New economic scenario: improved outlook for the Spanish economy in 2024

Five months after the last update to our macroeconomic forecast scenario, we have incorporated newly available information and re-examined the main factors dominating the outlook for Spain’s economy.

What is the starting point for the scenario?

The Spanish economy has exceeded our expectations in the final part of 2023. Despite the rise in interest rates, average growth in the second half of 2023 remained virtually unchanged compared to the first half (0.5% quarter-on-quarter). This success is attributed, on the one hand, to the significant rebound of private consumption in Q3, driven by the strength of the labour market and the moderation of inflation. On the other hand, GDP growth in Q4 was stronger than expected and reached 0.6% quarter-on-quarter, well above that of the euro area (0.0% quarter-on-quarter). While there are some not-so-positive traits in the growth pattern, such as the high dependence on public consumption and the weakness of investment, such a performance in an economic environment as challenging as the current one should not be overlooked.

The inflation data were also better than expected. In September 2023, our forecast for headline and core inflation (excluding energy and food) at the year end was 4.0% and 3.9%, respectively, but the final figures came in much lower, at 3.1% and 3.2%, respectively. This deviation is explained by the moderation in the oil price beginning in November and a steeper-than-expected fall in the inflation of industrial goods.

Thus, 2024 kicked off with stronger economic activity and a more advanced disinflation process than expected.

Changes in the underlying assumptions of the scenario

Just as in Spain, inflation data for the euro area was also better than expected in the second half of 2023. Whereas in July 2023 euro area headline and core inflation stood at 5.3% and 5.5%, respectively, by December they had fallen to 2.9% and 3.4%, respectively, having both declined by more than 2 pps in the space of under six months. This trajectory has led to a shift in market expectations regarding interest rates. Whereas at the end of September 2023 the markets were anticipating two 25-bp declines in 2024, by mid-February 2024 they were anticipating 4 or 5 such rate cuts.

Our new forecast scenario foresees a steady but gradual decline in euro area inflation over the course of 2024, with values still above, but close to, 2% by the end of the year. This leads us to bring forward the date when we expect to see the first rate cut, from September 2024 to June 2024. Under this new scenario, we expect the ECB to implement up to four rate cuts in 2024 (placing the depo rate at 3.0% in December 2024) and a further three in 2025. We believe the ECB will prefer to accumulate evidence that the disinflation dynamics are well established before beginning to lower rates.

With regard to the oil price, the combination of expectations of lower growth in demand, largely due to lower growth in China, along with the prospect of more rapid growth in supply from non-OPEC countries, lead us to revise our expectations for the path of crude oil prices slightly downwards in 2024, from an average price of 82 dollars/barrel to 79 dollars/barrel. This is a modest change that has a limited impact on our economy. As for gas, price developments in Europe have also been more favourable than we had anticipated a few months ago and we now expect the price to average around 30 euros/MWh in 2024, in line with the level indicated by the TTF futures market.

