The AI buzz in financial markets

The rise of AI has led to hopes of a new industrial revolution and, at the same time, fears of another bubble. This ambivalence extends to stock market valuations: they rest on expectations of vast revenue growth, but at the same time, there are doubts about their sustainability, either because the expectations themselves may disappoint or due to the eye-watering spending and investment plans being drawn up by firms in the sector.

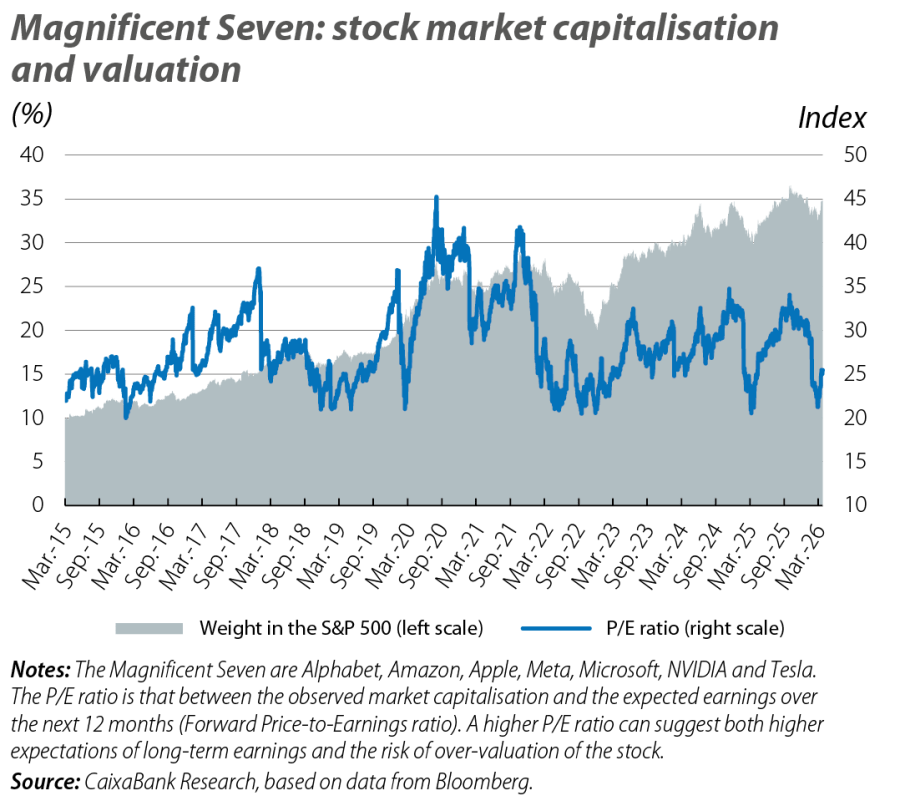

Artificial intelligence (AI) has accounted for much of the recent economic growth1 and stock market performance in the US. Since the emergence of ChatGPT three years ago, the so-called Magnificent Seven2 account for 60% of the cumulative increase in the market capitalisation of the S&P 500 and now represent around 35% of the index. The rise of AI has led to hopes of a new industrial revolution and, at the same time, fears of another bubble. This ambivalence extends to stock market valuations: they rest on expectations of vast revenue growth, but at the same time, there are doubts about their sustainability, either because the expectations themselves may disappoint or due to the eye-watering spending and investment plans being drawn up by firms in the sector.3

- 1

See the article «Productivity and employment in the face of generative AI: what do we know?», in this same Dossier.

- 2

Alphabet (Google), Amazon, Apple, Meta, Microsoft, NVIDIA and Tesla.

