Spain’s foreign sector performed better than expected in 2025

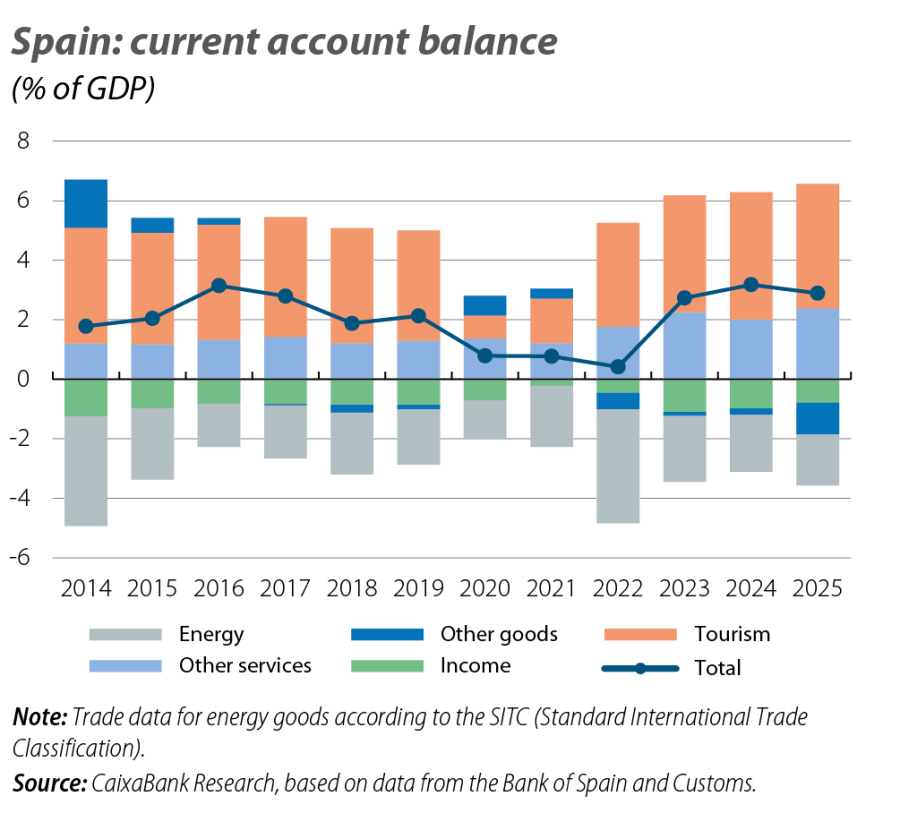

Despite the challenging international context of 2025, which foreshadowed a significant deterioration in Spain’s current account balance after showing uninterrupted surpluses since 2012, the balance has ended up being better than expected, thanks to favourable factors such as the containment of international energy prices and the dynamism of service exports, especially non-tourism services.

The challenging international environment in 2025 – marked by US tariff hikes, the slowdown in global trade and heightened uncertainty – foreshadowed a significant deterioration in Spain’s current account balance, which had been performing excellently with uninterrupted surpluses since 2012. These factors led us, in mid-2025, to revise downwards the current account surplus forecast to 2.3% of GDP. However, the balance has ended up being better than expected, thanks to other more favourable factors, such as the containment of international energy prices and the dynamism of service exports, including both tourism services and, above all, non-tourism services. Consequently, the deterioration of the current account balance was very limited, resulting in a surplus of 2.9% of GDP, just 0.3 percentage points below the historic figure of 2024.

By component, the deficit of the income balance in 2025 stood at 0.8% of GDP, slightly lower than the previous year’s figure (1.0%), but very similar to the average recorded since 2014. This balance, which shows a chronic deficit linked to the Spanish economy’s debtor position vis-à-vis the exterior,1 is mainly linked to interest and dividend payments to foreign investors (primary income) and to current transfers from the EU, notably the NGEU funds (secondary income). With still incomplete information (January-September), the sharp correction of the primary income deficit (–0.2% of GDP vs. –0.4% a year earlier), resulting from the fall in interest rates, contrasts with the stabilisation of the secondary income deficit (–0.7% of GDP).

- 1

See the Focus «The income balance suffers at the hand of the rate hikes» in the MR04/2024.

As for the trade deficit in goods, it rose sharply to 2.8% of GDP (2.1% in 2024),2 weighed down by the significant deterioration in the balance of non-energy goods, in a context of buoyant domestic demand that boosted imports, especially of capital goods, and a slowdown in foreign demand, in line with the weak performance of the euro area, the main destination for our exports. Other factors contributing to the weaker performance of exports include the strength of the euro (which appreciated by almost 14% against the dollar) and increased international competition, exacerbated by global tariff tensions and market diversification strategies. All this explains the meagre growth of Spain’s non-energy exports, of just 1.8%, a rate well below that of imports (6.7%). The energy balance, meanwhile, performed more favourably and its traditional deficit registered a significant correction, in line with the reduced price of imports (the price of a barrel of Brent oil fell by 18.6% in dollars).

