AI adoption in Spanish firms is advancing rapidly but remains limited and uneven

The adoption of artificial intelligence (AI) in Spanish firms has accelerated in recent years, but the process has been uneven and remains incomplete. This article analyses the extent of AI penetration considering four key dimensions: company size, sectoral differences, specific uses within organisations and the main barriers hindering its deployment, as well as a comparison with the rest of Europe. Understanding how and where AI is being incorporated is particularly important from a business and macroeconomic perspective, as its adoption influences efficiency and productivity gains and can widen gaps between firms, sectors and workers in a productive fabric like Spain’s, which is dominated by SMEs and microenterprises.

Business adoption: size matters

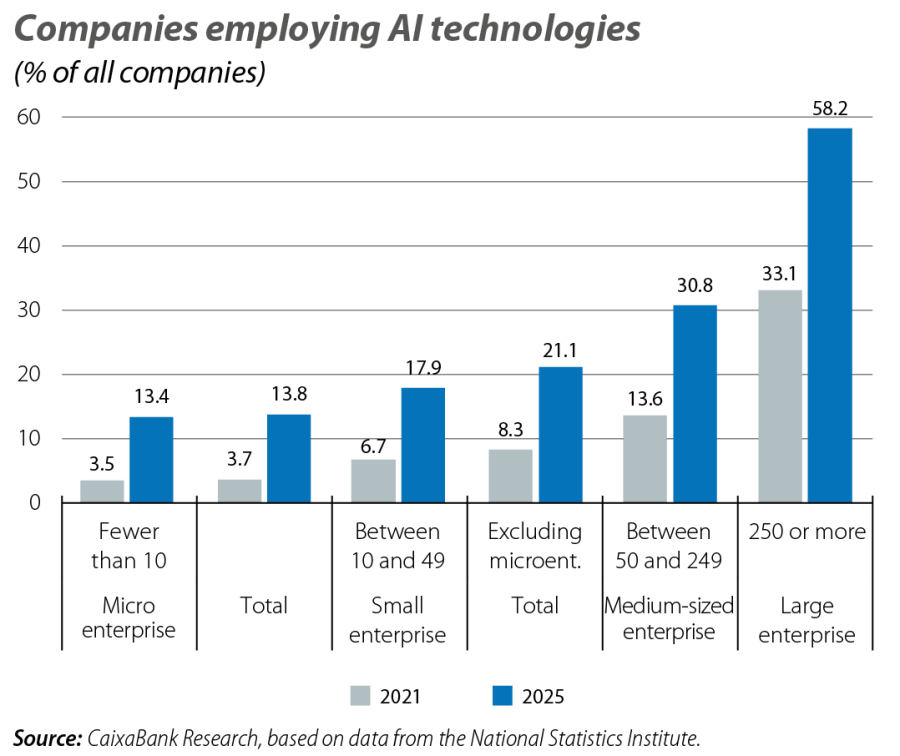

Between 2021 and 2025, the adoption of AI technologies in Spain’s economy has more than doubled in firms with over 10 employees,1 going from 8% to 21%, suggesting that AI is no longer an experimental technology. Nevertheless, in 2025, nearly 8 out of 10 firms were still not using it, suggesting that widespread adoption has not yet occurred.2

- 1

Excluding companies with fewer than 10 employees is also the most commonly used metric for international comparison purposes.

- 2

For this analysis of the adoption of AI tools by Spanish firms, we use data from the National Statistics Institute’s Survey on the Use of ICT and E-commerce in Enterprises. Given that the survey separates companies with fewer and more than 10 employees, the total figure is obtained by weighting both groups according to the business structure (National Statistics Institute’s Central Business Register): according to our calculations, AI adoption rises from 4% in 2021 to 14% in 2025.

The first key conclusion is that company size is a decisive factor. AI is present in nearly 3 out of every 5 large firms, but only in 18% of those with fewer than 50 employees. This gap reflects barriers that go beyond technology, related to financial resources, the availability of data, qualified personnel and organisational capacity.

