Spanish exports amid challenges to their competitiveness

We analyse the price and cost competitiveness of export sales, as well as Spain’s current share of exports in a global scenario marked by rising trade tensions where the margins for competition appear to be narrowing.

In the last three years, Spain’s foreign sector has significantly improved its position: the current account surplus went from representing 0.4% of GDP in 2022 to nearly 3% of GDP in 2025, which reflects a greater lending capacity relative to the rest of the world. However, this improvement has occurred in a context in which Spain’s inflation has remained slightly above the euro area average over the last two years, as well as coinciding with an appreciation of the euro against the dollar in this period. In light of the potential increase in export prices resulting from these conditions, we assess the impact on the price and cost competitiveness of export sales and we analyse Spain’s current share of exports in a global scenario marked by rising trade tensions where the margins for competition appear to be narrowing.

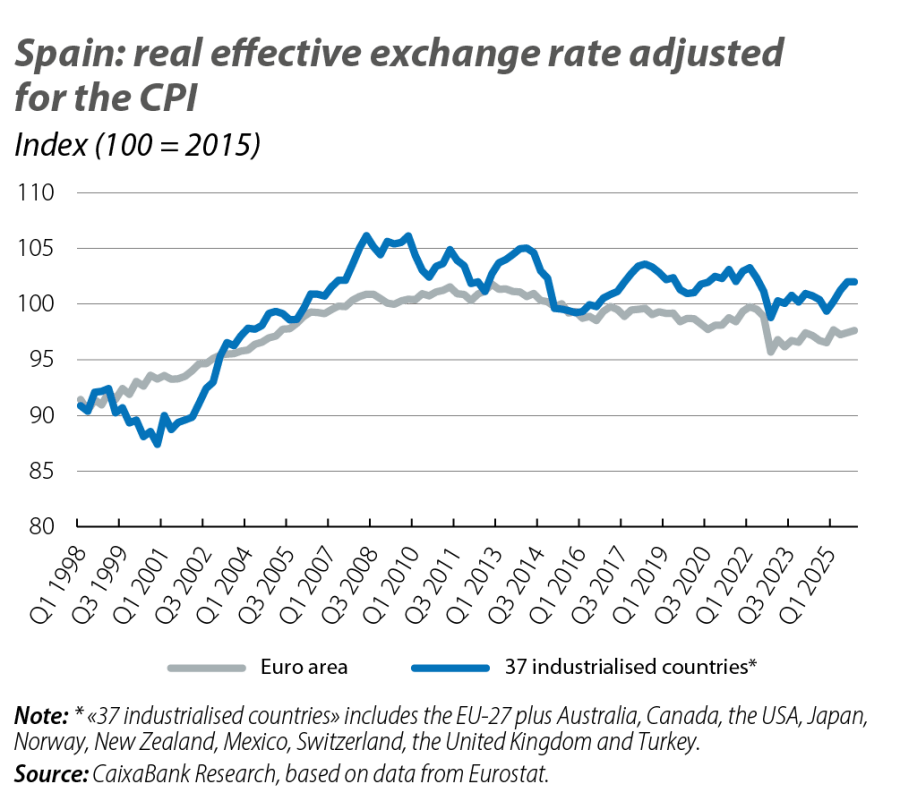

As a measure of price competitiveness, we will use the real effective exchange rate (REER), which measures Spain’s nominal exchange rate averaged against a set of trading partners, adjusted for relative inflation according to the harmonised index of consumer prices. The adjustment for inflation captures the differences in consumer prices between Spain and its counterparts. Therefore, if the REER rises, it means that Spain loses competitiveness, as its exports become more expensive and imports become relatively cheaper, and vice versa.

In the first chart, we compare the REER against the euro area and a group of 37 industrialised countries. In comparison with the euro area, given that Spain shares the same currency, the nominal exchange rate component does not operate and the reading equates to a comparison of relative prices. Following a turning point in the last quarter of 2022 (when inflation in Spain rose less than in other euro area countries), we see a modest deterioration in competitiveness until the last quarter of 2025, which leaves us, nevertheless, in a more competitive position than we had in 2019. Against the group of 37 countries, the recent rise in the REER is more pronounced due to the impact of the appreciation of the euro. Even so, we remain at levels comparable to the pre-pandemic situation.

