The Spanish economy in 2026

CaixaBank Research’s forecast scenario for the Spanish economy, which was finalised before the outbreak of the war in Iran, anticipates dynamic growth in 2026, albeit more moderate than that of recent years. Domestic demand, and especially private consumption and investment, began the year with sufficient momentum to enjoy strong growth and continue leading the recovery. However, the outbreak of the conflict in the Middle East opens a new chapter of global economic and political uncertainty.

The economic consequences of this conflict will depend on its regional scope and duration, as well as the damage sustained by the region’s energy infrastructure. In this regard, it is still too early to assess the impact it could have on the Spanish economy. At the close of this report, energy prices have risen significantly, but the markets are anticipating that this could be a temporary spike; the increase in inflation expectations has also been moderate, and sovereign risk premiums remain relatively low. These are some of the channels through which the Spanish economy could be affected, so they should be closely monitored over the coming months.

The economy ended 2025 on a strong note

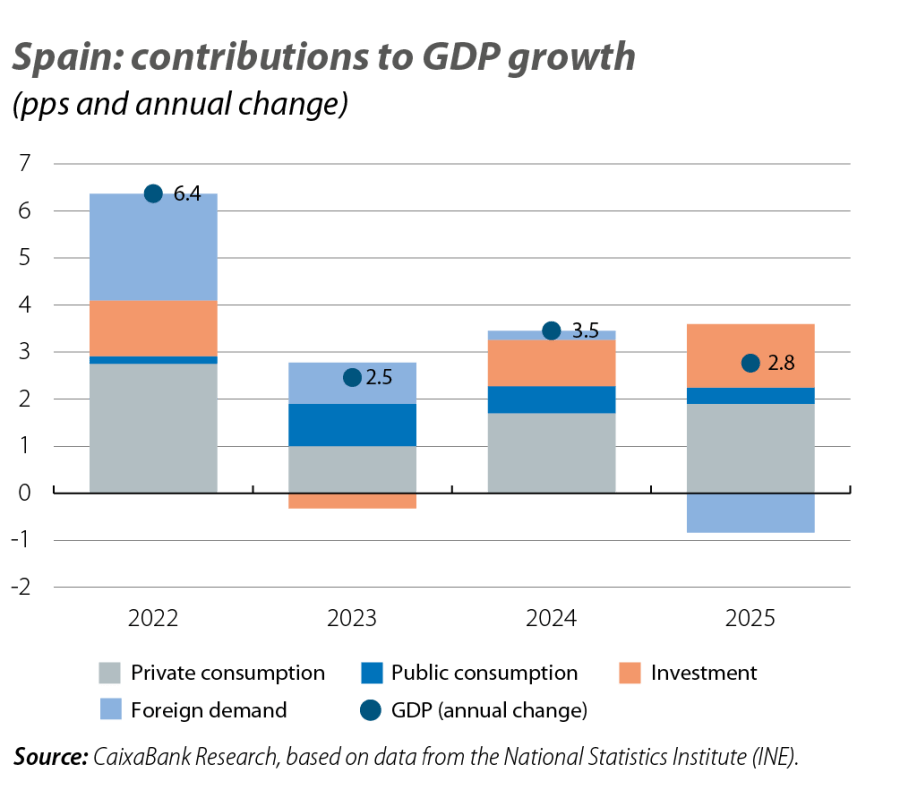

2025 was a good year for the Spanish economy. Despite the tariff challenges, GDP advanced by an impressive 2.8%, almost double the 1.5% recorded by the euro area as a whole. The composition of growth confirmed the shift in growth drivers. Domestic demand, particularly private consumption and investment, drove the expansion, while net foreign demand reduced growth for the first time in years (see chart). This negative contribution does not mean a loss of competitiveness – as we explain in the Focus «Spanish exports amid challenges to their competitiveness» in this same Monthly Report – but rather reflects the weak growth of our main trading partner, the protectionist shift in the US and the sharp increase in imports linked to investment and, to a lesser extent, consumption.

Growth in Q4 2025 was better than expected: GDP increased by 0.8% quarter-on-quarter, exceeding the initial forecast of 0.5%. Similarly to the entire year, the impetus came from private consumption and investment, while the foreign sector detracted from growth despite the rise in exports. This positive surprise places the Spanish economy in a better starting position to face 2026, and mechanically adds 0.2 pps to the annual growth forecast due to the so-called carry-over effect.

