Increase in Spanish household savings in 2024

The savings of Spaniards went from 5,800 euros per household in 2023 to more than 7,000 in 2024. Why has the household savings rate increased and what do we expect for 2025?

Introduction

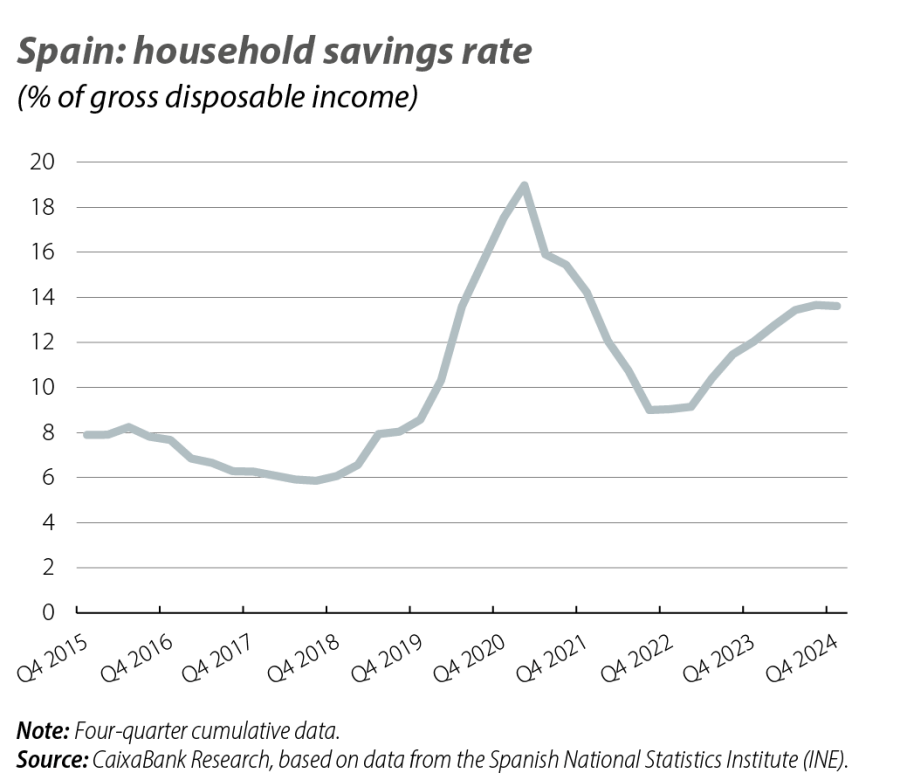

The household savings rate has increased in 2024, favoured by the sharp rise in disposable income. Specifically, the savings rate rose to 13.6% of gross disposable income (GDI), up from the 12.0% recorded in 2023 and the historical average of 8.6% between 2000 and 2019 (see first chart). This amounts to 139.9 billion euros of gross savings, 26 billion more than in 2022 and 86 billion more than the average for the period 2015-2019. If we look at savings per household, the figure has gone from 5,800 euros per household in 2023 to more than 7,000 in 2024.

