A red year-end in the financial markets

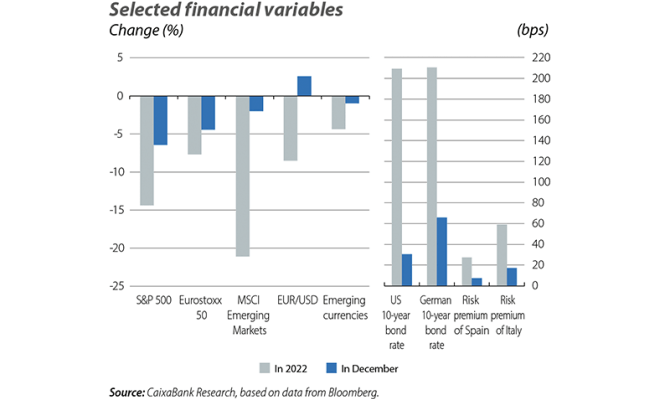

The closing weeks of 2022 were marked by reduced risk appetite and declines in the main financial assets, reducing the gains that had been registered for much of the autumn. The main factor was that central banks hardened their hawkish rhetoric, as they reiterated their intention to continue raising official rates in the coming months and lowered expectations of a possible end to the monetary tightening process. Meanwhile, the expectations of higher rates, along with the signs of cooling in most of the economic data, revived fears among investors about a possible global recession, or hard landing, which in turn exacerbated the losses in international stock markets, government bonds and other fixed-income assets. On the upside, the commodity markets ended the year with some stabilisation in the price of the main benchmarks, albeit still subject to the volatility and uncertainty associated with the prolongation of the war in Ukraine.

Among the major central banks, the ECB stood out with a significant tightening of its hawkish narrative during its last meeting in mid-December. Despite moderating the pace of its official rate hikes from 75 bps to 50 bps (with the depo rate at 2.00% and the refi rate at 2.50%), the institution surprised the markets by stating that additional hikes will be necessary. Moreover, these hikes are expected to be significant and will be introduced at a sustained rate, consistent with a terminal depo rate above 3.0%, according

to ECB president Christine Lagarde. In addition, the ECB announced guidelines for the reduction of its bond portfolio under the asset purchase programme (APP) beginning in March (at an initial rate of 15 billion per month). Together with the maturities and early payments of the TLTRO loans, this will result in a significant reduction in the size of the balance sheet (see the Focus «The reduction of the ECB’s balance sheet in 2023» in this same report). These announcements were reflected in an upward revision of expectations for implicit rates in the money markets and in a rise in sovereign bond yields, which was most pronounced in peripheral debt. On the other hand, other European central banks, such as the Bank of England, Sweden’s Riksbank and Norway’s Norges Bank, also announced more moderate rate hikes in December, albeit indicating that further adjustments would follow in the coming months.

In a similar vein, the Federal Reserve also raised official interest rates by 50 bps, placing them in the 4.25%-4.50% range, and announced that further increases would follow during 2023. Specifically, and according to the dot plot, most FOMC members expect that it will be necessary to raise official rates by 75 bps up to the 5.00%-5.25% range, slightly higher than expected in September and much higher than anticipated just a year ago. The announcement was in line with what had already been signalled in the messages from the FOMC members, so it did not significantly alter investors’ expectations regarding the future path of official rates. In fact, the money markets continue to reflect expectations that the rate-reduction cycle will likely begin in the second half of the year. As for the dollar, despite the lower risk appetite it remained virtually flat in December; against the euro it was trading at around 1.06, the highest level since the summer and far from the parity seen in recent months. Meanwhile, the Japanese yen appreciated significantly during the month following the Bank of Japan’s unexpected decision to ease some of the parameters of its yield curve control policy, with an increase in the upper limit applied to the yield on the 10-year government bond from 0.25% to 0.50%.

