Japan, at the dawn of a new cycle: fiscal tensions and monetary normalisation in the Land of the Rising Sun

Japanese sovereign yields have rebounded since 2022, particularly in the past year, and have exceeded the 2% threshold for the first time in nearly three decades. These movements have sparked a wide debate about the country’s fiscal sustainability and the direction of its monetary policy. In this article, we analyse the factors behind the recent upturn and its consequences for the Japanese economy.

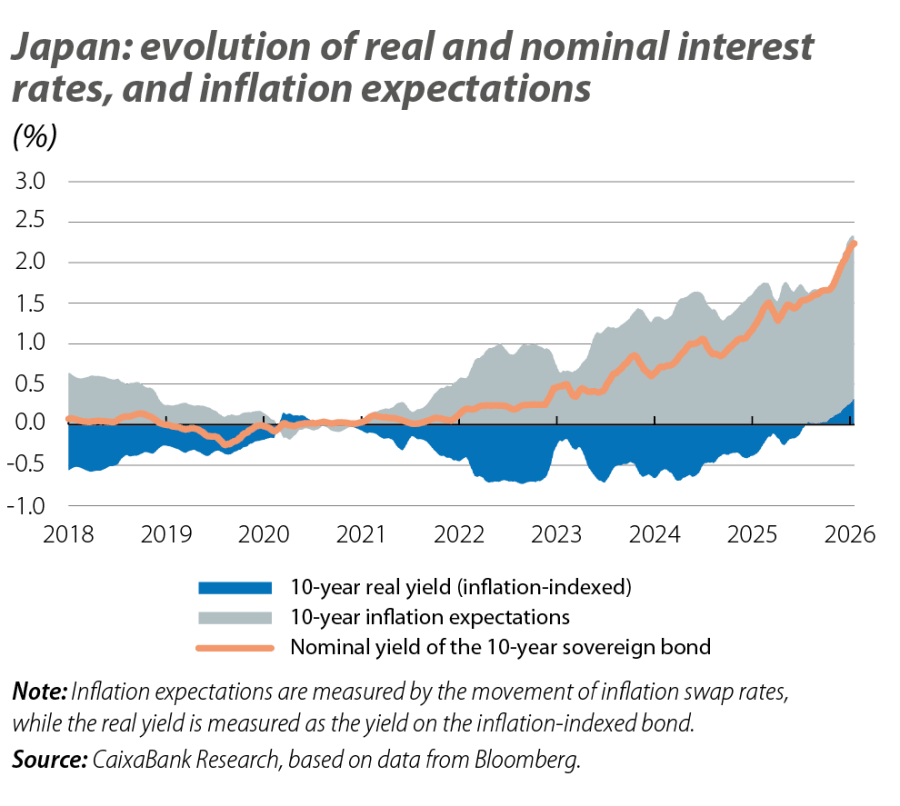

Evolution of interest rates in Japan: i = r+ πe

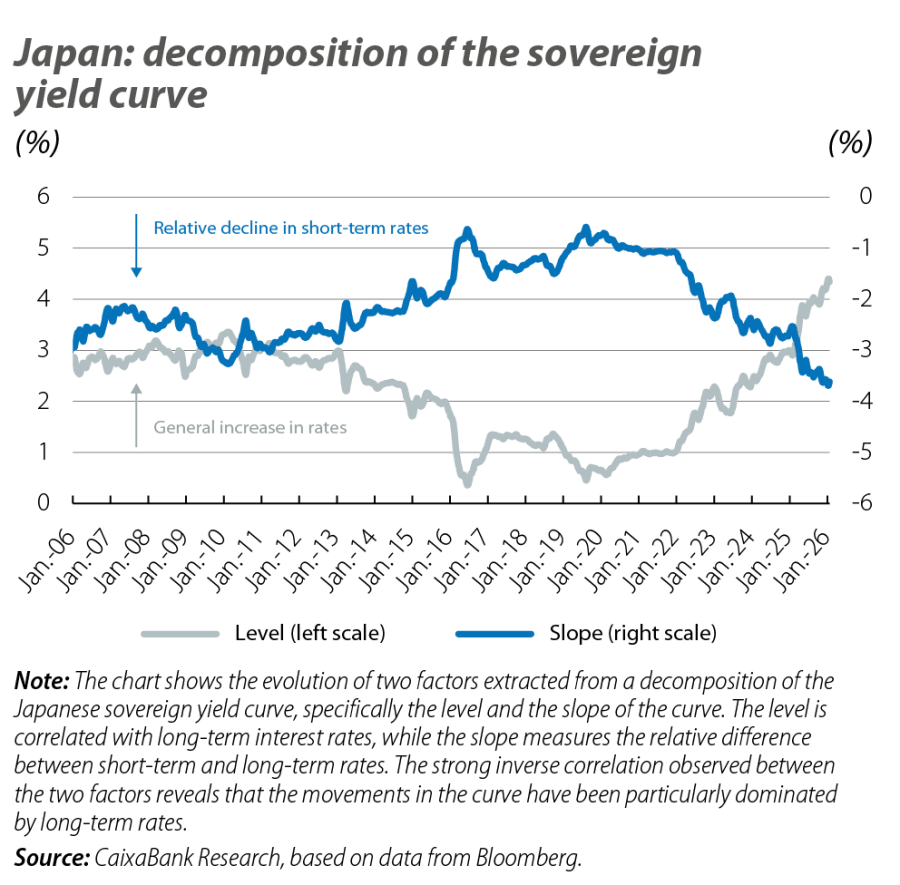

The rise in interest rates has been accompanied by a gradual normalisation of the Bank of Japan’s (BoJ) monetary policy and its control over the yield curve.1 This pattern can be broken down into movements in real rates and inflation expectations. The recent rise in nominal rates in Japan is mainly due to a sustained increase in long-term inflation expectations (see first chart). Since 2022, these have risen from levels of around 0% to a range of 1.5%-2% recently, alongside more persistent observed inflation (close to 3%, a level not seen since the early 1990s). This movement reflects underlying dynamics that go beyond the initial commodity shock that followed the outbreak of the Russia-Ukraine conflict, such as second-round effects, wage increases after years of stagnation,2 in addition to idiosyncratic factors (such as rising food prices, especially rice) and a depreciated yen.

- 1

In 2016, within the framework of the quantitative easing it had been carrying out since the early 2000s, the BoJ adopted a policy of sovereign yield curve control (YCC) in which it set a target (close to 0%) for the yield on the 10-year Japanese bond. This policy was gradually relaxed until it was eventually abandoned in 2024.

- 2

After years of wage rises of between 0% and 2%, an upturn began to be observed in 2023, during the shuntō spring negotiation process between large corporations and unions. In 2024 and 2025, the increases exceeded 5%, the highest since the early 1990s. Firms and unions are anticipating a similar or even greater wage rise in the shuntō of 2026.

