure construction, which is particularly evident in countries such as the US and some Asian nations.2 In this context, AI capabilities are improving at an exponential rate. This progress is being supported by hyperscaling, driven by rapid advances in the amount of data used to train models, the number of parameters, and computational capacity. At the same time, the surge in supply and demand is creating infrastructure bottlenecks.3

- 2

See the article «The AI buzz in financial markets», in this same Dossier.

- 3

For example, METR, a metric which measures AI performance based on the maximum task length (time horizon) a model can handle, shows that in recent months it can now satisfactorily perform tasks that would require several hours, whereas a year ago models could only handle tasks with a duration of minutes. See also «The AI Index 2026 Annual Report», by Stanford University’s Institute for Human-Centered AI. The main infrastructure bottlenecks are found in the chip market, but also in data centre capacity and in the energy market.

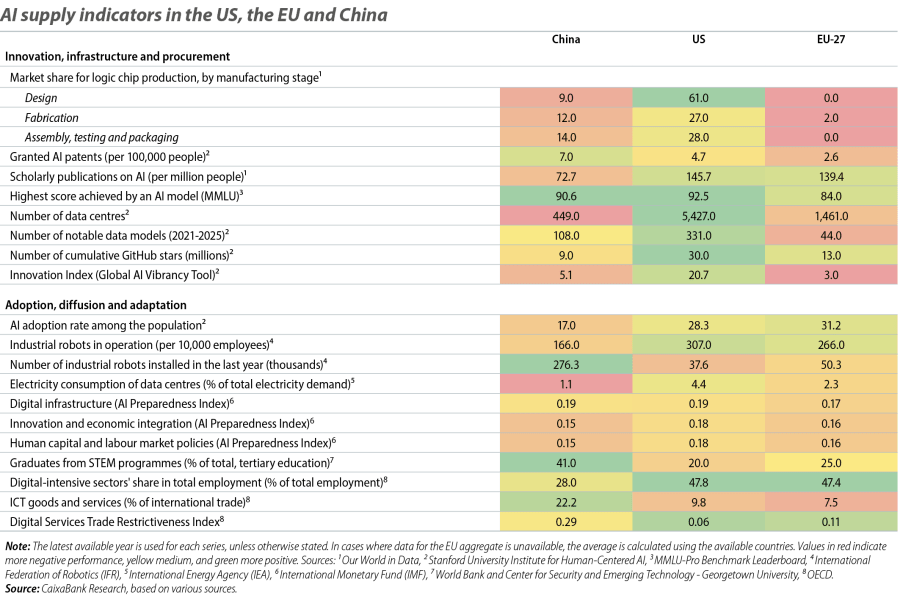

As has been the case with other technologies in the past, some economies will not play a decisive role in the innovation phase, but will benefit from adoption, diffusion and adaptation to the technology. If we focus on the comparison between the US, the EU and China, we can see important nuances in different phases of the deployment process. In the innovation phase, the US economy is taking a clear lead, as is particularly evident in indicators related to output (such as the performance of models at the technological cutting edge, academic publications and open-source development) and infrastructure (such as the number of data centres and chip design). Yet China has shown a remarkable ability to catch up with the technological frontier in recent years. Its most advanced models show a very similar level of performance to their American counterparts, while the dynamism observed in the granting of patents and the development of models points to a boom in innovation. The EU, meanwhile, is not so well positioned in terms of innovation, according to most indicators. In particular, its low market share in chip production makes it highly dependent in this sphere, while it is lagging behind China and the US in the development of AI models. Finally, China is leading in the supply of materials, due to its access to critical minerals and its processing capacity for chip and semiconductor manufacturing.4

In indicators related to adoption, diffusion and adaptation, the picture is somewhat more homogeneous. Adoption in the three major economies, in terms of the proportion of the population currently using AI, stands at around 30% in the EU and the US, while for China it is just under 20%.5 Similarities are also found in their degree of readiness for adoption, diffusion and adaptation, albeit with a slight advantage for the US. On the other hand, in recent years China’s manufacturing sector has undergone a very rapid modernisation – and «robotisation» – process, anchored in an aggressive industrial policy and significant investment in infrastructure and human capital. This places it in a strong position to benefit from the difussion of and adaptation to AI, especially as a global supplier of advanced technologies. Finally, the European and US economies are more intensive in digital services, positioning them as potential leaders in the adaptation phase, the speed and magnitude of which will be key to determining the macroeconomic effects of AI.6

- 4

See «China’s alchemy: how it transforms critical minerals into global power» in the MR01/2026.

- 5

These are significant figures that indicate a substantially higher adoption rate than that of previous technologies. Business adoption figures, meanwhile, show greater dispersion by function, sector and degree of implementation. See «The AI Index 2026 Annual Report», by Stanford University’s Institute for Human-Centered AI.

- 6

For further details, see the article «Productivity and employment in the face of generative AI: what do we know?», in this same Dossier.

The global economy, in the early miles of the AI marathon

The «AI race» is still in its early stages. While the US has taken the lead in the innovation phase, the pack is closing in, led by China, and it is unlikely that the race will be decided between just two participants. Given its transformative potential, the success of the deployment of AI and its macroeconomic impact will depend on the business sector’s ability to adapt and manage the frictions associated with this new technology. However, AI will also require an active role from states, both in its regulation and in its adoption, diffusion, adaptation and coordination at a global level, promoting the necessary improvements in terms of institutions, infrastructure and human capital.7 The task ahead is complex and will require new tools of public policy and economic diplomacy. Moreover, the AI supply model that is ultimately adopted – whether in fragmented blocks centred around the US or China, or more integrated globally – will have implications that extend beyond the economy. The AI marathon is only just begun, and everyone is taking part.

- 7

For further details, see the article «Differentiated strategies for governing AI: towards cooperation or conflict?», in this same Dossier.

Geopolitics

We analyse the major geopolitical trends and thier effects on the financial markets and the economy.

Digitalisation & Technology

The keys to understanding how digitalisation and new technologies are substantially transforming the economy and how society works.