In this context, the autumn rally in equities gradually lost steam and the main stock market indices ended the year with losses. Among advanced economies, the US indices led the decline (S&P 500 –6% in December and –20% in the year), followed by the European indices (EuroStoxx50 –4% and –12%, respectively), as the more defensive sectoral composition of the indices in Europe compared to in the US (i.e. less sensitive to the business cycle) cushioned the declines for the year as a whole. There were also big losses registered in emerging economies, with Chinese shares falling by around 20% amid slower economic growth and deteriorating investment flows from foreign portfolios. Looking ahead to the rest of the new year, the consensus of analysts anticipates slower growth in corporate earnings in both the US and Europe as a result of weaker aggregate demand and the extension of restrictive interest rates, which could undermine the positive effect of China’s reopening.

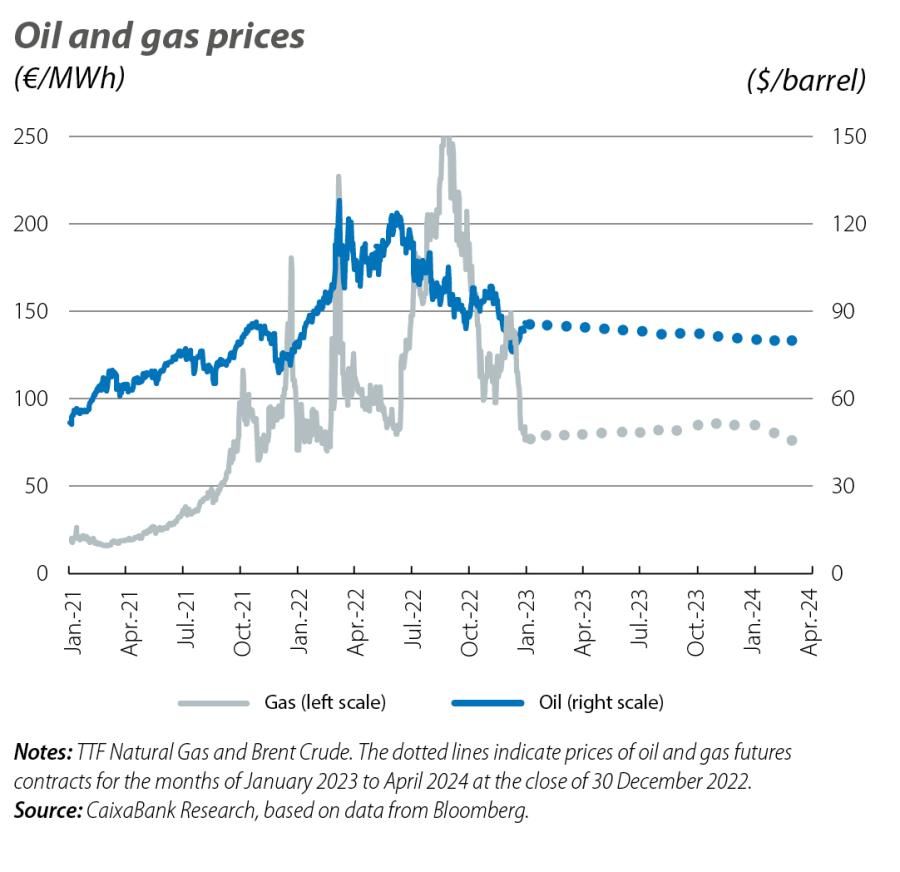

Unlike what happened for much of the year, energy prices stabilised in December and during the first sessions in January. European gas prices fell back to 2021 levels, due to milder-than-expected temperatures in the northern hemisphere and the high levels of gas reserves in Europe, which dispelled the risks of supply rationing. In addition, in December the EU agreed to set a cap on the price of gas, which will be activated if, for at least three consecutive sessions, the gas price (Dutch TTF) surpasses 180 euros per MWh and if the gap with respect to liquefied natural gas prices exceeds 35 euros. The Brent oil price, meanwhile, fell in the first few days of January to 80 dollars a barrel due to the combination of increased production in the US and Nigeria and doubts surrounding the possible weakening of demand in the face of the rise in COVID infections in China. Russia’s announcement of a 6% reduction in oil output during 2023 and a ban on exports to countries participating in the cap on its oil prices had little impact on the price.