Productivity and employment in the face of generative AI: what do we know?

Generative artificial intelligence (AI) has traits of a general-purpose technology: applications in many sectors, rapid improvement of the technology itself and a catalyst for complementary innovations. This has already happened with technologies such as electricity and the internet. Even so, having high potential does not necessarily mean an immediate or uniform macro impact. The final magnitude of AI's impact will depend on the speed of its adoption and the ability of firms to reorganise processes. This article examines how AI could affect productivity growth and what it means for the labour market.

Striking productivity increases at the micro level

Since the emergence of ChatGPT in 2022, research on the impact of AI on worker productivity has surged. A review by the OECD indicates that, on average, using AI tools can boost individual productivity by around 30%, and some studies find improvements exceeding 50% in specific tasks.1,2 Many of these studies, conducted in controlled environments where one group of workers is given access to the tool and another is not, find vast productivity improvements in tasks where the technology has a direct application, such as programming or writing.

These results should not be read as an automatic estimate of the impact on the entire economy. Firstly, they focus on specific tasks, and secondly, they often exclude implementation costs (training, process adaptation, organisational changes, legal or technical frictions). In short, they show what AI can do under favourable conditions, but not necessarily what it will do immediately on an aggregate scale. Even so, they represent a floor. As the technology advances, further improvements can be expected, and the evidence available to date suggests a rapid rate of improvement. Many of the available studies, for example, were conducted before the arrival of autonomous AI agents capable of executing complete tasks without human intervention; if this type of solution becomes widespread, then the productivity gains could increase substantially. There is also a pattern that is repeated in many jobs: among workers performing the same task, AI tends to be of greater help to those who started with a lower level of productivity. In this regard, it acts as a «leveller».

- 1

«Macroeconomic productivity gains from Artificial Intelligence in G7 economies», OECD Artificial Intelligence Papers, June 2025, nº 41.

- 2

The productivity metric varies according to the study. In some cases, it refers to time savings, while in others it refers to increases in production within the same time interval. In general, they can be interpreted as savings in labour costs.

The leap from micro to macro is not automatic

Small-scale advances do not always translate into macro figures. If AI were to have a big impact on a few occupations, then the overall impact could be limited. The Nobel laureate in Economics, Daron Acemoglu, proposes a simple framework for considering this leap.3 AI boosts productivity in two ways: it automates tasks (replacing human labour) or it complements workers (enabling them to do more and better). Both increase productivity, but with different implications for employment, wages and inequality.

Under certain assumptions, the author shows that the impact of AI on aggregate productivity can be approximated based on two ingredients: (i) the proportion of tasks or occupations actually affected by the new technology and (ii) the average productivity gain in those tasks.4 Unfortunately, there is significant uncertainty regarding the magnitude of both of these ingredients.

For instance, Acemoglu assumes that 20% of tasks are susceptible to being automated and that, among these, it will only be economically viable to automate 23% of them within the next 10 years. Other authors find higher figures, with 60% of tasks being susceptible to automation and 80% viability among these cases.5

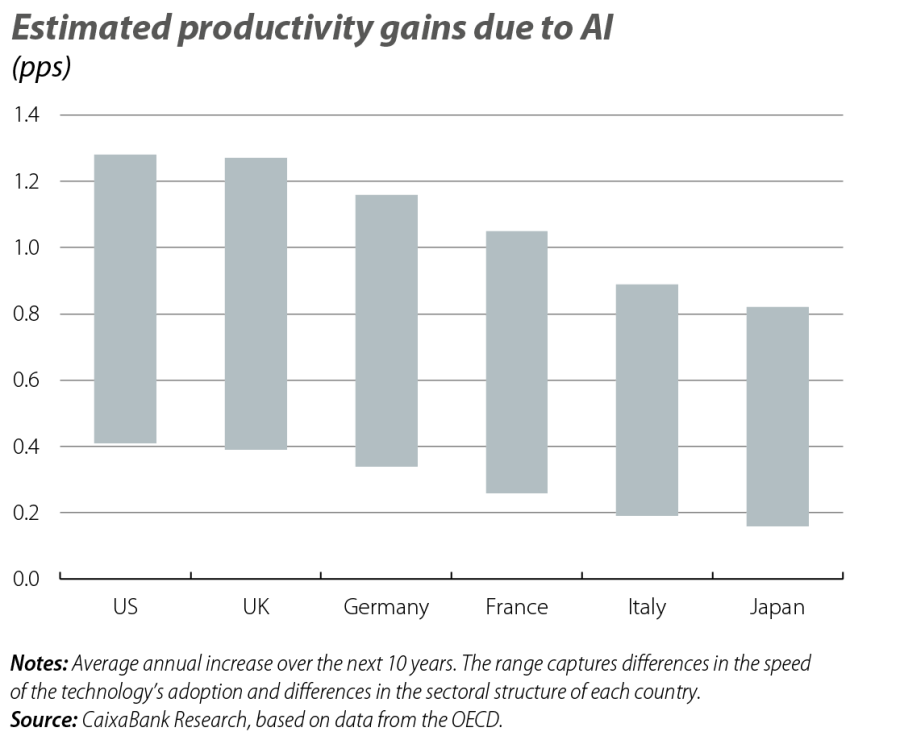

Aggregate estimates vary significantly depending on assumptions about the proportion of tasks affected and the average productivity gains. At one end of the spectrum, Acemoglu suggests modest productivity gains of around 0.1 pp per year. With more favourable assumptions, the figures are higher. For example, the OECD estimates that, over the next 10 years, annual productivity growth will increase by between 0.4 and 1.3 pps in the US and by between 0.2 and 0.8 pps in other advanced economies.6 These are broad ranges, depending on different assumptions about the speed of the technology’s adoption and the sectoral structure of each economy, but in no case are they negligible figures.