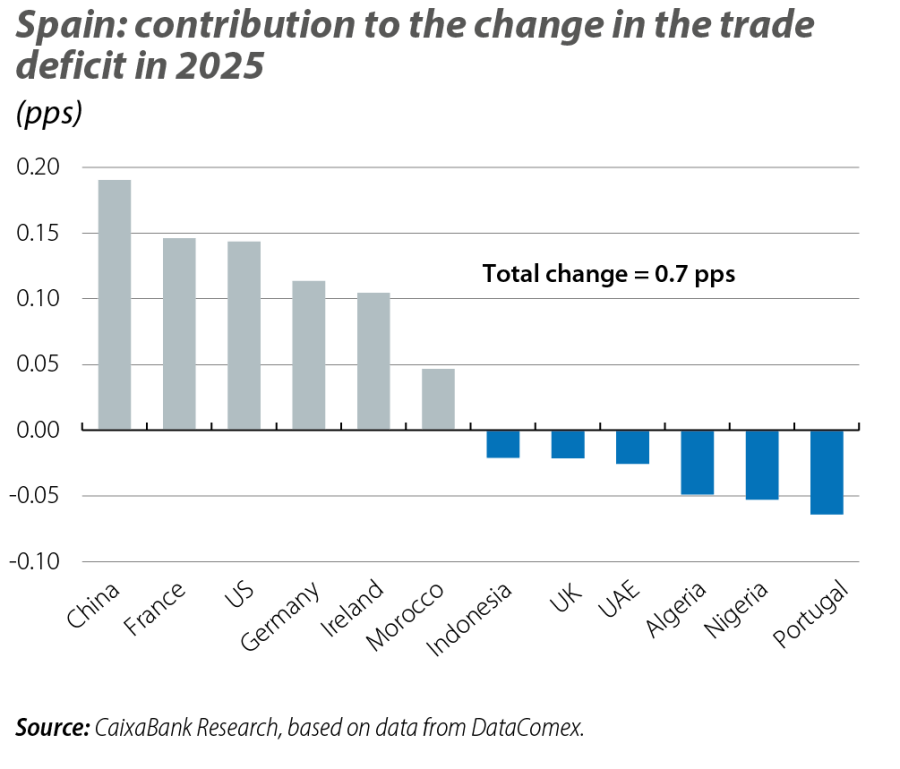

One of the key elements of the international landscape in 2025 was the US tariff hikes. The exposure of the Spanish export sector to the North American economy is limited (as of 2024, exports of Spanish goods to the US account for 1.1% of GDP, compared to 3.2% in the case of the EU), and this has cushioned the direct impact.3 However, the sharp decline in sales to the US (–8.0%), especially of oils, chemicals and crude oil derivatives, is compounded by vigorous imports (+7.0%), driven in recent years by the energy sector.4 This results in a notable widening of the trade deficit with the US, which, in turn, accounts for a substantial part of the deterioration in the overall balance of trade (see second chart).

- 2

This is an estimate, as the final data for the goods account of the balance of payments will not be known until 24 March. The balance in terms of the balance of payments is slightly different from the balance in terms of customs. For more information on the differences between the two, see the Focus «Excellent records in the foreign sector in 2024» in the MR03/2025.

- 3

For more information, see the article «Tariff tensions and reconfiguration of trade flows: impact on Spain» in the Sectoral Observatory S1 2025.

- 4

Since the outbreak of the war in Ukraine, dependence on US liquefied natural gas (LNG) has surged. See the Focus «The importance of the trade in goods between Spain and the United States» in the MR12/2024.