These differences have not diminished in the period 2021-2025. Although adoption is growing across all company sizes, progress has been far more rapid in large firms (+25 pps) than in small ones (+11 pps). Medium-sized companies (between 50 and 250 employees) reflect a turning point: their level of adoption (31%) is significantly higher than that of small businesses (18%), suggesting they meet a threshold of sufficient resources to experiment with AI.

If microenterprises were included in the analysis, the aggregate adoption rate would fall considerably: instead of 21%, it would be 14%, as these entities have a very low adoption rate (13%) and account for 95% of Spain's productive fabric.3

- 3

It is also interesting to look at adoption not in terms of companies, but employees. Weighted by employment (and including all companies, even microenterprises), it is estimated that in 2025 around 31% of workers in Spain were employed in companies using AI technologies. This is because adoption is concentrated in medium and large enterprises, which account for a much larger proportion of total employment. This result is obtained by combining AI adoption rates by company size with data on job distribution by size, according to the European Commission’s 2025 SME Country Fact Sheet (Eurostat/JRC).

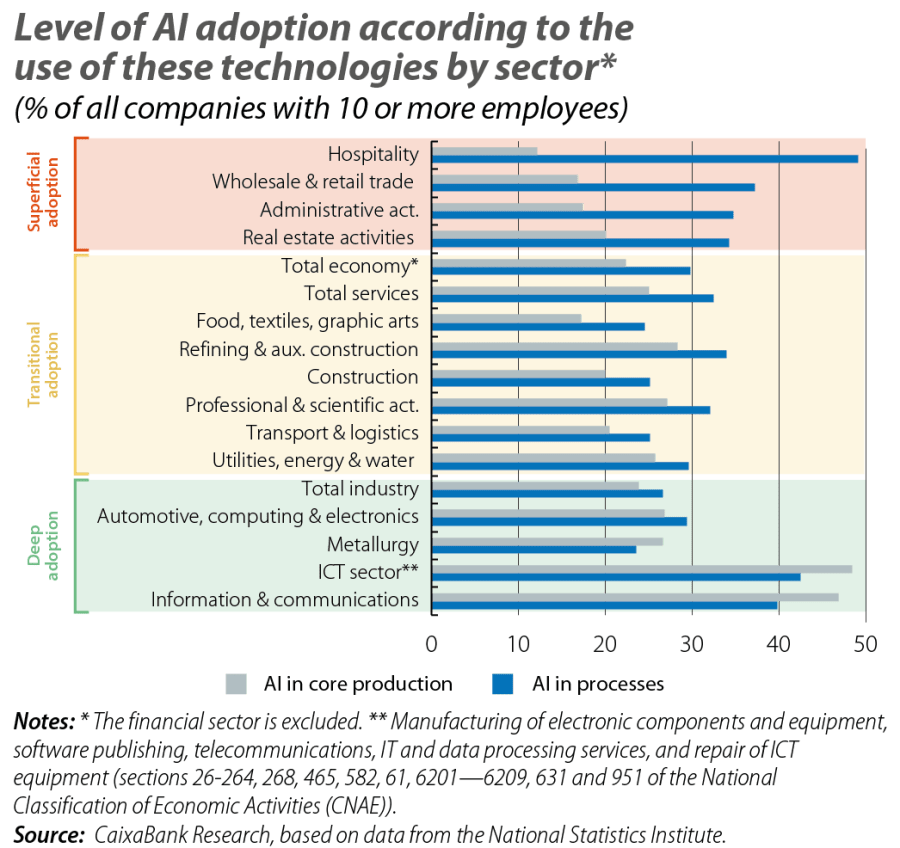

Highly mixed picture of AI adoption by sector

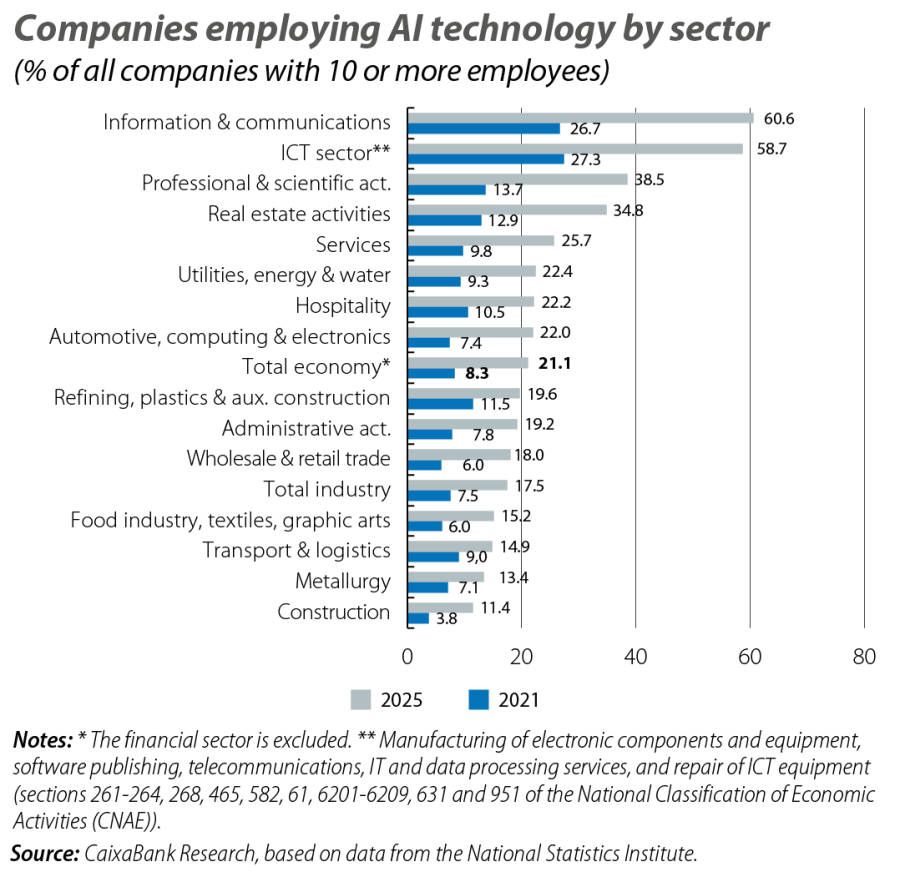

In 2025, the sectors with the highest adoption of AI were information and communications and the ICT sector,4 with percentages of around 60% – significantly above the levels observed in 2021 (26-27%). In these sectors, AI has become quite prevalent, in line with their greater intensity in intangible capital, the availability of data and their proximity to technological supply.

In a second tier are knowledge-intensive services, such as professional and scientific activities (38.5%) and real estate activities (35%). Thirdly, a wide range of sectors show moderate adoption levels, at around 20%-26%, spanning both services and industry: basic supplies, hospitality and the automotive and electronics sectors.