These exercises do not exhaust all impact channels. AI can facilitate new occupations and business models, and could accelerate scientific innovation. The OECD, for example, notes signs of a virtuous circle of innovation: there is an increase in generative AI patents cited in developments in other fields and, in turn, an increase in generative AI patents that cite innovations from other fields that cited generative AI patents.7 In other words, AI facilitates innovation in other fields and these accelerate innovation in AI itself.

The adverse effects also need to be included. The economy does not always function as the sum of isolated tasks. A simple example is the so-called Baumol effect: if productivity increases significantly in some sectors but little in others, wages tend to move similarly across sectors. Otherwise, workers would end up moving to where the pay is better. In order to retain them, less productive sectors have to raise wages, even if they do not produce more. The rise in wages in these sectors translates into higher prices and, therefore, the weight of these sectors on final expenditure increases and dilutes the impact of the productivity gains in the more advanced sectors. OECD simulations suggest that this effect could subtract around one-sixth of the potential increase in productivity growth associated with AI.8

Furthermore, AI can have harmful uses – disinformation, manipulation, cyberattacks or addictive advertising – that generate negative externalities. If these costs are not reflected in standard metrics, macro gains may overestimate the social benefits.

- 3

D. Acemoglu (2025). «The simple macroeconomics of AI». Economic Policy 40, nº 121, pages 13-58.

- 4

Economic literature distinguishes the concept of a task from that of an occupation. An occupation is a set of tasks, and the automation of a task does not necessarily mean that the occupation is automated. For the sake of simplicity, in this article we will use the words task and occupation as synonyms.

- 5

For a review of the estimates made, see P. Aghion and S. Bunel (2024).«AI and Growth: Where do we Stand?», Policy Note.

- 6

See footnote 1.

- 7

«Is Generative AI a General-Purpose Technology? Implications for Productivity and Policy», OECD Artificial Intelligence Papers, June 2025, nº 40.

- 8

The impact is greater the more unequal the productivity gains are between sectors and the greater the difficulty households have in redirecting their spending towards more productive sectors.

The labour market: a great unknown

The net effect of AI on employment is ambiguous. On the one hand, automation reduces the demand for labour in the affected tasks. On the other hand, new technologies also create new jobs – the reinstatement effect. This is an important channel. In the four decades following the Second World War, the emergence of new occupations completely offset job destruction due to automation.9 The big question is whether AI will replicate that pattern and at what pace. There is also a third channel: by boosting productivity, AI could result in lower costs, lower prices, and better products, which could stimulate demand and, therefore, the demand for labour too.

Wage inequality does not follow a single direction either. Unlike other technological waves, such as robotics, which disproportionately affected certain groups, exposure to AI seems to be relatively widespread across occupations of different skill levels, potentially limiting the increase in wage inequality. The IMF notes, however, that higher-income workers are, on the one hand, those at greater risk of having their jobs replaced by AI, but at the same time, those with more potential to benefit from its complementarity.10

The institution simulates three scenarios and finds that the effect of AI on wage inequality depends on whom it helps and whom it harms more: if task substitution dominates, inequality could decrease (because higher-paid jobs would be more affected). If complementarity prevails, inequality would tend to increase (because workers with higher qualifications would benefit more). And if AI increases aggregate productivity, wages can rise for everyone, but more so for those who benefit from greater complementarity with AI, once again widening the gap.

- 9

D. Acemoglu and P. Restrepo (2019) «Automation and new tasks: How technology displaces and reinstates labor», Journal of Economic Perspectives 33, nº 2,

pages 3-30. - 10

M. Giovanni, A. Panton, C. Pizzinelli, E. Rockall and M.M. Tavares (2024). «Gen-ai: Artificial intelligence and the future of work». IMF, 979, pages 1-37.

Competition will be a key element

The distribution of the benefits will also depend on the competitive environment. AI can reduce barriers to entry in some markets. Cheaper tools for programming, translating, designing or analysing data can enable small businesses to do things that previously required greater scale. In competitive markets, part of the profits would translate into lower prices and more widely distributed benefits. If, on the other hand, companies capture most of the income – through patents or market power – then the distribution may be unequal.

This tension is particularly relevant in the AI market itself. Economies of scale (larger size, greater efficiency), economies of scope (a single model can be adapted for multiple uses at a relatively low cost) and bottlenecks in access to data to train models, as well as the cost of computing and human capital, naturally drive this market towards greater concentration. It is not inevitable, but it is a plausible risk. Oversight by authorities will therefore be important: not to hinder innovation, but to prevent a technology with the potential to enhance well-being from being sequestered by excessively closed market structures.

In summary, AI will be transformative. Its potential to increase productivity is real, but its deployment will be gradual. Initially, time-saving in specific tasks will prevail. The most significant changes will come later, when companies redesign entire processes and when AI helps accelerate the generation of knowledge and new ideas.

The most reasonable scenario is thus one of increasing benefits in the medium term. This increase will be more intense and rapid in the US than in Europe, given the faster pace of technological adoption and the prominence of the tech sector in the US compared to Europe.11 In this context, it seems plausible to expect productivity improvements of up to 1 pp annually in the US over a 5 to 10-year horizon, and about half of that in Europe. This would not be an instant revolution, but it would represent a step change for growth.

- 11

For further details, see the articles «Artificial intelligence: a supply-side perspective» and «Differentiated strategies for governing AI: towards cooperation or conflict?», in this same Dossier.

Digitalisation & Technology

The keys to understanding how digitalisation and new technologies are substantially transforming the economy and how society works.