The international economy once again follows developments in the US

Geopolitical events have once again taken centre stage, almost relegating to the background the assessment of the economic indicators published over the past month. The US attack on Iran has caused a spike in geopolitical instability and economic uncertainty, opening up a new source of risk in an environment characterised by the transactional stance of the Trump administration and the erosion of multilateral institutions.

Geopolitical risk intensifies and trade uncertainty resurfaces

Geopolitical events have once again taken centre stage, almost relegating to the background the assessment of the economic indicators published over the past month. The US attack on Iran has caused a spike in geopolitical instability and economic uncertainty, opening up a new source of risk in an environment characterised by the transactional stance of the Trump administration and the erosion of multilateral institutions. The impact of this conflict will depend on its duration and geographical scope, but Iran's response has already triggered a sharp rise in energy prices. Iran is the fourth largest crude oil producer in OPEC (3.3 million barrels per day, 3.3% of global production) and it has strategic control over the Strait of Hormuz, through which over 20% of the world's maritime energy trade passes.

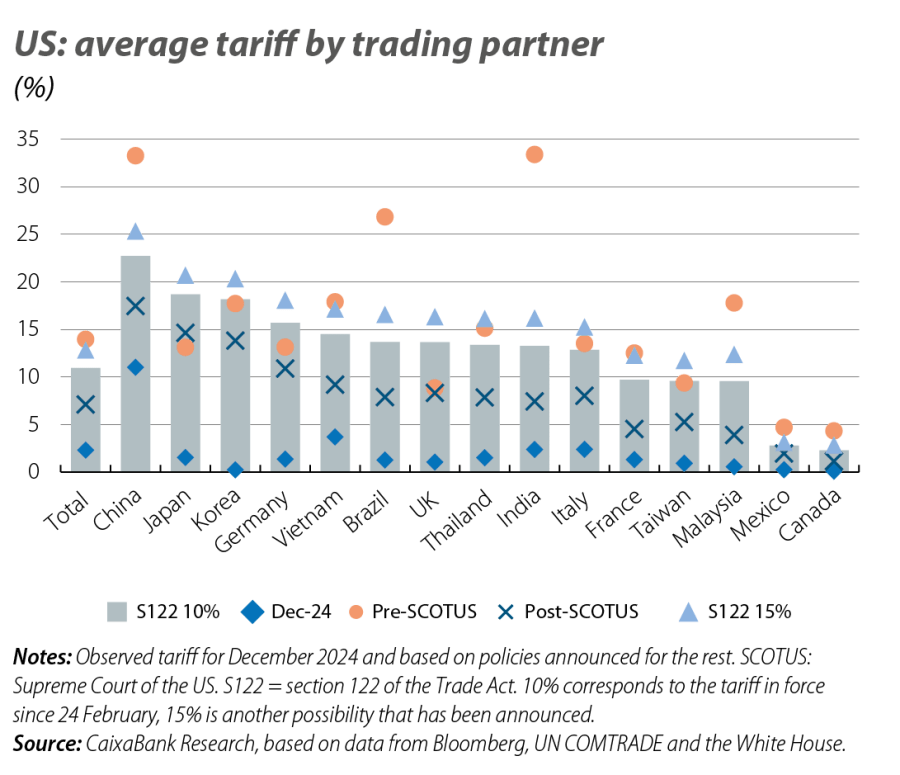

On the other hand, the US Supreme Court (SC) ruled in February that Trump exceeded the emergency powers invoked and has declared the tariffs imposed under the IEEPA illegal, but those approved under other regulations (on cars, steel, etc.) will remain in force. That is, the SC has declared the procedure used for the approval of the bilateral tariffs illegal, not the tariffs themselves. Trade uncertainty is now re-emerging as a period begins in which the Trump administration will explore all the legal avenues still available to continue implementing its tariff policy, which it has already made clear it will not abandon. In fact, Trump invoked Section 122 of the Trade Act to impose a universal 10% tariff, which has led to a «reconfiguration» of the tariff pressure. Countries such as China and Brazil will now have a much lower tariff than was in force prior to the Supreme Court's ruling, while the EU and the United Kingdom will lose out – so much so, that the EU has delayed the approval of the trade agreement reached in July of last year until there is more information and further clarity on this matter (see «10 questions about the US Supreme Court’s tariff ruling» in this same Monthly Report).