At the lower end we find construction, metallurgy, and transport and logistics, where adoption remains low. Overall, although some sectors are approaching widespread AI usage, the economy remains in an intermediate phase, with significant margin for future dissemination concentrated in the sectors and firms that are lagging the furthest behind.

- 4

The ICT sector includes activities such as the manufacture of electronic components and equipment, software publishing, telecommunications, IT and data processing services, and the repair of ICT equipment (sections 261–264, 268, 465, 582, 61, 6201–6209, 631 and 951 of the National Classification of Economic Activities (CNAE)).

What are our companies using AI for?

The next issue is to identify the specific functions for which AI is being used in each sector. To this end, we distinguish between two major types of applications. On one hand, we find AI used in processes, aimed at improving organisational and commercial efficiency, such as internal management, administrative tasks or sales support. On the other hand, there is AI linked to the productive core, that is, uses applied directly in the production of goods or in the provision of the main service.5

In this context, adoption is considered superficial when AI is primarily used in processes rather than in the production of goods or services; and it is considered deep when AI is employed to a greater extent in production rather than in management tasks. There is another group of sectors where AI adoption is currently in a transition phase, moving from its use in processes towards greater use linked to production. Most of the adoption in sectors such as hospitality, commerce and administrative activities is found in processes. In these cases, AI is initially introduced in cross-functional management and commercial support roles, where implementation costs and organisational risks are lower, before extending to the productive core.

