Lack of new housing where it is most needed: a growing and geographically concentrated deficit

According to estimates by CaixaBank Research, Spain has accumulated a housing deficit, now exceeding 730,000 units, as a result of rapid household formation and an insufficient response from new construction. In this article, we review the extent of this mismatch and its impact on recent patterns in house prices, which are showing increasing tension across much of the country. We also observe that the construction of new homes is not accelerating, precisely in the regions where the gap between supply and demand is most pronounced, exacerbating the imbalances and prolonging the pressure on prices. Finally, we examine the factors limiting the recovery of supply (from rising construction costs to regulatory restrictions and the lack of land designated for development, in addition to infrastructure issues) and we anticipate little improvement in the short term in the sector’s capacity to meet current housing needs.

The housing deficit in Spain exceeds 730,000 units and continues to grow

Since 2021, 1.2 million households have been created in Spain, while only 474,000 homes (including both unsubsidised and social housing [VPO]) have been completed.1 This represents a deficit2 of at least 734,000 homes, which extends across all of Spain’s provinces, with the only exceptions being Guipúzcoa, Cáceres and Soria.

- 1

At the close of this report, the data for completed homes in Q4 2025 has not yet been published, so we will assume that the completed homes in Q4 2025 experienced a similar variation to that of the cumulative figure for the year to Q3 (–4.5% for the national total).

- 2

This is a minimum estimate of the deficit, as it does not take into account that some of the completed homes will have been directed to meet the demand for second homes, tourist accommodation or will have been purchased by non-resident foreign buyers. For a specific analysis of other ways to measure the housing deficit, see the article «The price of not building: how the housing deficit explains much of the price pressures» in the Real Estate Sector Report S2 2025.

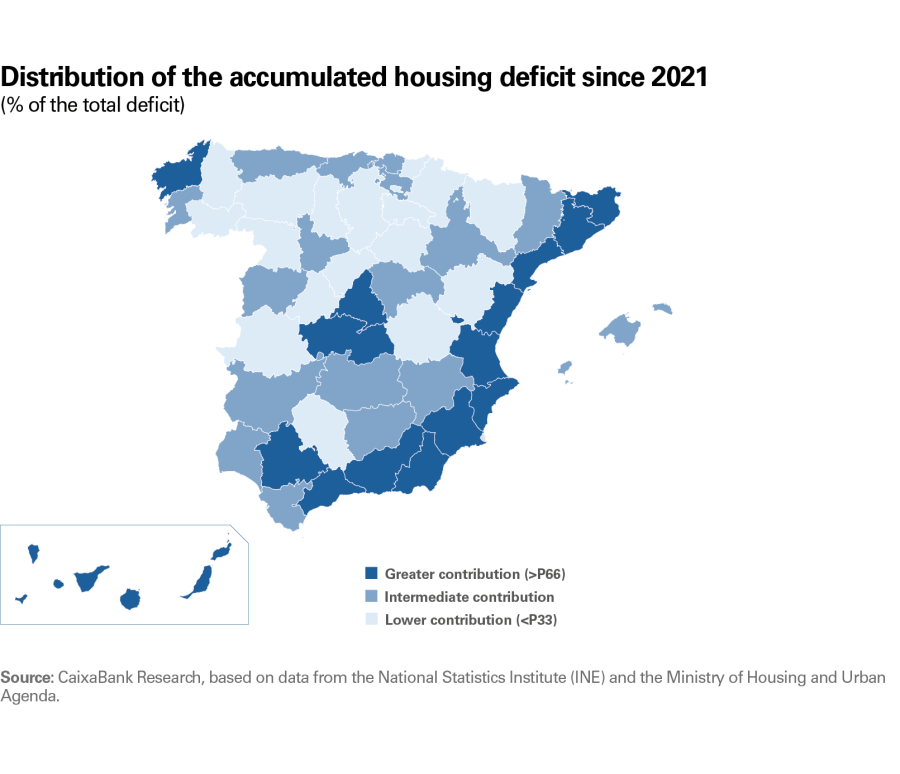

The first map shows the distribution by province of the housing deficit accumulated since 2021, expressed as a percentage of the total national deficit (the colours indicate the distribution of the deficit in percentiles).3 Almost half of the national deficit (49%) is concentrated in just five provinces: in order from greatest to smallest, Madrid, Barcelona, Valencia, Alicante and Murcia. In principle, it is not surprising that most of the deficit is concentrated in the large residential markets.

