The macroeconomic fragility of interest rates

Despite the unprecedented economic downturn caused by COVID-19, the cost of financing public debt is at an all-time low. To what extent do these interest rates lie behind the macroeconomic fundamentals?

- The unprecedented blow that the COVID-19 crisis has dealt to the economy lies in stark contrast with the current low interest rates and risk premiums. Nevertheless, the macroeconomic fundamentals remain good indicators of the interest rates observed in the market.

- We estimate that the deterioration in these fundamentals would have applied substantial upward pressure to rates across the euro area. This pressure, which has not materialized in the market, serves as a measure of the success of economic policy, but also as a reminder of how important it is for economic policy to remain active over the coming quarters.

In 2020, European economies will endure a fall in GDP far worse than any other in their modern history. Moreover, it will be accompanied by a very sharp rise in government debt, which will raise public debt ratios to new all-time highs.1 However, despite this unprecedented deterioration in the economy caused by the COVID-19 pandemic, the financing cost of public debt is almost at an all-time low: in September, Germany and France’s 10-year sovereign interest rates were even negative (–0.5% and –0.2%), while Spain and Portugal’s rates were slightly below 0.3%. To what extent can the macroeconomic fundamentals explain these interest rate levels?

- 1The forecasts of the consensus of analysts suggest an increase in the public debt ratio in 2020 of more than 15 pps for the euro area as a whole. According to historical data collected by the IMF, which dates back to the mid-19th century, this will lead to new highs in the debt of countries such as Germany, Italy and Portugal. This is not the case for Spain and France because, more than 100 years ago, they had achieved ratios of 160% and 240%, respectively.

Interest rates and macroeconomic fundamentals

Public debt yields depend on the macroeconomic fundamentals of the country in question and on the global environment. For instance, a state’s payment capacity depends on its level of indebtedness, as well as on expectations about its public surplus or deficit and the future growth of the economy. Furthermore, the situation of the European economy as a whole determines the monetary policy that is set by the ECB, which it uses to influence the many different types of interest rates. Global factors also play an important role (for example, interest rates in other economies, which offer an alternative investment opportunity), as does investors’ risk appetite. With all these ingredients, and based on the historical relationships between them, we can estimate the sovereign interest rate that is consistent with the macroeconomic fundamentals: the so-called «macro rate».2

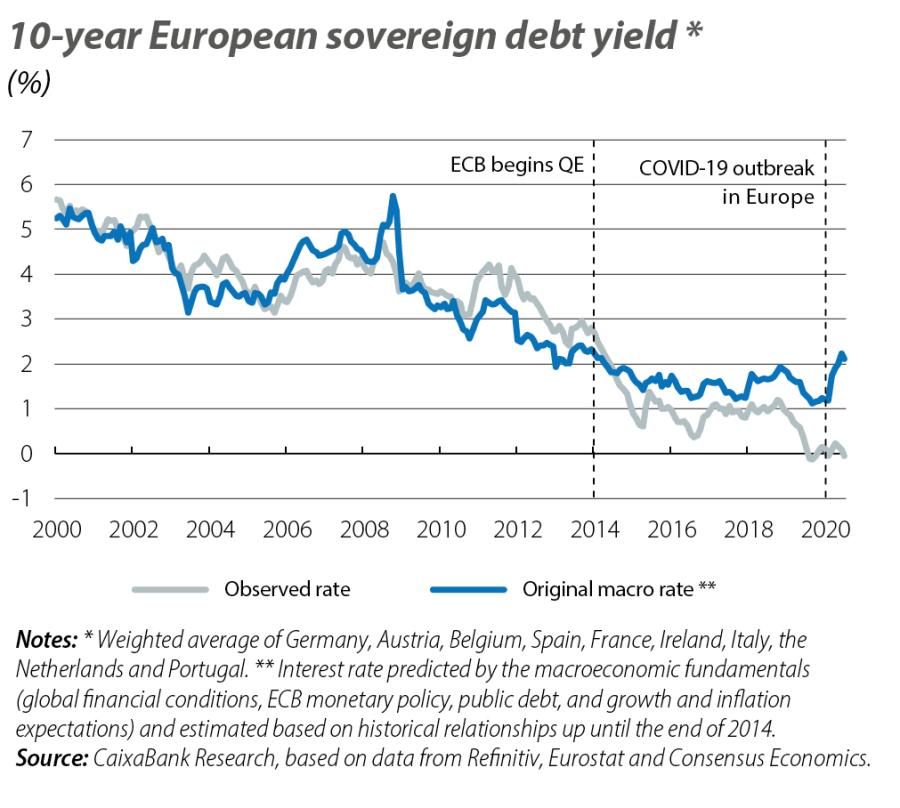

The first chart illustrates that macro fundamentals often serve as good indicators of market interest rates. However, in recent years there are two important periods of divergence: in 2020, with the COVID-19 outbreak, and in 2015, with the start of the ECB’s unconventional monetary policy that resulted in interest rates remaining persistently below the macro rate. However, this divergence from 2015 onwards is somewhat expected, since our macro rate does not include the asset-purchasing programmes initiated by the ECB five years ago as part of the macroeconomic fundamentals. However, after years of unconventional monetary policy and with the prospect of these tools remaining very much active over the coming years, it is useful to incorporate the ECB’s unconventional measures into our macro rate estimate.3