Macroeconomic outlook

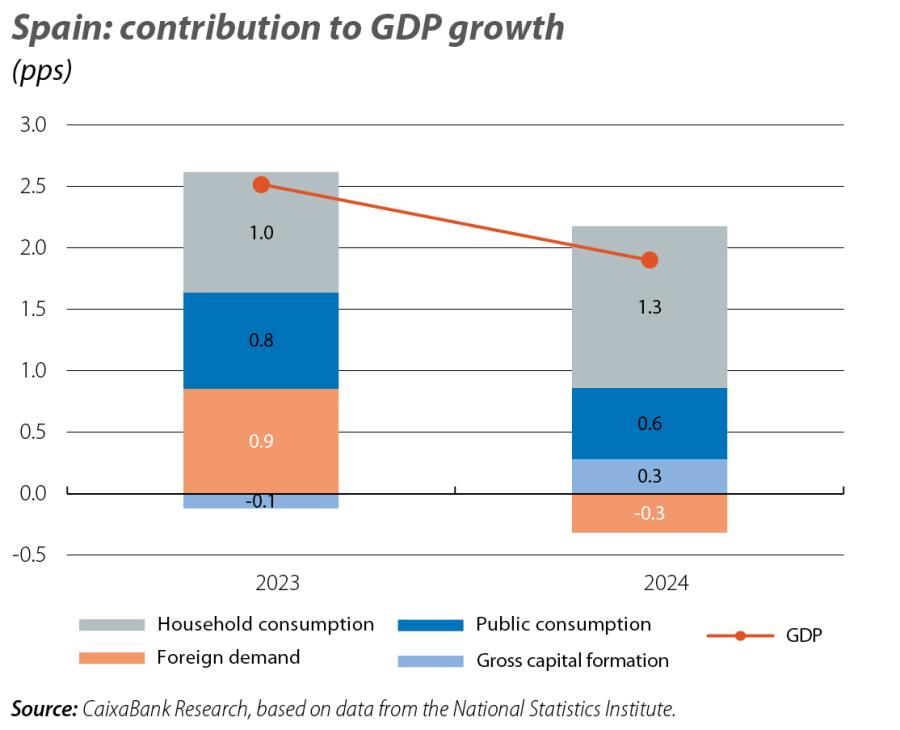

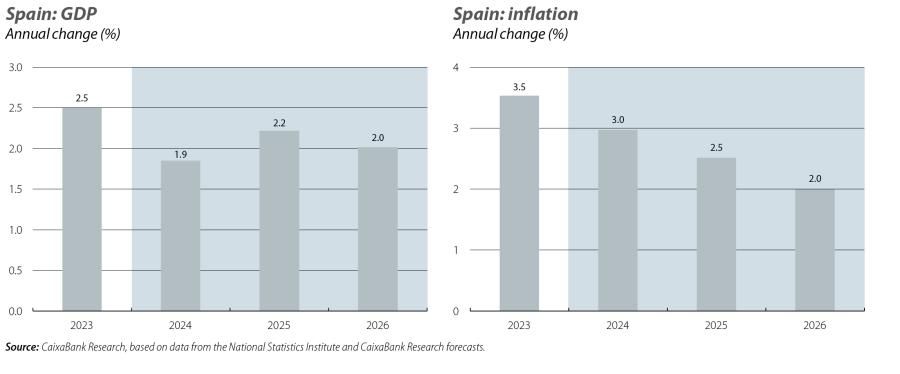

After growing by 2.5% in 2023, we expect the growth of the Spanish economy to moderate in 2024, for several reasons. Firstly, the impact of the rate hikes implemented since 2022 is estimated to have reached its peak in the closing months of 2023 and in early 2024. Secondly, the foreign sector is losing traction due to the weakness of our European trading partners and given that it can no longer benefit from the rapid rebound of the tourism sector, which is now operating above the levels of 2019.1 However, we expect the situation to improve over the course of the year. As the impact of higher interest rates fades, the economy benefits from lower inflation rates, we enter the downward phase of the monetary policy cycle and the impact of the execution of NGEU funds gains more traction, Spain’s economic growth should gather pace. Overall, we expect GDP to grow by 1.9% in 2024 (1.4% per our previous forecast) and to accelerate to 2.2% in 2025 (previously 2.0%).

In 2024, domestic demand is expected to be the driver of growth, spurred on by private consumption. This, in turn, will benefit from the moderation of inflation, higher population growth (closely linked to higher immigration flows) and robust income growth, thanks to job growth (1.9%) and a certain recovery in the purchasing power of wages. Thus, we expect private consumption to grow by 2.4% in 2024, up from 1.7% in 2023. As for foreign demand, as mentioned above we expect it to record more modest growth, associated with the weakness exhibited by our main trading partners.

On the inflation side, we expect the underlying trend to be one of moderation, in line with that observed in the closing stages of 2023. However, the gradual withdrawal of the tax measures previously introduced (VAT reductions on electricity, gas and food) will somewhat mask this underlying trend. Thus, while we expect headline inflation to fall from 3.5% in 2023 to 3.0% in 2024, core inflation will fall more sharply, from 4.4% in 2023 to 2.5% in 2024. This is explained by the fact that the process through which higher input costs translate to the prices of final products and services has been largely exhausted (there may even be some reversal of this process), as well as the limited impact of the so-called second-round effects (the impact on inflation that comes from rising wage costs and margins). The data available from wage agreements, which show a reduction in the average wage rise agreed in labour agreements from 3.5% in December 2023 to 2.8% in January 2024, support this assessment.

Finally, despite the moderation of growth, the labour market is expected to continue to generate employment. This job growth should allow the unemployment rate to continue to come down, although its reduction will be moderate due to the upward revision of the growth of the labour force, greatly influenced by the higher immigration flows observed since last year. Thus, we expect the unemployment rate to moderate from 12.1% in 2023 to 11.8% in 2024 and to 11.4% in 2025.

There are multiple risks surrounding our scenario, although this time we identify both upside and downside risks. On the upside, while we expect private consumption to grow at a significant rate in 2024 (2.4%), the strength of income growth will translate into a very slight moderation of the savings rate, from the 10.6% expected for 2023 to 10.2% in 2024.2 This reduction in the savings rate is small enough to leave room for the possibility of even greater growth in private consumption than our scenario incorporates. Also, our scenario contains relatively conservative assumptions regarding the impact of European funds, which could be greater. On the downside, the biggest risk is the delicate international geopolitical environment. If, for example, the conflict between Israel and Hamas were to escalate, then we could see sharp rises in energy prices and major disruptions to global logistics chains.

In short, in the absence of new surprises, the economy is entering the final stretch of the inflationary cycle which began in 2021 with the disruptions to global logistics chains as the world emerged from the pandemic and the pressures on gas prices in the run-up to the invasion of Ukraine. The gradual convergence of inflation towards the 2% target and the fading of the impact of the interest rate hikes should provide a boost to our economy. However, beyond these temporary tailwinds, it will be necessary to look at the structural challenges facing our economy, fundamentally the low level of investment and the lack of productivity growth.