The shutdown affected the US economy more than expected in Q4

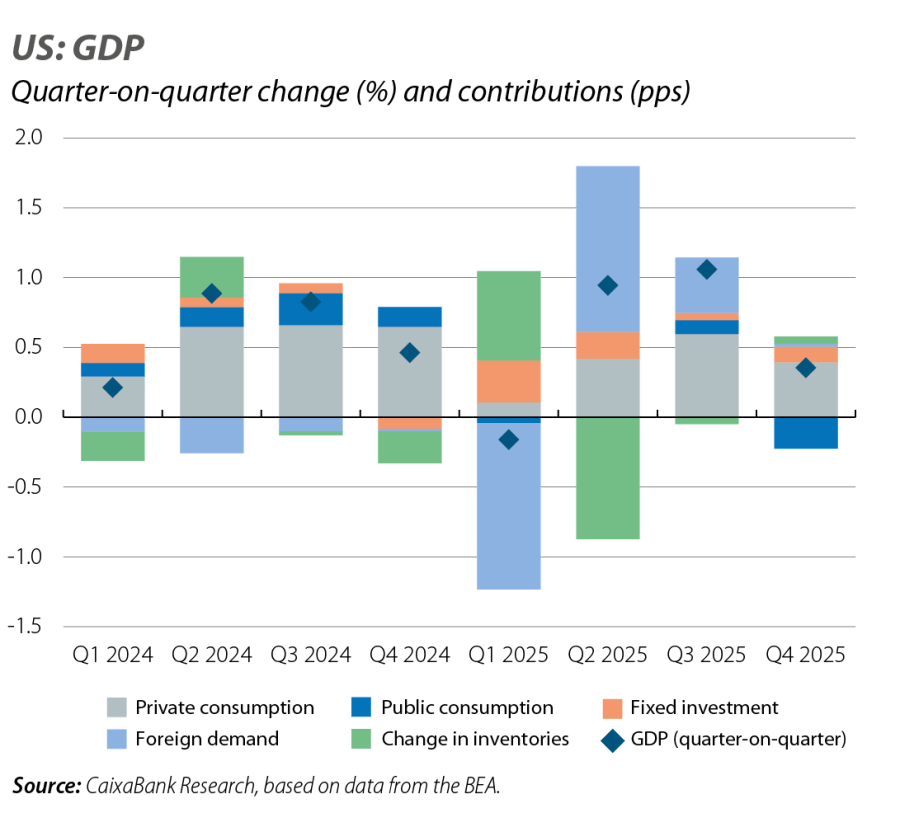

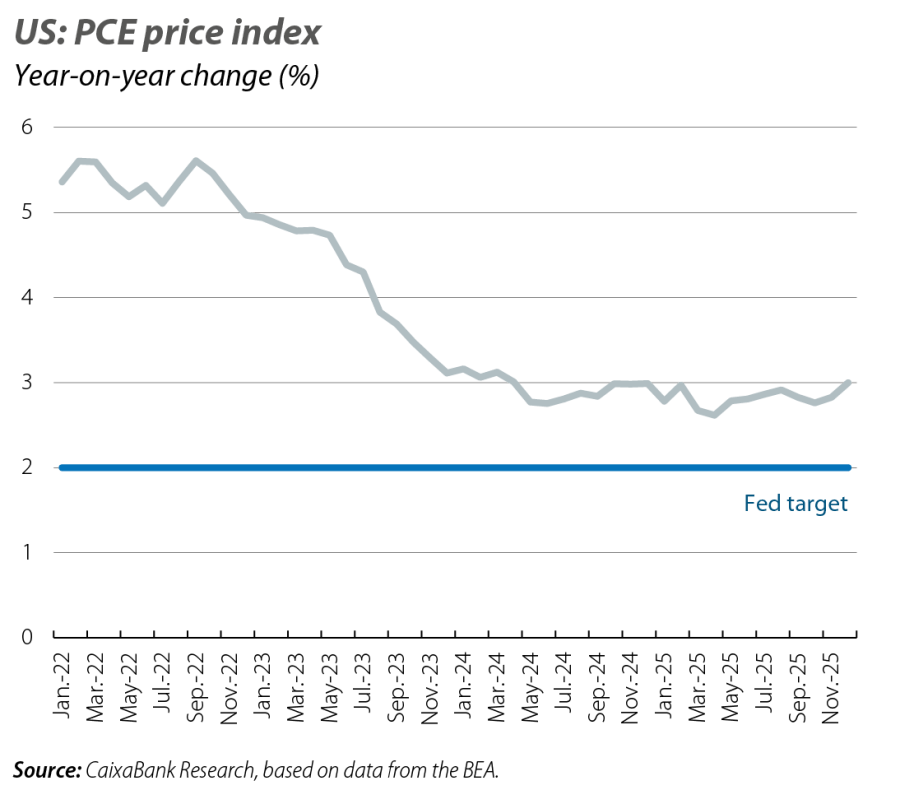

The Supreme Court's announcement regarding Trump's tariff policy added to the disappointment with the Q4 2025 GDP figure: growth reached 0.4% quarter-on-quarter (almost half of what was expected by the consensus of analysts), following 1.1% in Q3 2025, and placed growth for 2025 as a whole at 2.2% (2.8% in 2024). The result of Q4 is explained almost entirely by the decline in public spending (–1.3% quarter-on-quarter vs. 0.1% average for the year), as a consequence of the shutdown. In fact, the rest of domestic demand ended the year very dynamically: investment and private consumption grew at a quarter-on-quarter rate of 0.6%. Foreign demand, meanwhile, made an almost negligible contribution in Q4. However, the slowdown in Q4 appears to have been temporary and in Q1 2026 we may see a certain «rebound» effect, once activity in the federal government has returned to normal. In this regard, February's PMIs paint a picture of an economy that continues to perform well (51.9, following the Q4 average of 53.8, with 50 being the threshold denoting positive growth). Nonetheless, in February household confidence according to the Conference Board barely recovered from the substantial drop in the previous month (+2.2 points, to 91.2, with 100 being the threshold), while the University of Michigan’s indicator has yet to regain the levels of prior to «Liberation Day». This lack of household confidence is mainly due, among higher incomes, to volatility in the financial markets, and among lower incomes, to the loss of purchasing power they face. In fact, inflation is showing a clear resistance to falling to the Fed's target: according to the PCE price index, core inflation rose by 0.2 pps in December, reaching 3.0%, while January's CPI showed that overall inflation fell by 0.3 pps to 2.4%, but core inflation only decreased by 0.1 pp to 2.5%.