- 3

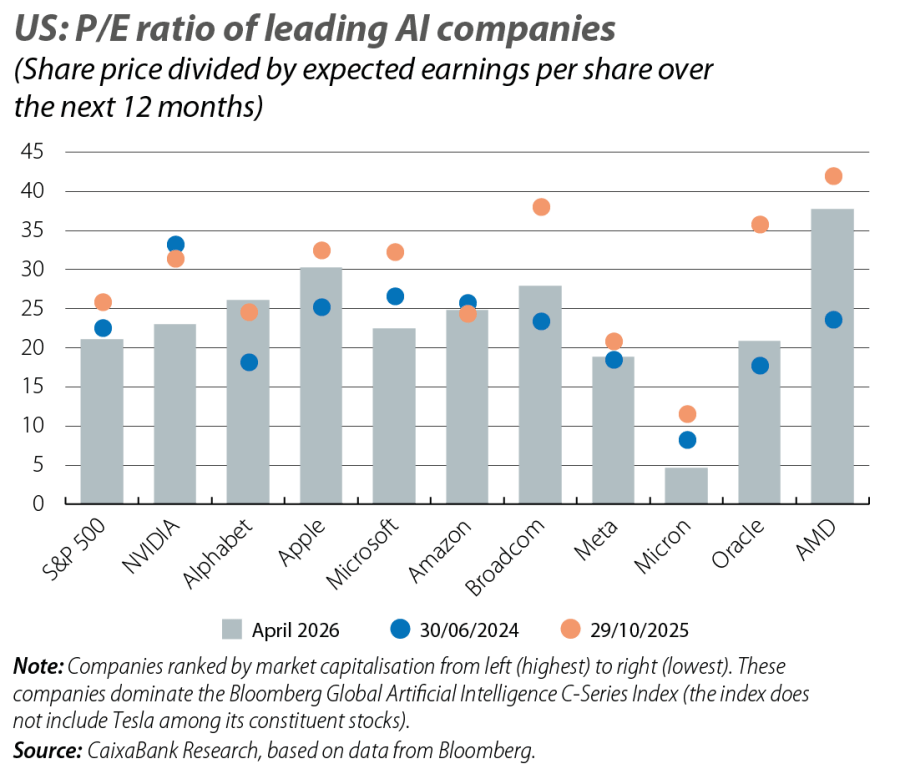

This ambivalence is reflected in the P/E ratios (price per share divided by earnings per share, a standard valuation metric) shown in the first two charts: tech firms have above-average P/E ratios, but they have experienced corrections in recent months.

The role of market structure

Although the Magnificent Seven are considered global leaders in AI today,4 one of the questions for determining whether they will be able to monetise their vast investment plans in time is the shape that the AI market will take and which companies will emerge as winners and losers when the technology matures.

The AI value chain provides insights into the potential evolution of the market. This chain has five layers.5 Firstly, computing power, with the design of microprocessors and memory chips that manage intensive calculations, where NVIDIA currently stands out in design and TSMC in production. Secondly, infrastructure, with data centres and cloud services and a notable presence of Amazon (Amazon Web Services) and Microsoft (Azure). Thirdly, datasets (images, text, audio) for training AI. The fourth link is large AI models, such as OpenAI's GPT or Anthropic's Claude, which can be adapted to a wide range of tasks. The final layer is applications that adapt these large models for specific use cases, such as Copilot, ChatGPT or Claude Code.

Generally speaking, the current technology involves significant investment needs and high fixed costs, which can create barriers to entry in the AI value chain. This applies especially to the first two layers, where network effects are also observed that reinforce the competitiveness of incumbent firms against potential new entrants. The last three layers (data, models, and applications) are, a priori, more open to competition (training with public data, open-source code for models and applications), but they also exhibit dynamics that may favour market concentration. For example, if public data as a training source become exhausted (something various experts see as imminent), it will be necessary to resort to private data. Here, established companies such as Meta, Google or Microsoft could reinforce their competitive advantage thanks to the high volume of users of their applications (social networks, such as Instagram or LinkedIn, navigation [Google Maps] or office software [Microsoft 365]).