- 5

We consider process AI to include uses in business administration and management, marketing and sales, accounting and finance, ICT security, and support for information analysis. Conversely, production AI is considered that directly linked to the production of goods, the direct provision of services, logistics and operations, as well as advanced R&D, such as automation, simulation and process optimisation.

In an intermediate position we find sectors such as food and textiles, professional and scientific activities, and construction, with a transitional adoption where both types of uses coexist. AI is beginning to permeate operational decisions, but it does not yet play a dominant role in core business activities.

Finally, sectors such as information and communications and the ICT sector show a high level of adoption both in processes and in the productive core. In these fields, AI is not merely an efficiency tool but an integral part of the product, service and digital infrastructure.

Overall, the pattern observed suggests that the recent progress in adoption within the Spanish economy has been primarily driven by horizontal uses, which are quick to implement, low-cost, and more oriented towards administrative tasks than production processes. This is consistent with what Daron Acemoglu has documented for the US, where improving quality and the reliability of processes is the main motivation for adopting AI.6 The big unknown for the impact on aggregate productivity is when the use of AI will become widespread in operational and core business uses, which require greater integration, investment, and the redesign of processes.

- 6

See D. Acemoglu et al. (2022). «Automation and the workforce: a firm-level view from the 2019 annual business survey». NBER Working Paper, 30659, National Bureau of Economic Research.

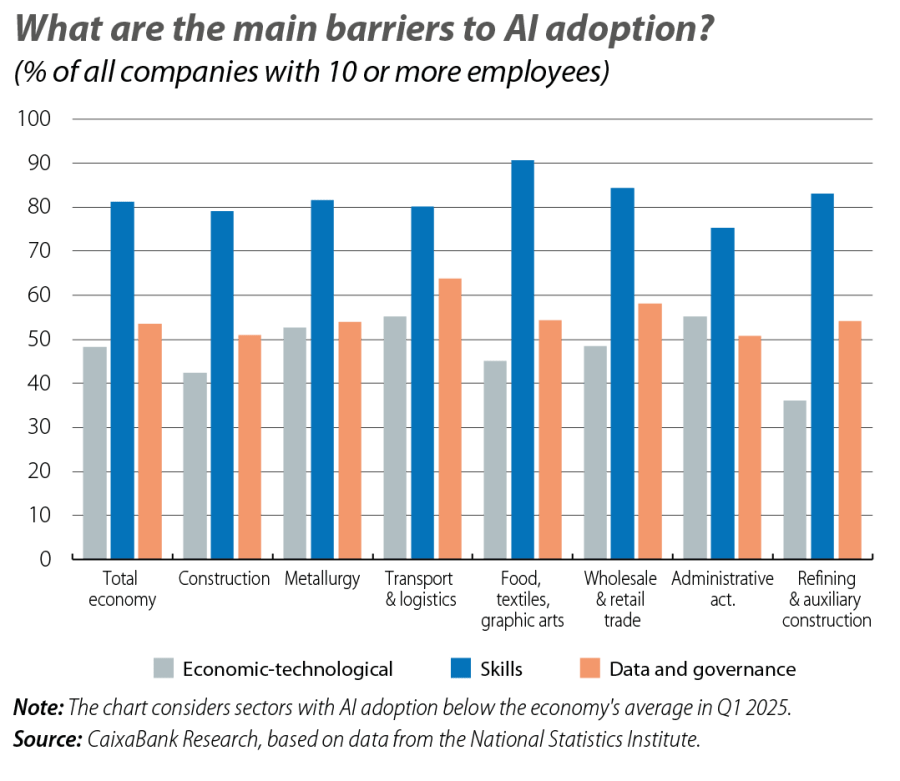

The main barrier to greater adoption is the lack of skills

Among the reasons hindering AI adoption, we can distinguish three groups: (i) economic-technological barriers (primarily high costs), (ii) skills, and (iii) data and governance – the quality and availability of data, privacy, and legal clarity. In sectors with below-average adoption, the main and most commonly cited barrier is a skills issue. Below, we set out the barriers related to data and governance, before covering economic-technological barriers.