- 2We estimate a panel regression for the 10-year sovereign rates of Germany, Austria, Belgium, Spain, France, Ireland, Italy, the Netherlands and Portugal with the following explanatory variables: expectations on the 3-month Euribor, real GDP growth and inflation, the ratio of public debt to GDP, an indicator of stock market volatility, the 10-year US sovereign rate and an indicator of euro area stress (a binary variable that equals 1 if a sovereign risk premium becomes significantly stressed). Initially, to avoid considering the ECB’s unconventional monetary policy as one of the fundamental factors, we estimate the regression with data for the period between 2000 and 2014.

- 3We re-estimate the regression of the previous note, including data up until the beginning of 2020 and adding the asset purchases that the ECB has amassed on its balance sheet since 2015 as another of the explanatory variables.

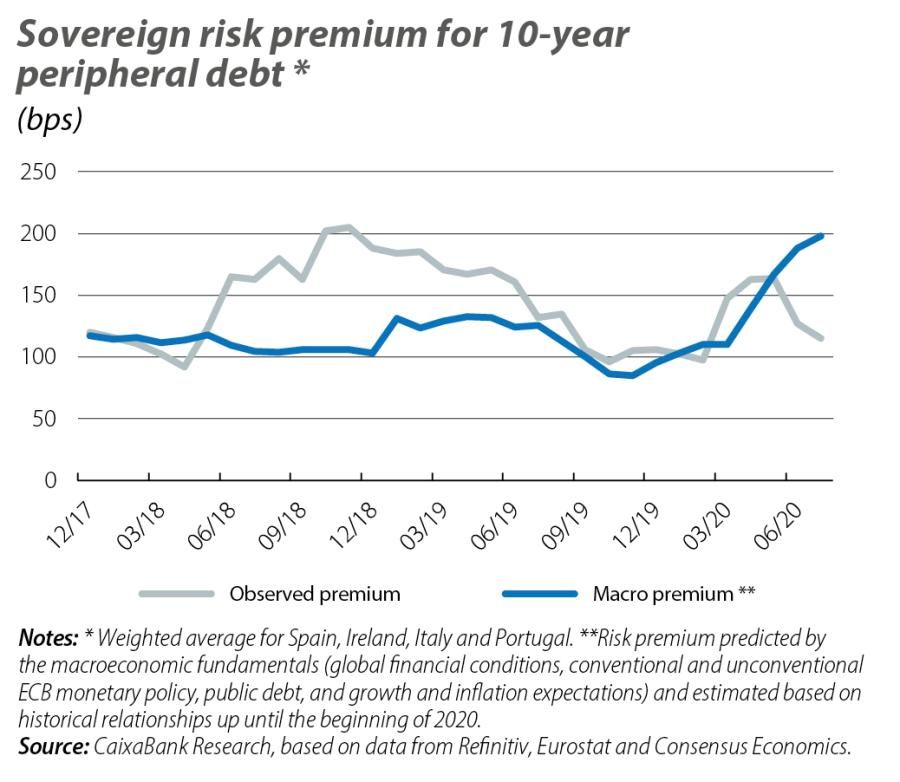

As the second chart shows, including unconventional monetary policy as one of the macroeconomic fundamentals helps us to better explain the decline in market interest rates in recent years. However, with the COVID-19 outbreak we continue to see a marked decoupling between the observed rates and macro rates. Specifically, the macro rate for the euro area as a whole suggests that the deterioration in the macroeconomic fundamentals should have led to an increase in the euro area’s sovereign interest rate of around 100 bps greater than that observed.4,5

- 4An ECB estimate concludes that the monetary measures taken between March and June would have reduced the euro area’s sovereign rate by 45 bps. See J. Hutchinson and S. Mee «The impact of the ECB’s monetary policy measures taken in response to the COVID-19 crisis», Economic Bulletin 5/2020, ECB.