The complementary connections between the different layers in the chain also favour the dominance of firms that encompass multiple layers in the AI value chain – an integration already exhibited by the established big tech firms. For example, Google also produces its own hardware (TPU chips), builds models (Gemini) and integrates its products with one another.

A step change in investment needs

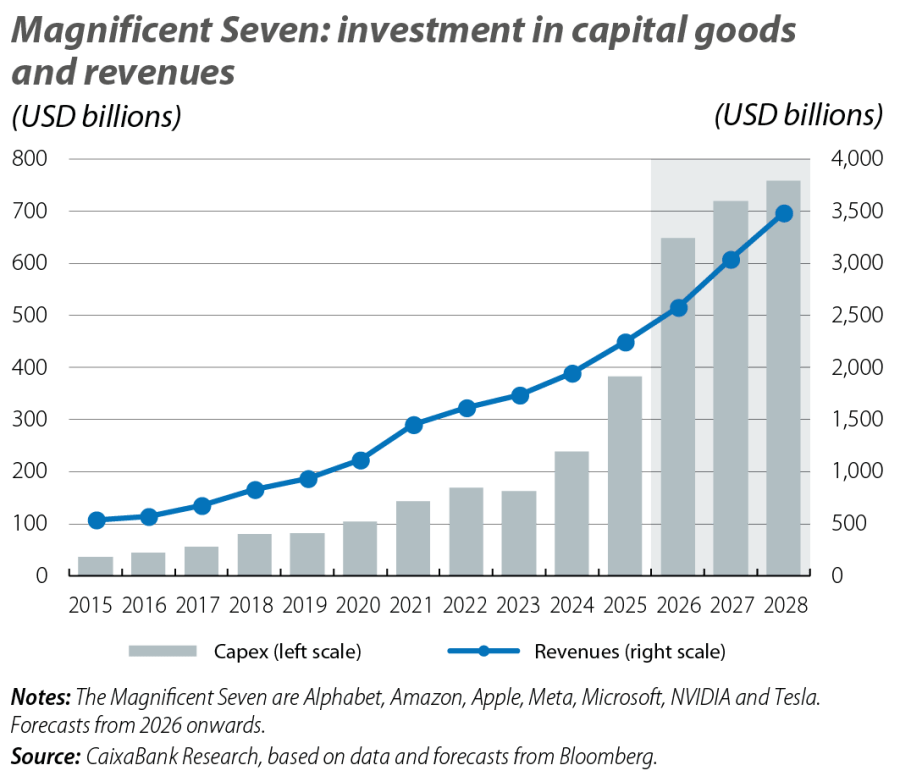

AI not only requires cutting-edge research but also vast investment in infrastructure, particularly related to the computational needs for storing data and training and using models. This investment includes data centres, computer servers, cooling systems, energy facilities, etc. Among the Magnificent Seven, this investment ambition has translated into capex growth of 50% and 60% in 2024-2025, accelerating to 70% in 2026, according to estimates and forecasts by Bloomberg's analyst consensus.