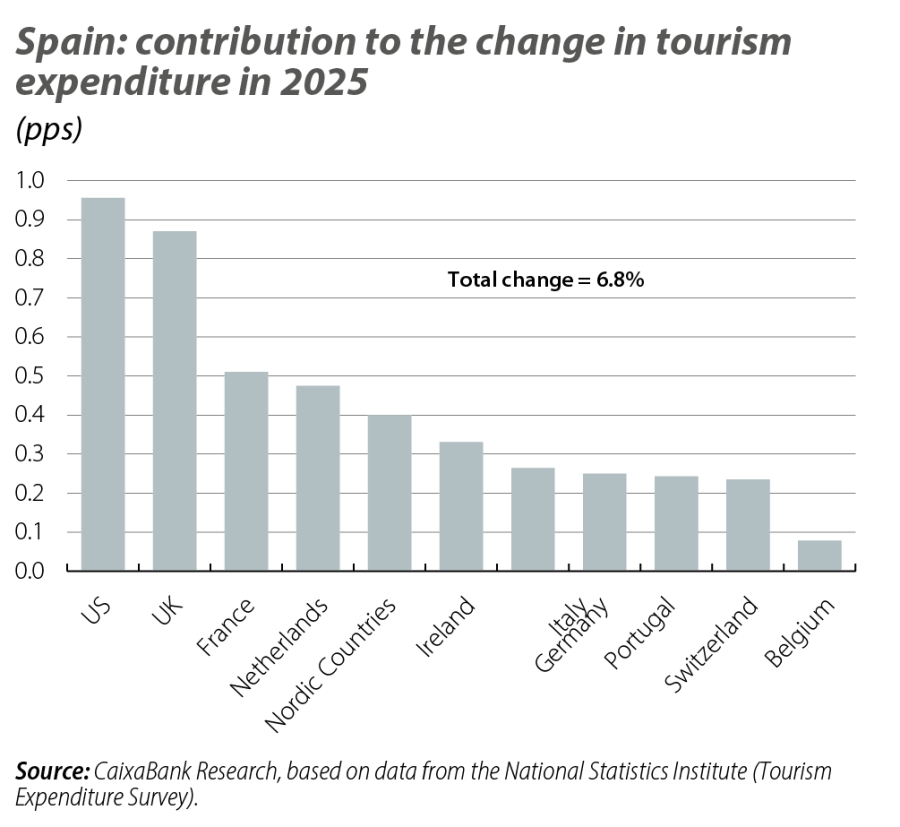

As for the balance of trade in services, it continues to register record surpluses. On the one hand, tourism has once again become the driving force of the current account, demonstrating great resilience despite the global economic slowdown, with a surplus that remained very close to its peak (4.2% of GDP vs. 4.3% previously).5 The depreciation of the dollar against the euro, meanwhile, did not reduce the influx of travellers from the US, which is one of the source markets with the highest average spending.6 On the contrary, it was the market that contributed the most to the growth of total expenditure and, among non-European markets, the one that contributed the most to the growth in tourist arrivals (see third chart).

As for non-tourism services, which have been gaining prominence in Spain’s foreign sector in recent years, they performed better than expected. Sectors such as transportation, financial services, consultancy, and digital services experienced very strong growth, supported by the growing trend of outsourcing among European firms and the consolidation of Spain as a hub for advanced corporate services. This dynamism allowed the surplus of this sub-balance to rise by 0.4 percentage points, to 2.4% of GDP, marking a new all-time high. With data up to September, exports are growing at twice the rate of imports (15.4% year-on-year vs. 7.7%), resulting in a 33.0% year-on-year surge in the surplus. By type of service, only intellectual property and insurance and pensions show deficits, while transportation has registered a notable improvement in its surplus.

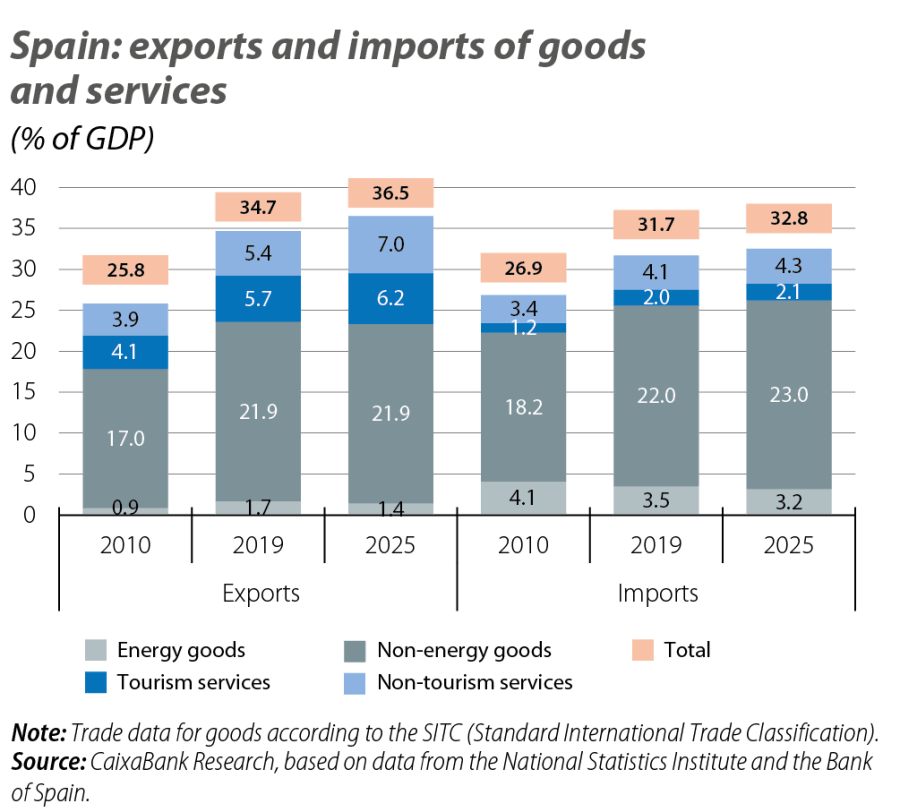

Ultimately, the 2025 data reinforce the diagnosis of a robust Spanish export sector. Taking a longer-term view, the current account surplus between 2023 and 2025 averaged 0.6 pps above the 2017-2019 average. The significant increase in recent decades in the share of non-energy goods and services exports – both tourism and non-tourism – (see last chart) reflects a growing diversification of the foreign sector. In this context, and as set out in the Focus «Spanish exports amid challenges to their competitiveness» in this same report, the deterioration of the balance of trade in non-energy goods this year seems to be primarily explained by the weakness of our main trading partners and by the increase in imports linked to the rebound in investment, rather than by a deterioration in competitiveness.