Factors that explain the increase in the savings rate

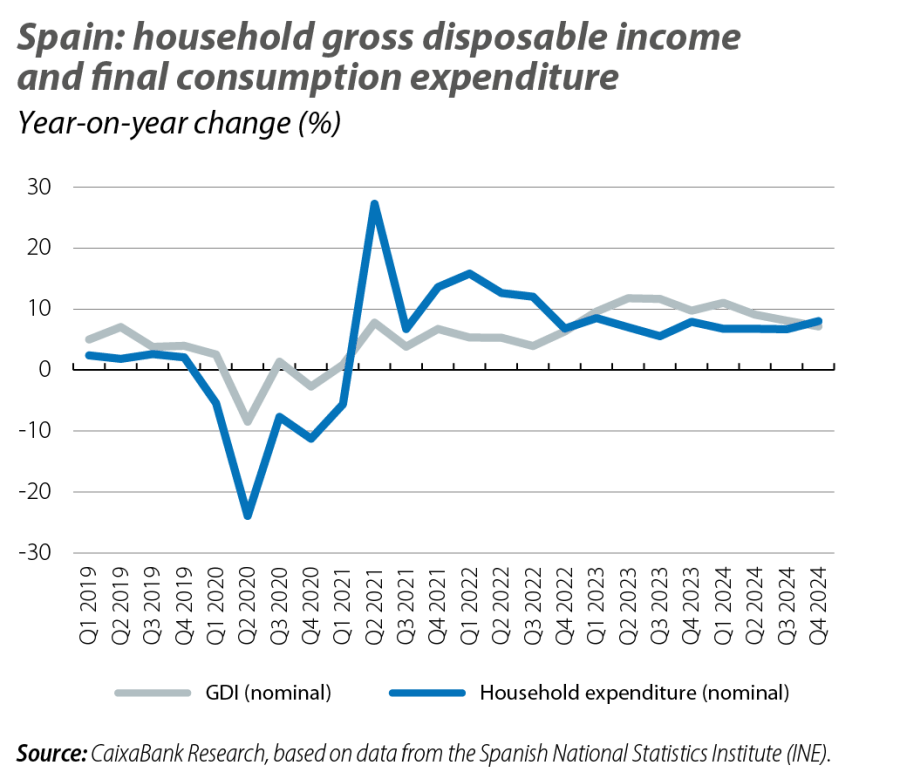

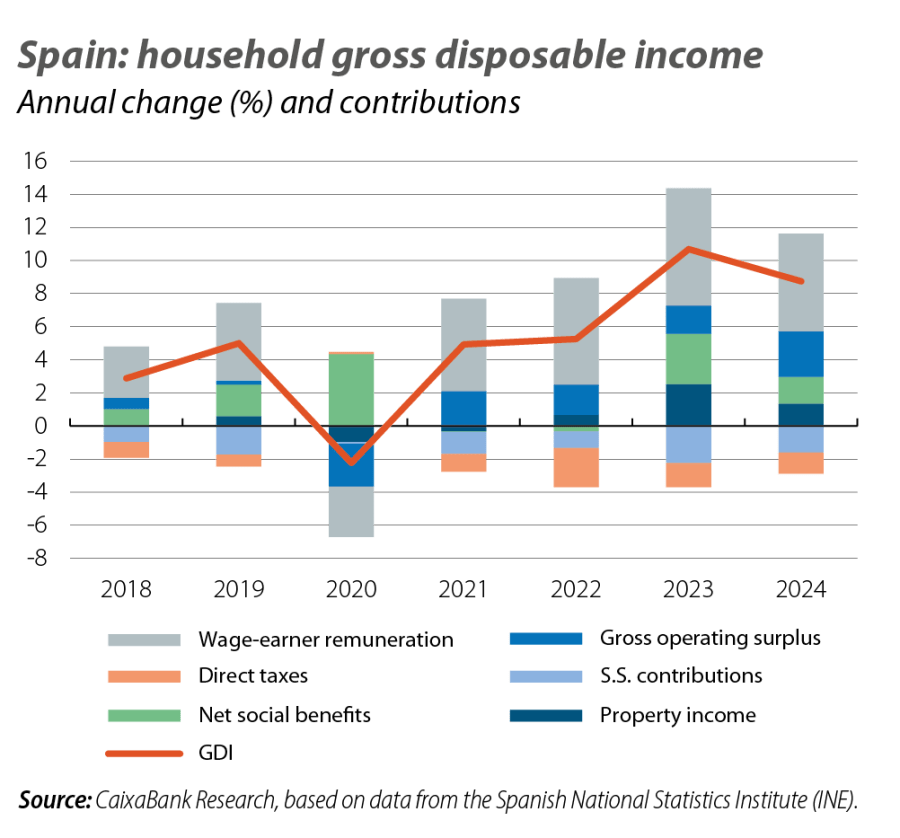

What is behind these figures? The increase in the savings rate has been driven by nominal GDI growth of 8.7% year-on-year. This is a dynamic growth rate, albeit slightly below that of 2023 (10.7%), and it is much higher than that recorded by household final consumption expenditure, which rose by 7.1% (see second chart). But what economic factors underlie these trends? The buoyancy of GDI has been due to a significant increase in wage-earners’ remuneration (7.7%), reflecting the intense job creation that took place in 2024 (resulting in an increase in the number of wage earners) as well as the strength of wages themselves, as indicated by the 4.7% rise in the remuneration per worker. Other factors that have also contributed to the rise in incomes include social benefits received, which increased by 5.9% year-on-year as a result of the growth in the number of pensioners and the pension rise of 3.8%, self-employment income and net property income, thanks to an increase in the collection of dividends and other investment income in an environment of high interest rates that stimulate savers. All this has more than offset the increase in the negative contribution of direct taxes and social security contributions paid (see third chart). Finally, for the year as a whole, net interest payments (14.45 billion)1 fell by 9% year-on-year and the debt burden represented 1.4% of GDI, versus 1.7% in 2023.

