An optimistic end to the year among investors

Risk appetite is driven by hopes of a recovery in 2021

Investors closed the year giving continuity to the bullish trend that the markets had accentuated in November. Their performance was favoured by the initiation of vaccinations against COVID-19 around the world, the unblocking of the European Recovery Plan (Next Generation EU) and the signing, in the last week of December, of the Brexit trade agreement and a new fiscal stimulus package in the US. Furthermore, at their respective December meetings, the major central banks reiterated their intention to maintain accommodative financial conditions for a long period of time. Together, all of these elements fuelled investors’ optimism and appetite for risky assets more closely linked to the business cycle. Thus, the financial markets closed the year with a December marked by widespread gains in the stock markets, in commodity prices and in most currencies against the dollar. This bullish trend has brought relatively high valuations, which on the one hand are sustained by the continued support from economic policies and the expectation of a stronger economic recovery in 2021. However, on the other hand they also highlight the vulnerability of the global financial scenario if the economic outlook were to take a turn for the worse. Thus, while the start of the vaccination process paves the way for the recovery in the medium term, in the short term economies continue to face a highly demanding health scenario. In this context, investor sentiment will remain sensitive to how the pandemic develops, to economic policies and, more in the medium term, to the emergence of the scars that the COVID-19 crisis could leave on the productive fabric of the economy (such as the risks of increased defaults, business failures or job destruction).

The stock markets register new gains

In a year marked by historic stock-market crashes (in March, the US stock market suffered the third worst session of the last 100 years), the major equity markets ended December with widespread gains. Moreover, indices such as the MSCI global (All Country World) index, which includes both developed and emerging economies, and the S&P 500 managed to claw back the losses of the spring and even reach new all-time highs in December. The European stock markets, meanwhile, also performed very well in the final leg of the year, driven by the recovery of the sectors most closely linked to the business cycle (such as energy and the financial sector). Similarly, the emerging market indices showed an encouraging performance (MSCI Emerging Markets +15.7% in Q4) driven particularly by the recovery of Asian economies.

Brent oil breaks through the 50-dollar barrier

Expectations of greater economic activity and mobility of goods and individuals in 2021 boosted commodity prices across the board, with monthly increases of around 10% in agricultural and precious metal indices, as well as in oil prices themselves. Specifically, the price of a barrel of Brent oil continued the climb initiated in November and approached to 52 dollars, marking a historic rally of 160% from the low registered in April. In fact, the oil price was also supported by the decisions of OPEC and its allies, which in December agreed to increase production by a much lower amount than previously suggested (+500,000 barrels a day from January, and with monthly revisions, compared to initial indications of +2 million barrels a day).

The ECB extends the measures to combat the COVID-19 crisis beyond 2021

In line with expectations, in December the ECB relaunched various measures to continue to offer highly favourable financial conditions and to stimulate the euro area’s economic recovery. These included the extension of net purchases under the PEPP until at least March 2022 and an increase in the programme’s budget of 500 billion, bringing the total to 1.85 trillion. Therefore, having spent just over 750 billion in 2020, the PEPP is embarking on 2021 with a spending capacity of almost 1.1 billion still remaining, in addition to the net purchases under the APP (which amount to 20 billion per month). The ECB also agreed on three new TLTRO-III liquidity injections in 2021, with favourable conditions which will be extended until June 2022 (full details can be found in the ECB Observatory of 10 December). In this context, in the fixed-income markets, sovereign yields and risk premiums in the euro area remained low in countries of both the core and the periphery.

The Fed anchors asset purchases in 2021

Like the ECB, the Fed reiterated its commitment to maintaining dovish accommodative financial conditions for a long period of time. However, in the US, the strong market performance (with the stock markets at a peak and volatility close to pre-pandemic lows) and the improved resilience of the economic activity indicators, coupled with the strong monetary measures already in place, led the Fed not to add any additional stimuli. Thus, in December the Fed held the reference rate at 0.00-0.25%, maintained asset purchases at 120 billion per month (80 billion in treasuries and 40 billion in MBSs) and limited itself to clarifying that purchases will continue at least at the current rate until «substantial further progress has been made toward the Committee’s maximum employment and price stability goals». According to its own macroeconomic forecast table, this would indicate their continuity until at least the end of 2021.

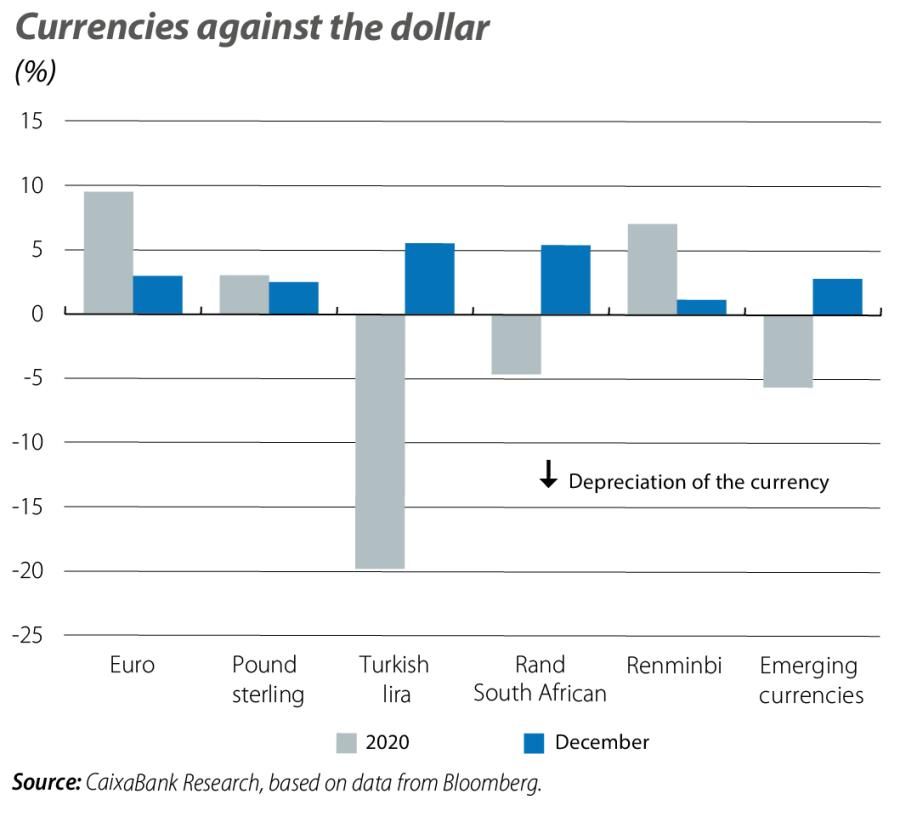

Emerging currencies regain ground against the dollar

The improvement in investor sentiment in December encouraged the shifting of capital flows away from safe-haven assets, such as the dollar and the yen, towards other assets with more attractive yields, such as emerging-country currencies. This set of currencies experienced an accelerated appreciation against the dollar during the month (+2.8%), with the Chilean peso and the Turkish lira leading the rally thanks to the improvement of their domestic monetary scenarios and the recovery of demand for commodities. In advanced economies, the euro extended its strength to reach 1.23 dollars, its highest level in two and a half years, while the pound sterling also registered a notable appreciation (+2.6% against the dollar) thanks to the signing of the trade agreement between the EU and the United Kingdom.