- 5In the second chart, the rebound in the macro rate which incorporates the ECB’s unconventional policy is somewhat higher than that of the original macro rate. The reason for this is that the sensitivity of interest rates to changes in growth and inflation expectations has increased since 2015. This could reflect the fact that they serve as an indirect measure of expectations as to whether the ECB will withdraw or intensify its asset purchases, which have had such a significant impact on market interest rates.

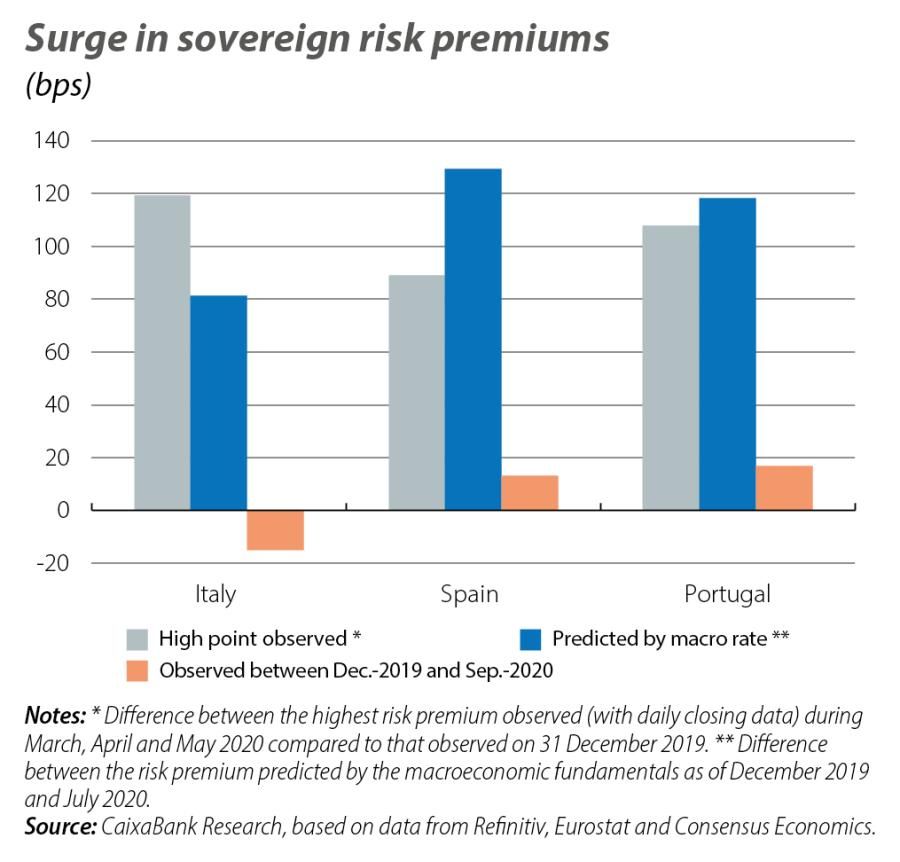

In fact, this decoupling can be interpreted as a measure of the success of the economic policy response and, in particular, of the ECB’s decisive action and the EU’s shared fiscal effort.6 A good demonstration of this can be found in how risk premiums in the euro area periphery have behaved. The third and fourth charts show how the initial surge in periphery risk premiums in the market was reasonably consistent with that projected by the macro rate and, therefore, by the deterioration in the macroeconomic fundamentals. However, there was a widespread retreat in stress levels following the ECB’s battery of announcements throughout the spring and the EU’s various fiscal packages.

- 6For a summary of both actions, see the notes «El Consejo Europeo llega a un acuerdo histórico sobre el Plan de Recuperación Europeo» and «Gracias a una actuación contundente, el BCE respira y se da un tiempo» at www.caixabankresearch.com.

Among the EU’s various shared fiscal measures, one of the most positive developments for risk premiums has been the agreement to issue European debt backed by the EU budget. Although the issuance of European debt will not begin until 2021, this agreement sends an important signal of commitment to the European integration project, which reduces the perception of sovereign risk and helps to keep sovereign risk premiums down. Nevertheless, it should also be borne in mind that the issuance of European debt will increase the supply of high-quality bonds which, in the medium term (2023-2024 according to some estimates)7 could lead to an increase in financing costs for states with a lower credit rating due to the increased competition when vying for purchasers of debt.

Finally, the current environment is so demanding that, despite the decisive steps taken by economic policy to date, policymakers cannot afford to lower their guard. The discrepancy between the observed market interest rate and the macro rate is not only a measure of their success: it also tells us that, without ambitious action, we would be observing substantially higher interest rates and risk premiums in the market, in some cases even approaching levels that could fuel doubts about the sustainability of public debt.8

Macrofinance

What factors will determine the evolution of interest rates, investment sentiment and macro-financial conditions in general?