Spain: key drivers of regional growth in 2026

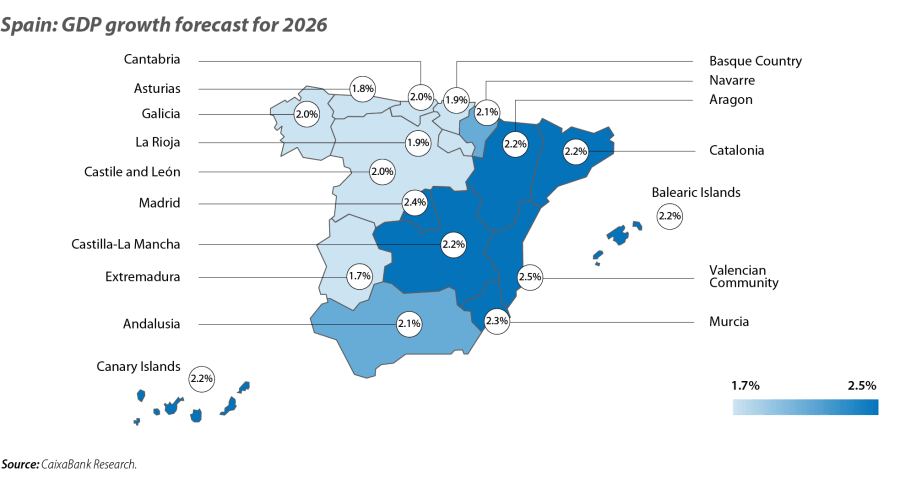

The new GDP growth forecast by autonomous community for 2026 presents a mixed picture: the regions of the Mediterranean arc and the archipelagos will experience stronger growth, while the Cantabrian coast and much of the interior will record more modest rates.

This disparity is explained by a combination of structural and demographic differences, as well as unequal exposure to external shocks. In regions where domestic demand plays a more important role, the boost from consumption and services – further bolstered by strong demographic expansion – allows growth rates to remain above average. In contrast, regions with a greater focus on energy-intensive industries and higher exposure to external markets will experience slower growth, hindered by rising production costs and weak external demand.

Population growth, primarily driven by immigration, has become a key pillar of the business cycle. On one hand, it boosts domestic demand by increasing consumption and accelerating household formation; on the other, it expands the labour supply, increasing the workforce and allowing employment to remain dynamic. This dual lever helps explain why regions with more intense population growth show stronger economic activity, and together it acts as a buffer amid a more adverse international environment.

On the other hand, geopolitical uncertainty enhances Spain’s appeal as a safe tourist destination, redirecting a portion of the flows of international travellers to the country. This context raises the tourism sector’s prominence as a driver of regional growth, providing a particularly strong boost to the islands and Mediterranean regions, which already have very dynamic tourism sectors, as well as the regions of so-called «Green Spain», which are attracting more domestic visitors as an alternative holiday destination.

In contrast, the energy shock triggered by the conflict in the Middle East is having a bigger impact on manufacturing regions. The industrial regions of the north, which are highly specialised in semi-manufactured and capital goods, are facing rising costs in sectors such as steel and chemicals. In turn, the weakness of the European economy and trade tensions are particularly affecting regions that are more exposed to markets and products subject to tariff hikes.

Nevertheless, the Spanish economy has significant buffers. The final execution of the Next Generation EU funds in 2026 will continue to serve as a key driver of investment in several regions. New growth drivers are also emerging: for instance, increased defence spending could provide a boost in regions with a military and technological industrial base.

Ultimately, each region faces the shock with its own strengths and vulnerabilities, but overall, the resilience of Spain’s domestic market remains a key source of support for regional growth in 2026.