Spain in the face of the new energy shock: a comparison with Europe

The recent escalation of the conflict in the Persian Gulf, with the outbreak of the war in Iran, has once again placed energy at the centre of the global economic agenda. Although the scope and duration of the conflict remain uncertain, markets, especially those for oil and natural gas, have reacted swiftly. In this context, we analyse where the Spanish economy stands in the face of this new energy shock.

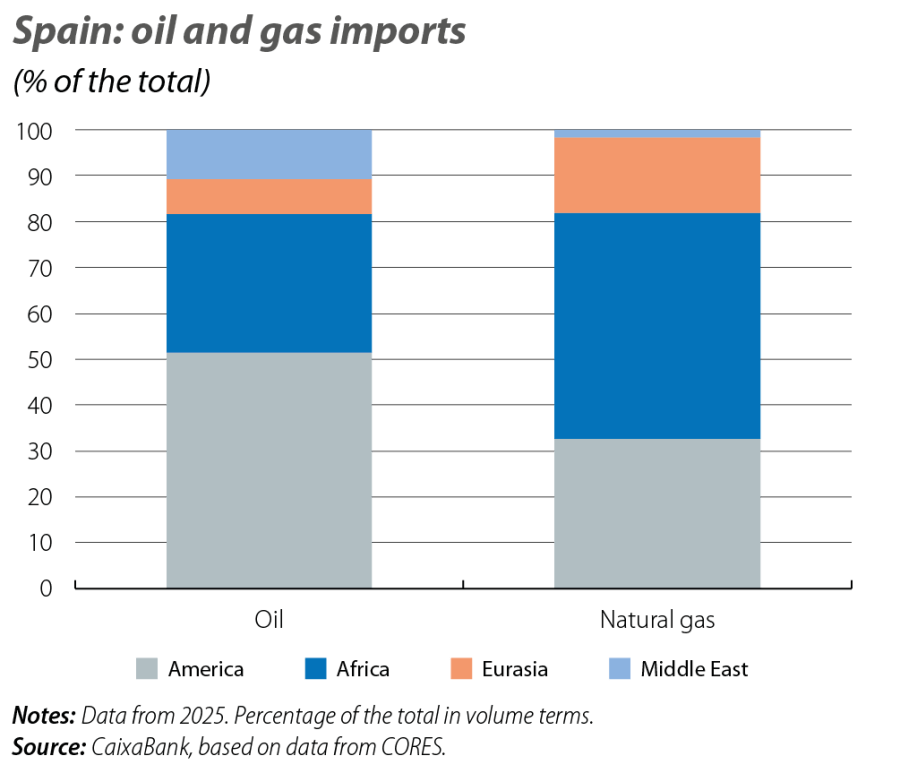

From a supply perspective, one of Spain’s main strengths is its low direct exposure to the Persian Gulf. Around 10% of the country’s oil imports come from the region (mainly from Saudi Arabia and Iraq), while for natural gas this percentage is less than 2%, primarily from Qatar. This limited dependency reduces the risk of physical supply disruptions. However, the global nature of these markets means that a sustained increase in geopolitical tensions is reflected in prices regardless of the origin of the imports.

Compared to the EU as a whole, Spain has a slightly lower exposure to the Persian Gulf, but a greater dependence on Algeria and Nigeria for oil and gas imports, as well as on the US in the case of gas. The important role of Algeria as a source of gas imports represents a comparative advantage, as it is primarily transported via pipeline. This type of supply is less likely to be redirected to other markets and, therefore, tends to be more stable than liquefied natural gas (LNG). Moreover, this lower capacity to be redirected, together with the absence of costs associated with liquefaction and regasification, tends to result in a lower price compared to LNG.