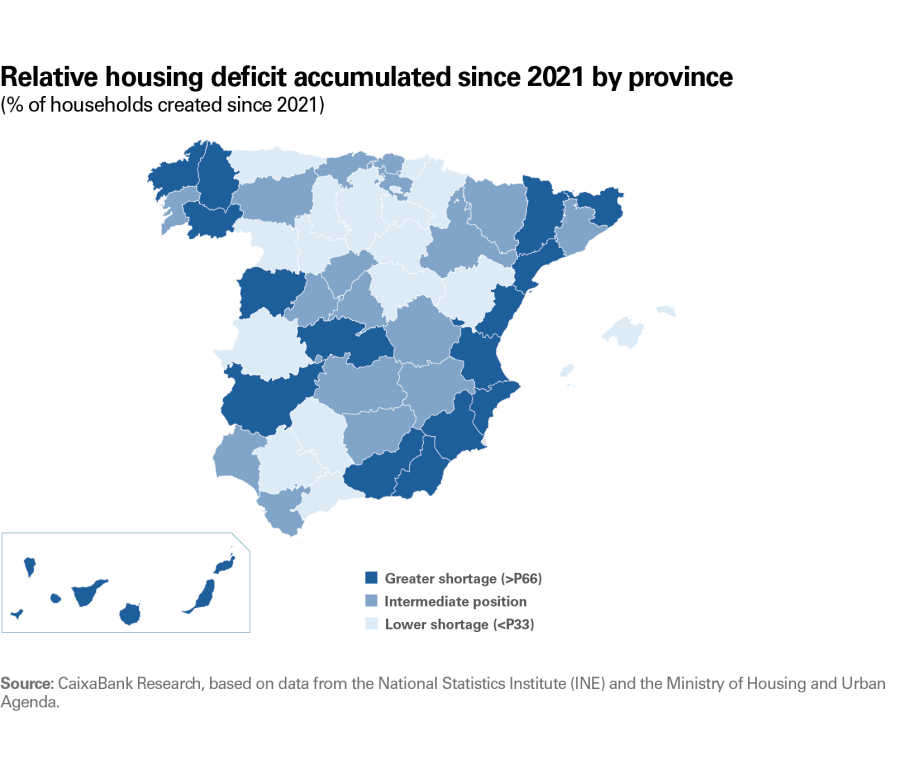

The second map shows the accumulated deficit in each province as a percentage of households created since 2020 and indicates which provinces have a greater or lesser housing shortage relative to household creation. Broadly speaking, the provinces of the Mediterranean arc continue to stand out, as do some provinces in the south and southeast of the peninsula, as well as the island regions. It is noteworthy that provinces with large cities (Madrid, Barcelona, Zaragoza and Seville) have disappeared from the category of greatest housing shortage (darkest blue). Special mention should be made of the provinces of Galicia and the specific cases of Badajoz, Salamanca and Toledo, which have a high relative shortage of housing, not so much due to strong household formation, but rather due to the limited addition of new homes to the housing stock.

- 3

The accumulated housing deficit at the national and even the provincial level does not fully reflect the existing tensions, as part of the shortage recorded in certain areas and municipalities cannot be offset by the surplus in other regions.