Following the strong end to 2025, the available indicators for economic activity, employment and consumption in 2026 to date present a more mixed picture. The initial Social Security affiliation data and the PMIs show a slight moderation compared to the previous quarter, partly due to disruptions caused by the bad weather. The CaixaBank Research consumption indicator also shows a temporary loss of momentum due to the bad weather: in January, it grew by 4.0% year-on-year, a very similar figure to that of 2025; in the first two weeks of February, the growth rate fell below 1%, but the latest data already suggest a certain recovery. The forecast scenario anticipates growth of 0.5% in Q1 2026, but in light of all this, the risks have shifted to the downside.

Underlying assumptions of the scenario

The Spanish economy has benefited from several dynamics that could persist and continue to drive economic activity. The population grew by 1.0% in 2025, well above the average rate of 0.4% recorded between 2014 and 2019, mainly due to immigration flows. Although these flows may moderate, they are likely to continue supporting demographic growth in the coming years.

The labour market has managed to absorb the population increase, and the employment rate – employed persons as a proportion of the population aged over 16 – continued to grow, rising from 52.1% in 2024 to 52.8% in 2025. Our scenario assumes that this trend will continue in the coming quarters, as we do not observe any clear signs of stress. Proof of this is that the CaixaBank Research wage indicator shows that private sector wages grew by 2.7% on average in 2025, below the 3.3% recorded in 2024, suggesting an absence of widespread wage pressures.

Additionally, in 2025, a strong investment cycle began, particularly in capital goods. This type of cycle tends to show high persistence, so as long as the macro-financial conditions remain accommodative and there is not a persistent increase in uncertainty, investment could remain relatively dynamic over the coming years.

At the international level, the main uncertainty is the price of energy. Before the outbreak of the conflict, we were anticipating a steady moderation. In the early stages of the conflict, Brent oil and natural gas prices have surged. Nevertheless, they are still lower than those recorded in 2022. If this price spike is short-lived, then its impact on growth and inflation would be limited to just a few fractions of a percentage point. Under this assumption, the inflationary disturbance would be temporary and the ECB could keep interest rates at their current levels. However, the uncertainty is particularly high in this area.

Regarding foreign markets, the forecast scenario is based on the assumption of moderate growth in the main export destinations, of around 2% in 2026 (2.8%

in 2025, 4.3% between 2017 and 2019), but it could be lower depending on how the conflict in the Middle East develops.1 Therefore, Spanish exports are likely to continue to grow at a moderate pace.

- 1

For further information about the calculation for the export markets, see the article «How will the Spanish economy be affected by the performance of its main export markets?», in the MR11/2025.

Forecast scenario

The forecast scenario assumes that in 2026 the Spanish economy will retain much of the dynamics that characterised 2025, although they could be more or less affected depending on how the conflict in Iran pans out. In principle, domestic demand – sustained by consumption and investment – could continue to be the main driver of growth. In contrast, exports are expected to play a more subdued role due to the weakness of global trade. At the same time, the anticipated increase in imports to meet domestic demand would mean that foreign demand will detract from growth. Following the 2.8% recorded in 2025, the scenario anticipates GDP growth of 2.4% in 2026 and of 2.0% in 2027.

Private consumption could be supported by interest rate cuts, demographic growth driven by immigration, the strength of the labour market and the gradual reduction of the savings rate. Investment, for its part, could also benefit from lower interest rates and the continued support of NGEU funds. 2026 is a crucial year for these funds, as it marks the programme’s final year. Our forecast scenario assumes that they will be executed in their entirety before the deadline, which would involve a slight acceleration in the pace of execution. While around 15 billion was executed annually between 2023 and 2025 on average, it is assumed that around 16 billion will be executed in 2026. By component, we anticipate a greater boost in residential investment, while investment in equipment is expected to grow at a more moderate pace.

On the other hand, the scenario envisages a moderation of inflation to around 2.4%, compared to 2.7% in 2025. However, the surge in energy prices triggered by the conflict in the Middle East introduces upside risks in this regard. Beyond the doubts about the future evolution of the energy component, services prices continue to show resistance to moderation and there has been a certain resurgence of food price pressures.

There is also significant uncertainty surrounding forecasts for the labour market. It ended 2025 on a very strong note, even accelerating the growth rate in the final part of the year. In this context, employment growth began 2026 with a relatively favourable outlook, as reflected in our forecast scenario, which anticipates a 2.3% increase in employment this year and a reduction in the unemployment rate to as low as 9.8%. However, in this sphere, the impact of the war in the Middle East could also be felt if it affects energy prices, global trade or financial conditions.

In short, the Spanish economy began the year with sufficient support to continue growing at a strong pace, but the outbreak of the war in Iran once again makes any forecasting exercise very difficult. Its impact will depend on the duration, intensity and geographical scope of the conflict. In order to gauge this, over the coming months it will be necessary to closely monitor the expected magnitude and persistence of the energy price rally and the potential impacts on global trade flows, as well as the resilience of financial conditions.