In addition, real rates have also risen, going from around –0.5% to a range of 0%-0.5% at the long end of the curve. According to economic theory, this movement in real rates could be explained by various structural factors: higher potential growth, demographic changes that have structurally reduced savings and prospects of a sustained increase in investment. However, given the abruptness of the movement in the real rate, concentrated mainly in the last year, and the absence of significant changes in demographics or growth potential,3 the movement seems to be attributable to other factors. These might include an improvement in investment expectations (after a long period of corporate deleveraging and with greater dynamism in the real estate market) or changes in fiscal policy.4

- 3

Japan's GDP grew by 1.1% in 2025, and the IMF forecasts growth of 0.5% in the medium term, while the average growth in the period 2000-2019 was 0.8%.

- 4

Expectations of fiscal stimulus may translate into higher interest rates, both due to an increase in the term premium and through inflation expectations.

Fiscal policy in Japan: from Abenomics to Takaichinomics?

One of the keys to understanding the recent rise in sovereign rates lies precisely in the country’s fiscal situation. With gross debt of 230% of GDP and net debt (which subtracts government-held financial assets from the gross debt) reaching 130% of GDP, Japan has one of the highest debt ratios in the world. While the budget deficit is relatively low, the latest projections indicate a moderate deterioration in the medium term, reflecting pressures from spending on pensions, health and defence.5

In recent months, these factors have been compounded by Prime Minister Sanae Takaichi’s rise to power6 and an expansionist shift anchored in a rhetoric of a «proactive and responsible» fiscal policy. This includes increases in public investment and tax cuts, such as the temporary removal of the 8% levy on food – a key electoral promise with an impact estimated at around 0.8% of GDP per year.