Housing is not always built where it is needed

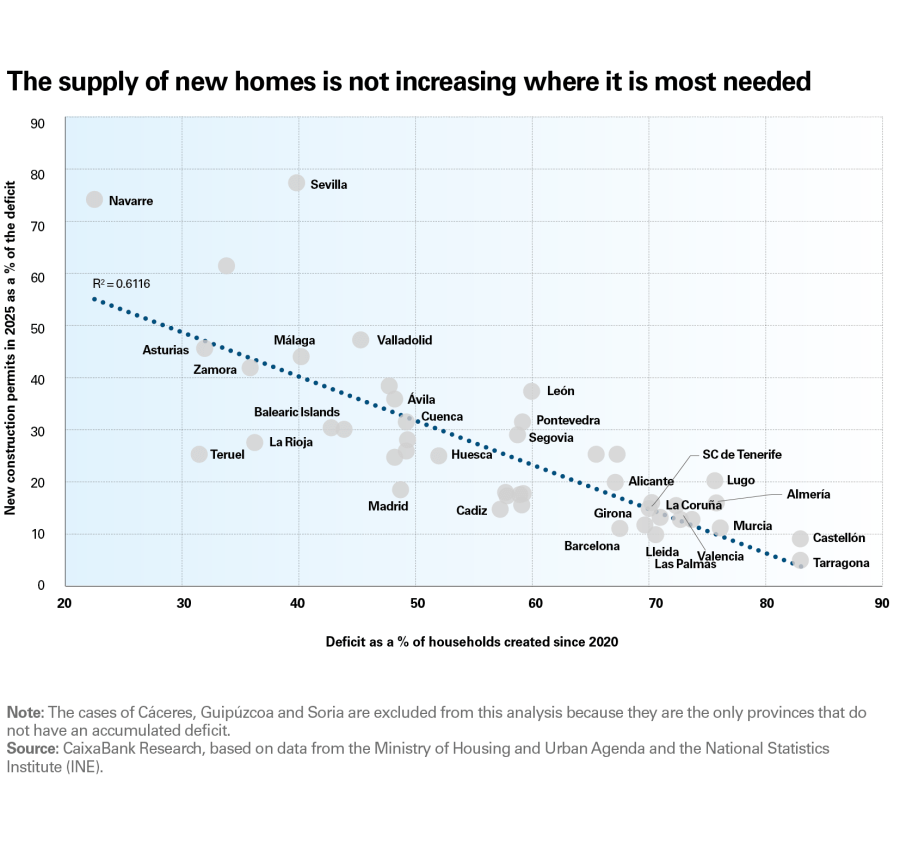

New construction permits in Spain increased by 11.8% in 2025 (unsubsidised and social housing), below the rate of 2024 (24.6%), although around 34% of Spanish provinces recorded declines.

In the following chart, for each province we compare the housing deficit (as a percentage of the total households created since 2020 in each province) with the new construction permits granted in 2025 (as a percentage of the accumulated housing deficit in the province). The chart reveals that the increase in the supply of new homes does not always occur where the deficit is greatest. Although the dispersion is high, a clearly negative correlation can be observed between the accumulated housing deficit and the growth of permits, revealing significant territorial imbalances. In provinces with relatively higher deficits (Tarragona, Castellón, Murcia, and Almería, among others), the new permits do not even cover 10% of the deficit, whereas others with lesser needs, such as Seville, Navarre, Córdoba, and Asturias, show an intense rate of new construction. This pattern indicates the existence of local constraints – such as land, regulation, costs, or administrative capacity – that limit the response from supply precisely in the most strained markets and contribute to the persistence of structural imbalance. As long as this imbalance persists, the deficit will continue to accumulate in the most strained provinces, maintaining upward pressure on prices and hindering affordability.