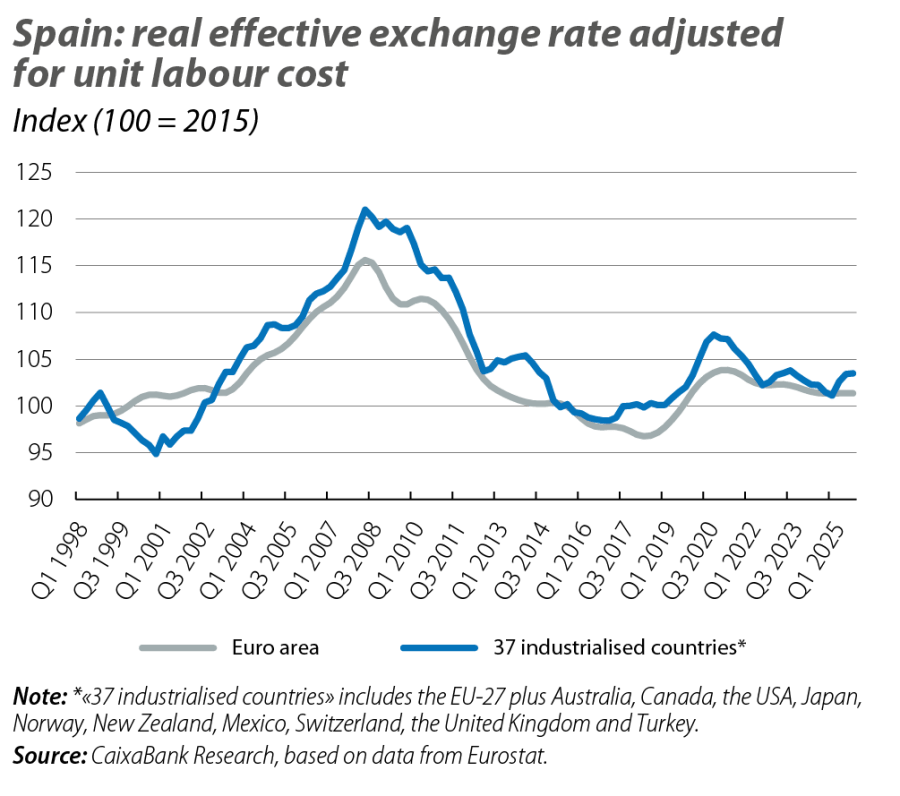

On the other hand, we can also analyse the evolution of the REER deflated by the unit labour cost (ULC) index instead of inflation. This allows us to assess whether, from the production side, there is any pressure arising from the relationship between wages and productivity that could contribute to a relative increase in costs compared to other countries. In the second chart we can see that, following a peak in the REER during the COVID-19 pandemic due to the sharp rise in ULCs, Spain has clearly regained competitiveness against euro area costs, although it is in a worse position than in 2019. Against the group of 37 industrialised economies, the improvement that occurred in 2020 has gradually moderated and, after a slight upturn in 2025, the current position is similar to that of 2019.

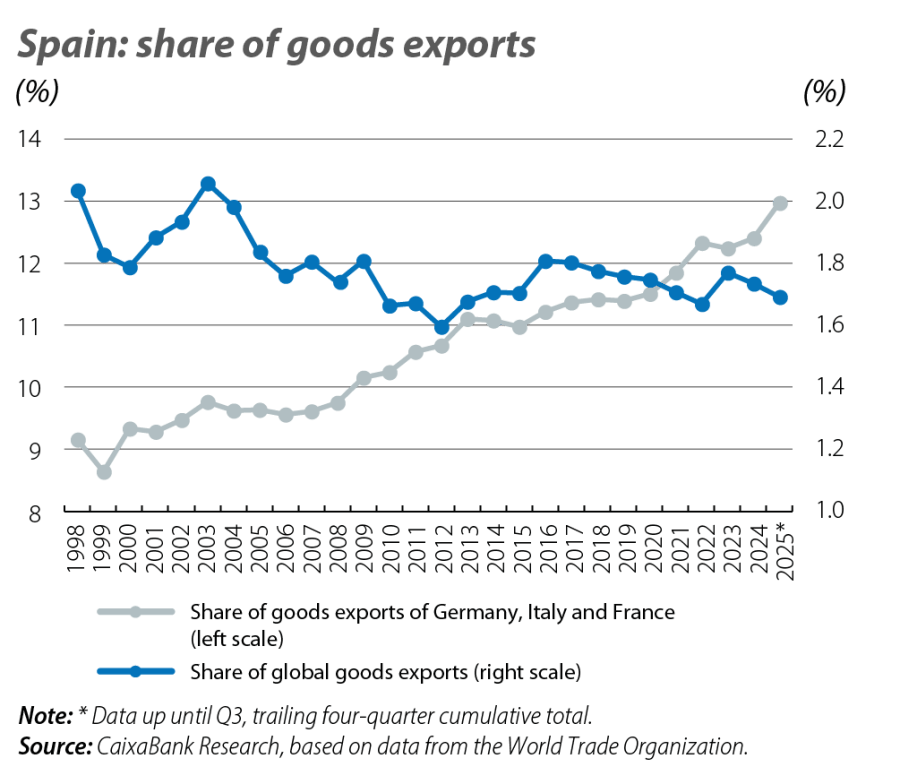

Taken together, the two charts present a nuanced picture: on the side of final prices, there is solid competitiveness, while the recent slight loss is more attributable to labour costs, which have evolved more favourably compared to the euro area than against the group of 37 industrialised economies, in turn highlighting the effect of the exchange rate appreciation. In order to determine whether these tensions have actually resulted in a setback in our external position, we complement the analysis by examining the evolution of Spain’s share of exports of goods and services. This measure is useful because competitiveness can be assessed not only in terms of prices and costs, but also from the perspective of other dimensions such as innovation, complexity or the level of technology of exports.1 In this regard, the export share reflects how the set of factors that influence international trade ultimately materialises in foreign sales.