- 5

The IMF projects a deficit trajectory going from 1.3% in 2025 (3.0% in 2019) to around 4.5% in 2030, while the primary structural deficit, which excludes interest payments and the change in the more volatile components associated with the business cycle from the fiscal balance, would stand at 2.5% in 2030, compared to the current level of 1% (vs. 2.6% in 2019). Despite the unfavourable demographics, the latest OECD projections place pension spending at around 10% of GDP by 2060, compared to around 9% currently – such an increase represents additional fiscal pressure that is in line with the OECD average (around +1 pp by 2060), but lower than in countries like South Korea (around +6 pps) or Spain (around +3 pps). The increase in defence spending is anchored in the discussion on the revision of Article 9 regarding non-belligerence, enshrined in Japan's Constitution since 1947, and in a geopolitical context marked by rising tensions with China and in the Pacific region, with Russia and North Korea as close neighbours.

- 6

This February, the Liberal Democratic Party secured a «supermajority» in the Lower House of Japan's parliament (316 seats out of a total of 465, plus 36 from its coalition partner, the Innovation Party).

Furthermore, beyond the country’s current fiscal position, the recent concerns may be linked to an increase in perceived risks regarding its long-term outlook, in the event that spending increases or tax cuts are not offset by other measures to balance the public accounts. In its preliminary report on Japan’s economy, the IMF has recommended maintaining a neutral fiscal stance, in a context in which the economy is operating above its potential, avoiding increasing cyclical pressures and preserving «buffers» against future shocks.7

- 7

The Fund mentions the tax cuts on food consumption as an ineffective measure that would increase fiscal risks. See «Japan: Staff Concluding Statement of the 2026 Article IV Mission» (17 February 2026).

Monetary policy in Japan: the BoJ faces new challenges

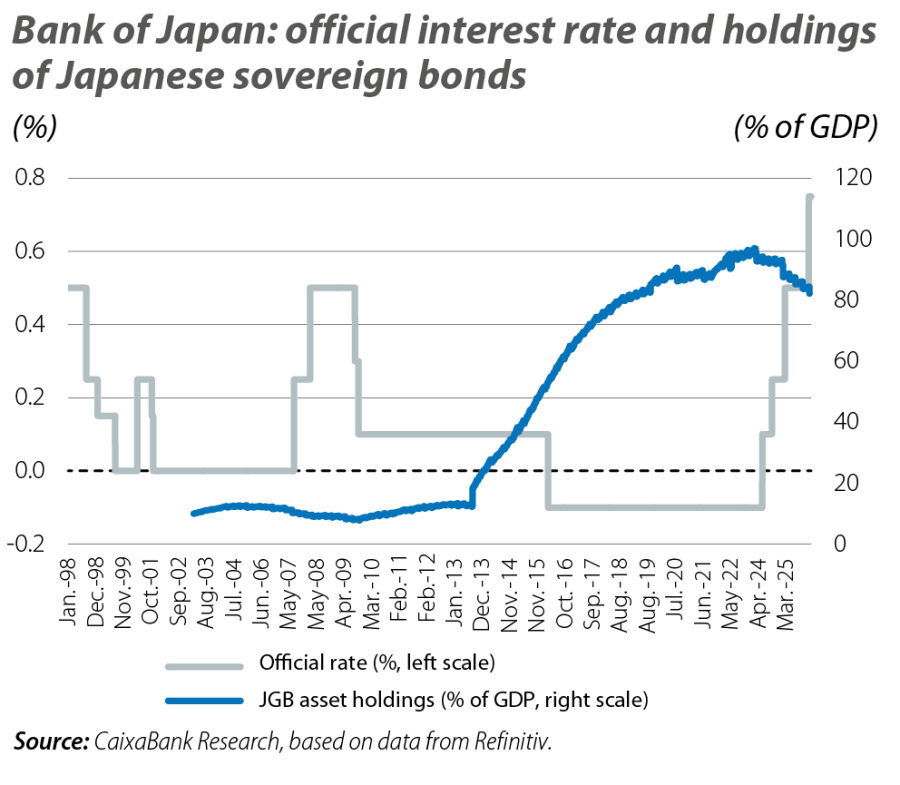

In this context, the BoJ is facing a structural shift in the macroeconomic environment. After many years dealing with deflation, the country has managed to exceed the 2% inflation target since 2022, and long-term expectations are anchored around that level. Thus, the BoJ has begun to adjust its monetary policy, abandoning its YCC policy in 2024, gradually raising interest rates and implementing a strategy of quantitative tightening, which reduces the pace of asset purchases, especially sovereign bonds (approximately half of Japan’s debt is held by the BoJ).

In its latest communications, the BoJ has reinforced its intention to pursue a gradual path of rate hikes. However, the difficulty of combining a restrictive monetary policy with expansive fiscal policies, in a high-debt environment, may become clearer in the future.