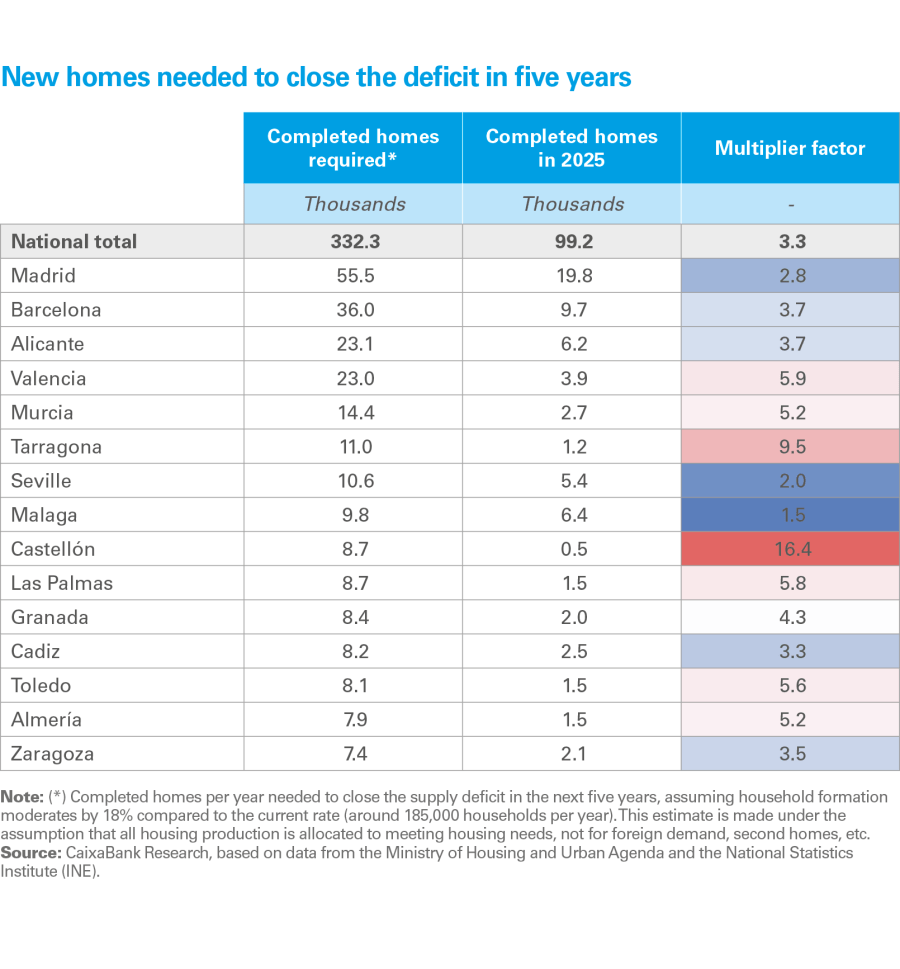

The magnitude of the gap between completed homes and household creation is such that it would be necessary to produce around 330,000 homes annually over the next five years in order to absorb the existing deficit, representing a quadrupling of the current rate of completion.4 However, this need for acceleration varies widely across the country and is particularly intense in those provinces where, since 2020, household creation has far exceeded housing construction. In particular, the adjustment required in the provinces with the greatest accumulated deficit is summarised in the following table.

- 4

This estimate assumes a reduction in household formation of around 18%, to approximately 185,000 households annually, in line with our trend-based scenario, under the assumption of a moderation in household formation in the coming years due largely to housing affordability issues.

The factors that are limiting new supply are unlikely to be resolved in the short term

The supply of new housing remains constrained by multiple structural factors that are limiting the sector’s ability to respond to the sustained increase in demand. These include the shortage of land designated for development in areas with the highest residential pressure, the administrative delays in urban planning processes – which in some cases can extend for more than a decade –, the additional costs arising from more stringent regulations, the increase in production costs, and the shortage of skilled labour, all within the current context of historically low returns for the property development sector.

The traditional obstacles to new development persist and others of a more temporary nature are emerging

More recently, the capacity of the electricity grid to support new developments has been identified as an additional bottleneck for housing production. In February 2026, Spain’s national grid (Red Eléctrica, REE) published the first access capacity map for demand on the transmission grid, showing that around 75% of the network nodes are saturated or have no available capacity, precisely in the areas where residential activity is the most concentrated. Given that grid access is a prerequisite for the granting of permits, this saturation directly affects developments, causing delays in the execution of new projects.

The recognition of this issue by the government and the main agents in the electricity system has prompted MITECO (the Ministry for the Ecological Transition and the Demographic Challenge) to begin working on a royal decree aimed at increasing access capacity to the electricity networks. This regulation proposes, for example, updating the technical connection requirements in order to unlock currently blocked capacity – without the need for any major reinforcements of the network.

The housing deficit will continue to increase in the coming years

To assess how the housing deficit in Spain could evolve over the next 15 years, we consider three alternative scenarios. In cumulative terms, all of them account for a total production of around four million homes, although they differ significantly in construction rates and household formation dynamics.

The scenario we might call trend-based (grey line in the chart on the next page) projects that the housing deficit will reach its peak in 2029, with around 922,000 homes, and would not be fully corrected until 2037. This scenario is based on two main assumptions. The first assumption is that supply will gradually increase, with annual growth rates of 14%-16%, allowing the development sector to reach 200,000 completed homes by 2031, after which it would continue to grow, but at a more moderate pace, approaching 400,000 homes by 2037. The second assumption is a slight moderation in household formation, to around 180,000 net units annually from 2028.

The second scenario considers a more intense rebound in supply in the coming years, assuming that the development sector manages to resolve the current bottlenecks and increases production at rates in excess of 20% annually between 2028 and 2031, which would mean nearly 300,000 homes being completed in 2031. In this case, the deficit would reach its peak in 2028 (around 900,000 homes) and would disappear by 2034.

Finally, in the third scenario, a more pronounced moderation in household formation is assumed, precisely as a consequence of housing affordability issues and scarce supply. A gradual decline in net household creation is assumed until it stabilises at around 150,000 units annually from 2031. With a supply trajectory similar to the trend-based scenario, the deficit would reach its peak in 2029 (around 931,000 homes) and would correct more quickly, disappearing by 2036.