In the third chart, of particular note are Spain’s gains over time compared to Germany, Italy, and France: Spain’s share of this group’s exports of goods has continued to increase and now stands at 13%, compared to 11.4% in 2019. This improvement is explained by the fact that, in the period 2020-2025, Spanish exports of goods grew by 30%, compared to a growth rate of 12% in these three countries as a whole. Spain’s share of global trade, meanwhile, has remained stable at around 1.7% in recent years, indicating that Spain has not lost its presence in the global trade of goods despite the inflation and exchange rate dynamics. This ability to maintain market share during this period is even more noteworthy in a context in which the export share of China, and of other Asian economies such as Vietnam and Taiwan, has grown inexorably.

- 1

See the Focus: «Is technology and complexity exported from Spain?» in the MR07/2025.

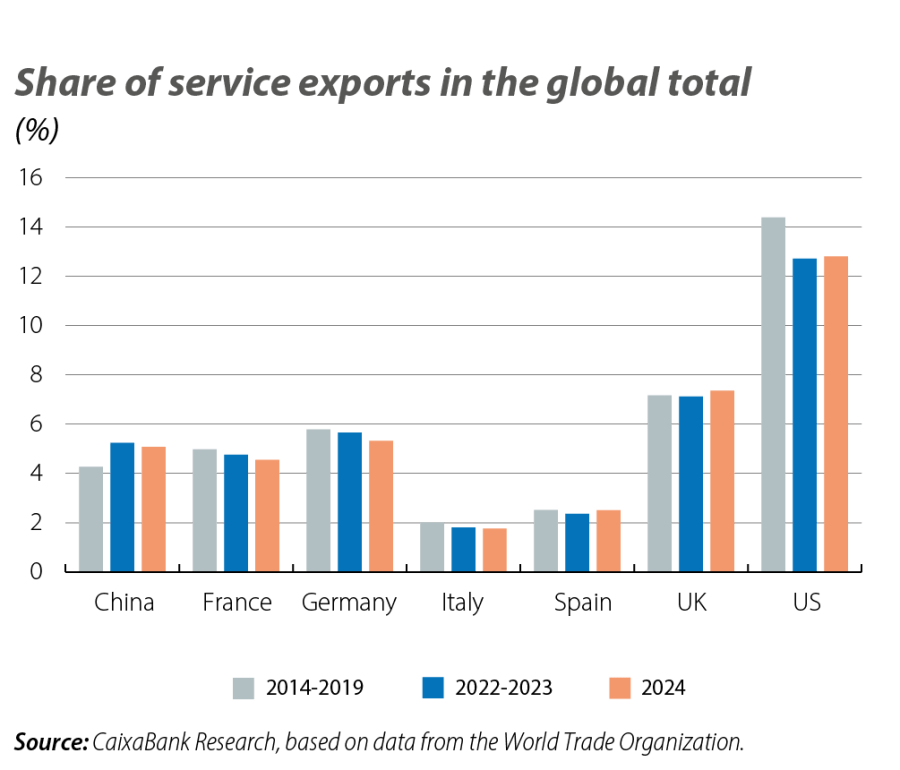

Regarding the share of service exports in the global total, in the last year Spain has regained its pre-pandemic level – a particularly positive result when compared to Germany, Italy and France, which are losing share. In parallel, the US, despite remaining the leader in the sector, is losing some ground in the global distribution, while China and the United Kingdom have gained share in recent years. If we analyse tourism services in particular, Spain’s performance is especially impressive. Our global share stands at around 6%, ahead of France (around 4%), Italy (3.5%) and Germany (2.5%), and 1 pp above the level recorded in 2019, consolidating Spain as one of the main exporters of tourism services in Europe. If we focus solely on non-tourism services, following the exceptional growth of the sector since 2021, we find that Spain has managed to maintain its market share in an environment with Germany, Italy, France, and the US in retreat. That said, it has not improved this share either, given that the volume of global exports has also increased sharply.

Taken together, the indicators analysed suggest that, despite the inflation gap and the appreciation of the euro in recent years, there has been no significant deterioration in Spain’s external competitiveness. This, combined with a stable or rising share of exports in both goods and services, suggests that the Spanish economy has managed to maintain its competitive position in a challenging environment. This performance could be associated with a diversification effort by our export sector, or with the ability to compete in other dimensions, which may have partially offset the impact of higher relative prices. All this becomes even more relevant in a global environment in which China continues to expand its influence and where several European economies and even the US have lost ground.