- 1Before financial brokerage services (SIFMI).

Gross disposable income outlook for 2025

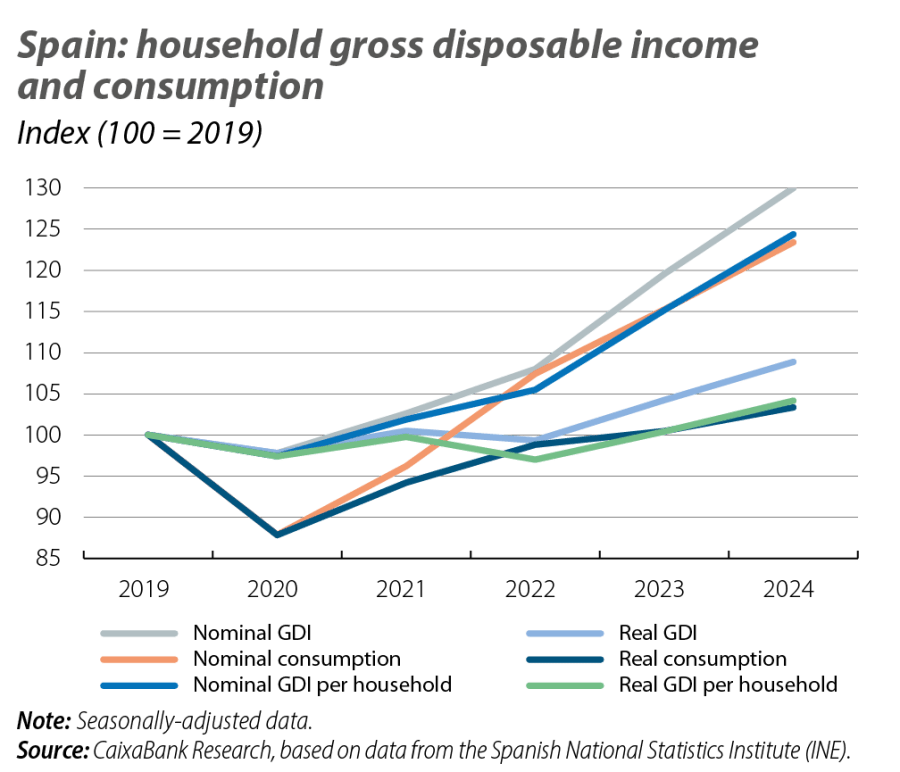

The increase in GDI clearly outpaced both average annual inflation (2.8%) and the growth in the number of households (0.7% according to the LFS) in 2024, enabling a recovery of purchasing power. Thus, in 2024 real GDI per household stood 4.1% above pre-pandemic levels, after having recovered that level in 2023, as shown in the fourth chart.

For this year, GDI growth is expected to remain dynamic thanks to the strength shown by the labour market. In fact, the final GDI figure for 2024 coupled with the good labour market data for Q1 2025 suggest that the growth of GDI could slightly exceed 5.0% this year. Such a growth rate is consistent with the good outlook in the labour market and the anticipated increase in pension spending, which AIReF estimates will reach 5.0% (2.8% due to pension rises plus 2 points driven by the replacement effect/new entries). Thus, if household spending registers a growth rate of around 6% – slightly lower than in 2024 in nominal terms due to the lower inflation – then the savings rate would be reduced by half a point this year to 13%. After the savings rate increased in 2024 with the rise in interest rates, in a context of falling rates it would be logical to see a decline in the savings rate. Other factors besides rates, such as uncertainty and differences between age brackets and income percentiles, help explain these high aggregate savings rates. According to a previous analysis by CaixaBank Research,2 households of retirement age and those with higher incomes are the ones that have experienced the biggest increase in savings relative to the pre-pandemic period.