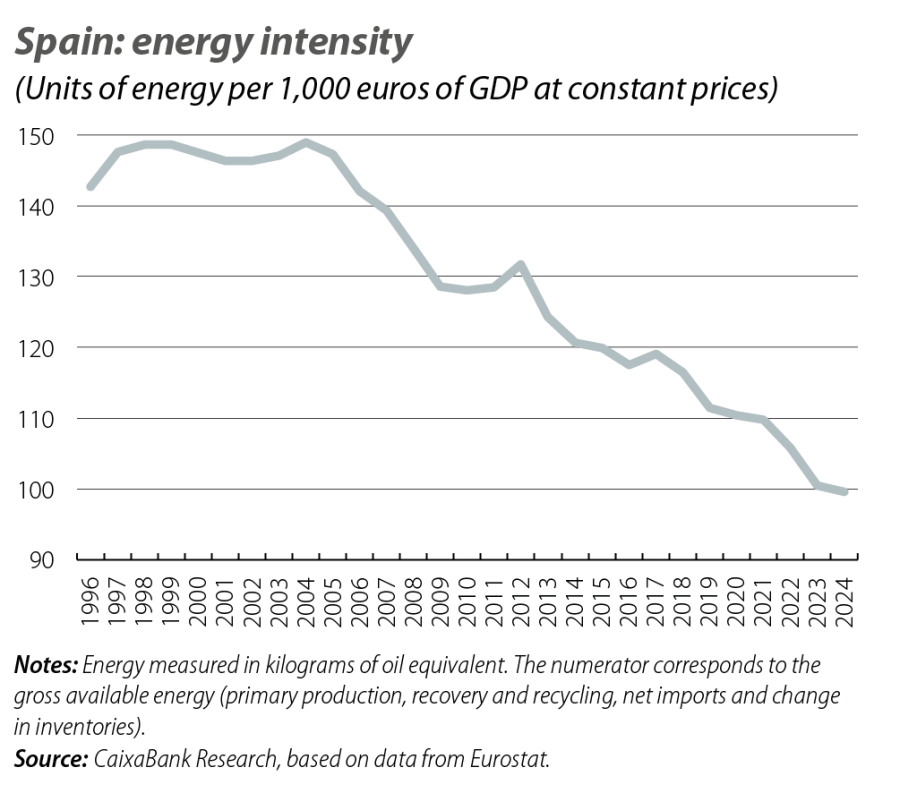

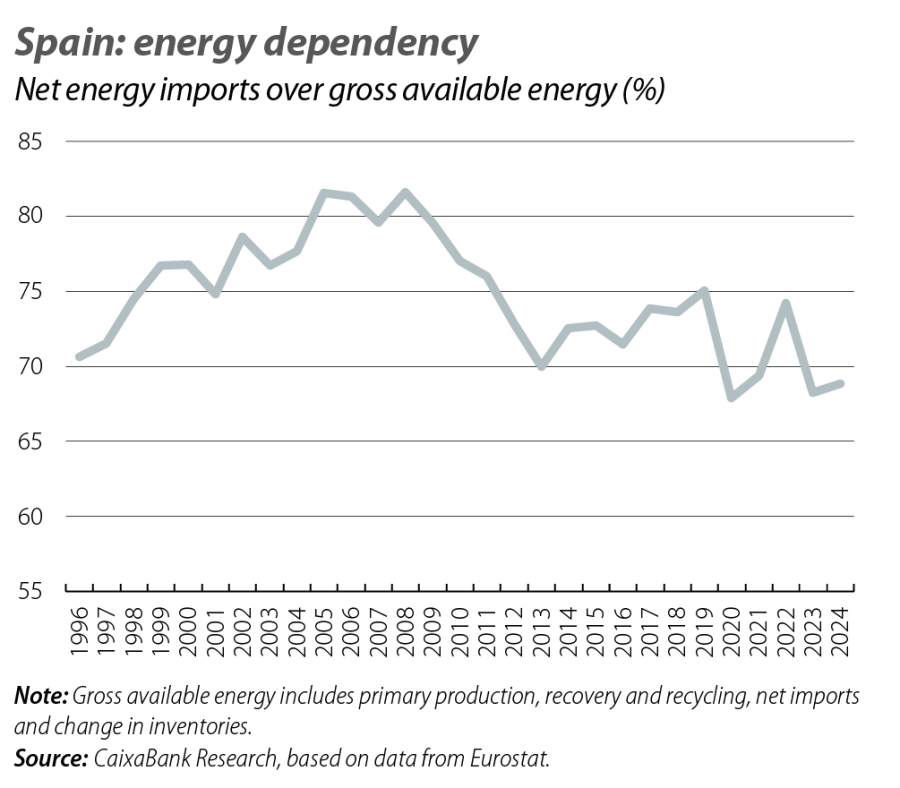

Another relevant structural factor is the accumulated improvement in the energy efficiency of the Spanish economy. Since the beginning of the century, energy intensity, measured as the amount of energy required to generate 1,000 euros of GDP at constant prices, has decreased by about a third. This progress helps to cushion the macroeconomic impact of rising energy costs by limiting the increase in production costs and, ultimately, in final prices. Opposing these favourable elements, Spain’s main weakness remains its high energy dependency on foreign sources: 70% of the country’s energy needs must be met through imports, a rate that is only 5 percentage points lower than at the turn of the century.