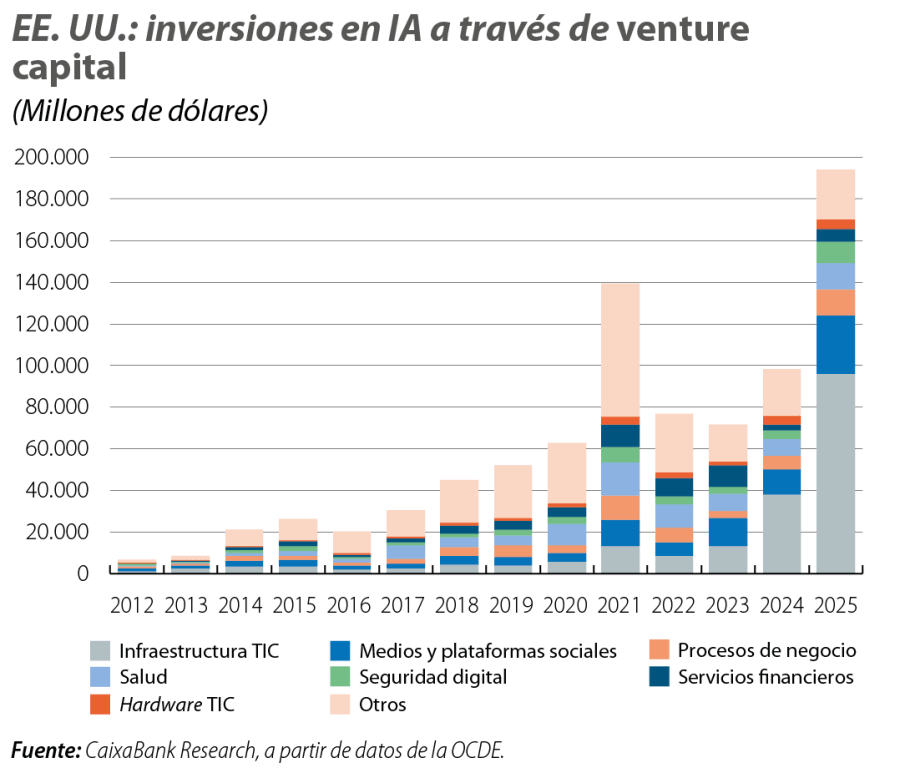

The sharp growth in investment has led to a shift in financing strategies. In recent years, tech firms have taken advantage of their low debt ratios and highly profitable operations to fund their investments with the cash flow they themselves generated. But their spending plans have grown so much that they have become more reliant on external financing (corporate bonds, loans and private credit and venture capital6).7

A common structure for obtaining external financing links data centres, private equity, and cross-investments among large AI firms.8 Typically, this formula involves forming a consortium of actors to create a new entity, which will own data centres. That consortium includes, as a minority shareholder, the AI company itself which will pay the rent and operate the data centres. To obtain financing, the entity issues debt, often channelled through private credit9 or institutional investors, and the servicing of that debt is backed by the income generated from the rental of the data centres. According to the Bank for International Settlements itself,10 this structure can create circularity and opacity around AI firms’ actual level of indebtedness. Furthermore, it tends to create links between the established major AI firms (when they converge in consortia), just like in other cross-investment operations among the leading companies.11

Overall, the current AI value chain and the financing strategies and strategic deals between established tech firms exhibit traits that are conducive to market concentration and dominance by incumbents. Besides helping to explain current market valuations, such concentration could pose a source of instability.12 Nonetheless, how the AI market will actually develop remains uncertain and could result in very different configurations. Regulation, the ease of building new models, and supply dependencies (such as specialised chips) will be key to determining its final structure.

- 8

Eren et al. (2026). «Financing the AI infrastructure boom: on- and off-balance sheet borrowing», Bank for International Settlements.

- 9

i.e. non-bank credit granted by specialist investment funds, negotiated directly between lender and borrower.

- 10

Eren et al. (2026), op. cit.

- 11

Bloomberg (2026). «A Guide to the Circular Deals Underpinning the AI Boom», describes various such circular arrangements. e.g. in 2025 NVIDIA agreed to invest 100 billion dollars in OpenAI, while OpenAI committed to operating its data centres intensively with NVIDIA chips. OpenAI and AMD also formed a strategic alliance whereby OpenAI could end up becoming a major shareholder of AMD and, at the same time, committed to purchasing AMD chips worth tens of billions of dollars.

- 12

For example, by exposing a large portion of the economy to the difficulties of a handful of agents or to bottlenecks, or by increasing the correlation between agents (e.g. correlated market movements that amplify moments of stress). S. Breeden (2024), Engaging with the machine: AI and financial stability, speech at the HKMA-BIS Joint Conference on Opportunities and Challenges of Emerging Technologies in the Financial Ecosystem.

Digitalisation & Technology

The keys to understanding how digitalisation and new technologies are substantially transforming the economy and how society works.