- 2See the Focus «The rise in savings: magnitude, distribution and the importance of demographics» in the MR01/2025.

In Q4 2024, for the first time since Q4 2022, nominal GDI growth was lower than that of final consumption expenditure, indicating that in 2025 the savings rate is likely to decline. In Q4 (for the quarter only), nominal GDI grew by 7.2% year-on-year (8.1% in Q3), while final consumption expenditure grew by 8.0% (6.7% in Q3), reflecting the greater dynamism of private consumption in real terms. In order for these dynamics to consolidate this year, it is important that uncertainty, which has spiked as a result of the trade tensions, returns to more moderate levels.

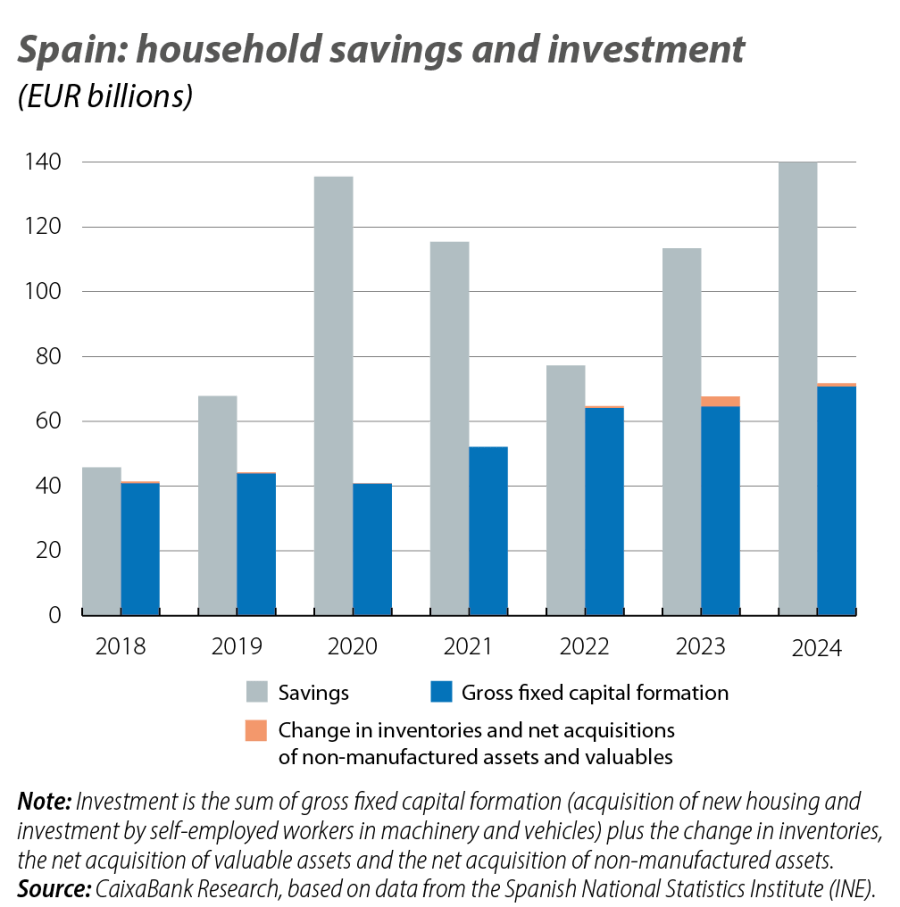

Finally, households’ lending capacity surged in 2024, going from 44.6 billion euros in 2023 to 74.4 billion euros in 2024. The reasons behind this increase include the higher savings (increase in gross savings from 26 billion to 139.9 billion) and the smaller relative increase in investment by households: gross fixed capital formation, which includes real estate purchases (new construction) and investment in physical assets by self-employed workers, stood at 70.7 billion euros in 2024, 6 billion more than in 2023. However, according to these statistics, investment is beginning to pick up following the revival of the housing supply: its growth stood at 9.5% year-on-year in 2024 after stagnating in 2023. In short, the strength of the labour market paved the way for a significant increase in household GDI in 2024. This increase, together with a more moderate pattern in spending despite its gradual revival, enabled significant growth in household savings.