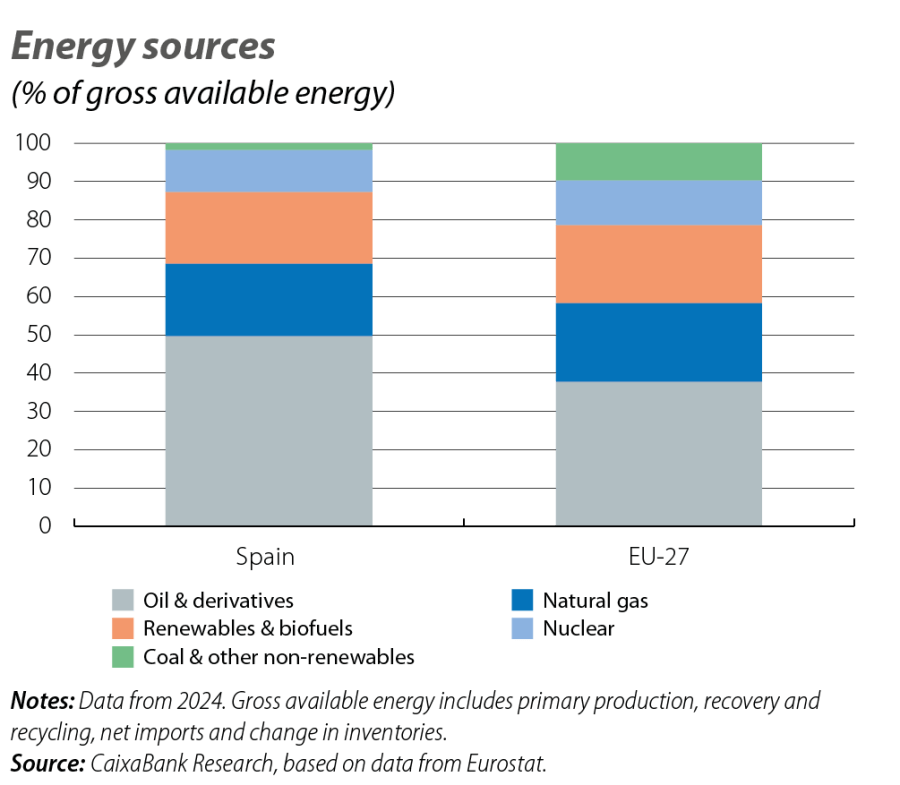

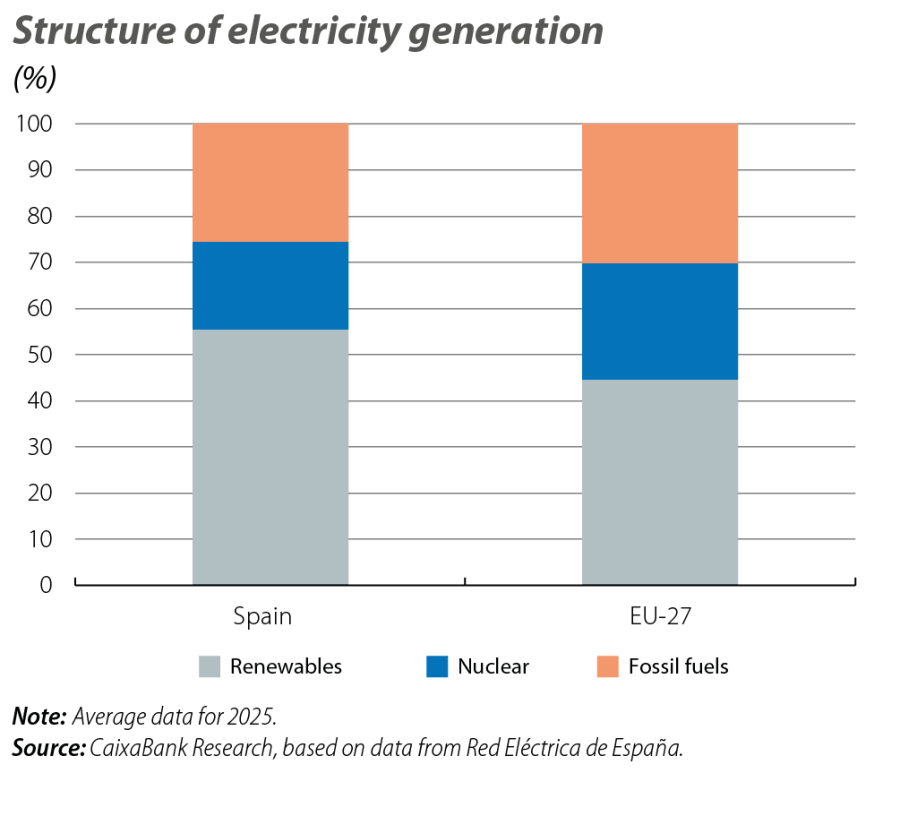

In terms of energy intensity, Spain is very close to the European average. Where significant differences are observed is in the total energy dependency, which is higher in Spain than in the rest of Europe. As we can see in the fourth chart, Spain meets its energy needs to a greater extent with imported petroleum products, whereas in the rest of Europe these are largely met with coal, of which there are significant reserves on the continent, particularly in Germany and Poland.1

- 1

It may be surprising that the combined weight of renewable energies and biofuels in the gross available energy is not greater in Spain, given its relative advantage in electricity generation. This apparent discrepancy is explained by the fact that electricity generation is only one part of the total energy system, while other uses such as transport continue to show a high dependence on petroleum products.