International comparison: we are catching up, but remain behind the European leaders

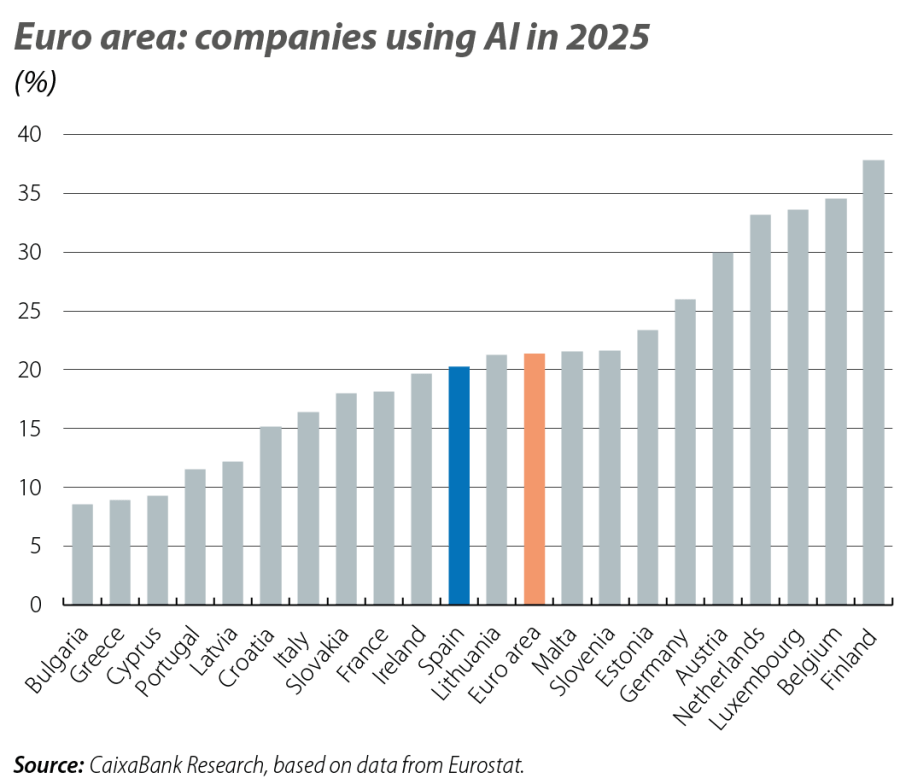

Data from the European Commission reveal that AI adoption rates in 2025 among Spanish firms with over 10 employees are close to the euro area average (albeit still 5 points below). In large firms, the adoption rate is practically identical between Spain and the euro area; the difference is greater (–7 pps) in medium-sized firms.

Compared to the main European economies, the percentage of firms using AI in Spain exceeds that of Portugal, Italy and France, but is below that of Germany and the Netherlands. The recent acceleration in Spain is particularly noteworthy: between 2021 and 2024, adoption increased by just 3 pps (half that of the euro area), whereas between 2024 and 2025 the increase reached 9 pps – outpacing the euro area average and that of Germany, France or Italy.

In summary, there is progress in AI adoption among Spanish firms, but it remains limited and highly uneven. Firstly, company size is crucial: large firms are adopting AI to a much greater extent than SMEs and microenterprises – which are predominant in the country’s productive fabric – potentially widening productivity gaps. Secondly, AI is primarily introduced in cross-functional management and commercial support roles, while its penetration into core production tasks is progressing more slowly, hence its still limited overall impact. Finally, the main barriers are related to a lack of skills, highlighting the importance of strengthening human capital through educational and training policies. The challenge, therefore, is no longer to demonstrate the usefulness of AI, but to facilitate its deep and widespread adoption where the greatest obstacles are currently concentrated.

Digitalisation & Technology

The keys to understanding how digitalisation and new technologies are substantially transforming the economy and how society works.