The electricity market: the Iberian exception

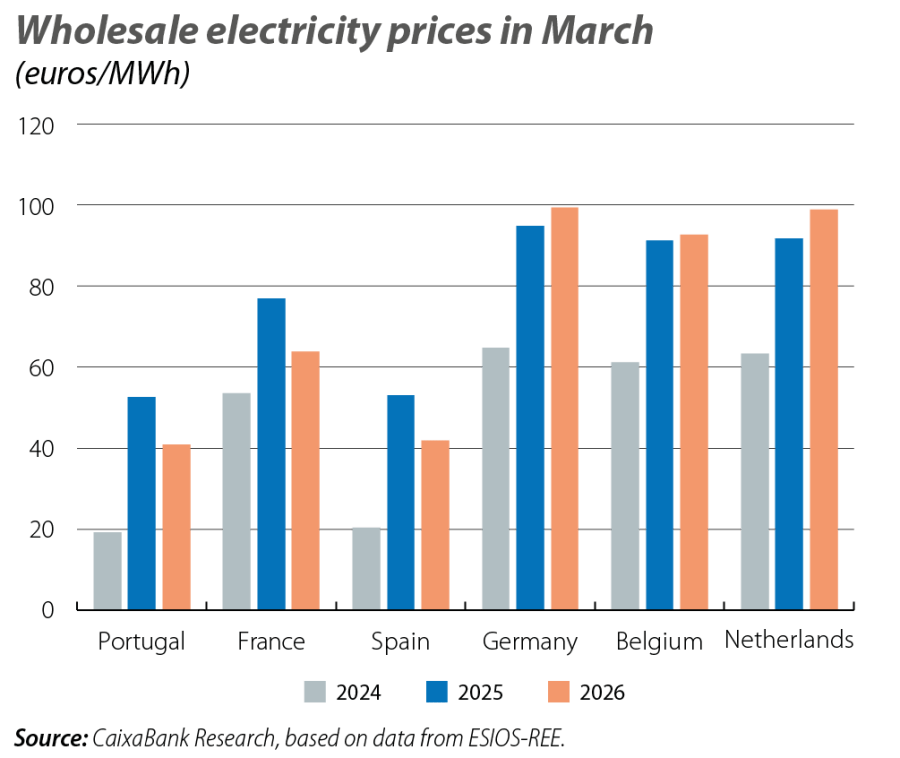

The wholesale electricity market is one of the main strengths of the Spanish economy in the energy sector relative to the rest of Europe. Unlike oil or gas, the European electricity market is less homogeneous, so external shocks are not transmitted in the same way across all countries.2 Despite the energy tensions, the wholesale price of electricity on the Iberian Peninsula actually decreased in March in year-on-year terms, unlike in other European countries, and it was also well below the levels observed in Northern Europe (see fifth chart).3

- 2

It is important to clarify that the final price which consumers pay for electricity includes various fixed costs (tolls, charges, taxes) that significantly increase the total bill, which means that Spain’s electricity market represents a comparative advantage mainly for electricity-intensive companies. The National Commission on Markets and Competition (CNMC) estimates that these costs account for around two-thirds of the bill for domestic consumers, while for industrial consumers they represent less than half of the total.

- 3

Due to the strong seasonality of electricity prices, month-on-month comparisons are not informative.

This pattern is mainly due to the greater share of renewable energies in electricity generation on the peninsula. The European electricity market operates under a marginal system, where the technology that is required to cover the last unit of demand is the one that sets the price. The greater presence of renewables in our economy means that there are more time slots during the day when this source becomes the marginal energy. Given that renewable energies have very low marginal costs, especially compared to natural gas combined cycle power plants, this tends to reduce the price.4

- 4

Also, even when combined cycles set the electricity price, the relatively advantageous position in gas supplies limits the increase in costs compared to other countries.

Overall, although the war in Iran introduces a new focal point of tension in international energy markets, the limited direct exposure to the Persian Gulf, advances in energy efficiency, and advantages in the electricity market all place the Spanish economy in a favourable position to absorb the shock. However, the country’s high dependence on foreign energy remains a source of vulnerability. This balance indicates that, although Spain remains exposed to a price shock, it has certain structural elements that could mitigate its impact compared to recent episodes.

Climate change & green transition

What polices can be implemented to stop climate change? What are the implications of shifting towards a more sustainable economy?