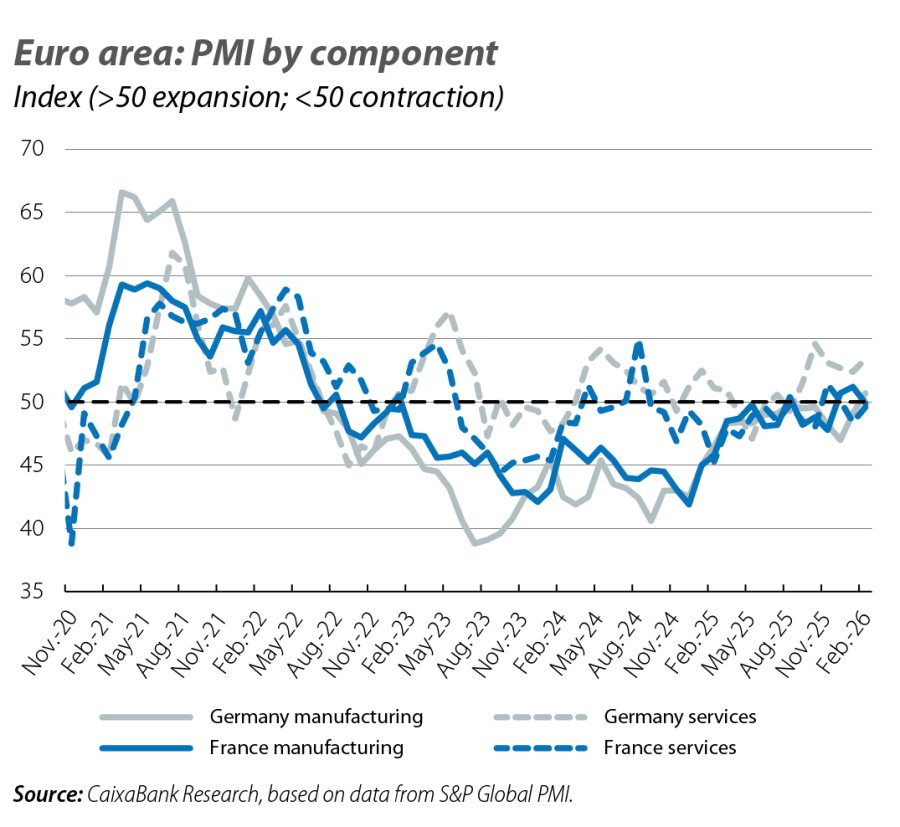

The performance of the euro area will largely depend on Germany

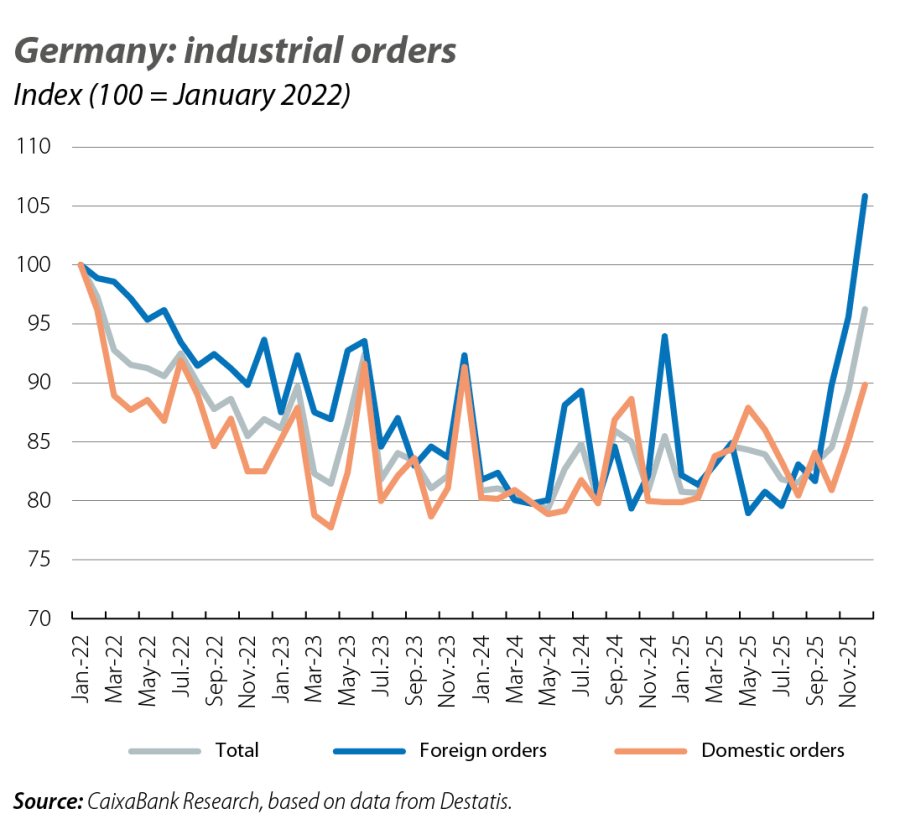

In fact, the PMI for the euro area rose by 0.6 points in February to 51.9, with activity in services continuing to grow, albeit at modest rates, and a manufacturing sector that is consolidating the positive shift initiated several months ago. This result is based on the recovery observed in Germany (+1.1 points, to 53.2) thanks to the continued momentum in the services sector and a manufacturing sector that is confirming a somewhat positive shift, albeit still with modest progress. Other opinion and business climate indicators contribute to this increased optimism towards the German economy, but with caution: in February, the ZEW shows that the percentage of respondents anticipating an improvement remains around 60%, while the Ifo increased, although it remains well below the threshold of 100 that denotes growth around the average rate (+1 point, to 88.6). Nonetheless, signs of recovery in the German economy are beginning to accumulate, particularly in the industrial sector: industrial orders grew by almost 13% year-on-year in December, anticipating a recovery in production in the coming months. France, for its part, seems to be confirming its position as the weakest link: the PMI remains below the 50-point threshold in February, due to weakness in both manufacturing and services, while consumer confidence remains weak and does not hint at any recovery in consumption in the short term. On balance, the euro area economy will continue to grow, albeit still below its long-term average, in a context in which inflationary pressures remain contained: in February, inflation rose by 0.2 pps, bringing the headline rate to 1.9% and the core index to 2.4%.

A rather apathetic close to 2025 in other parts of the world

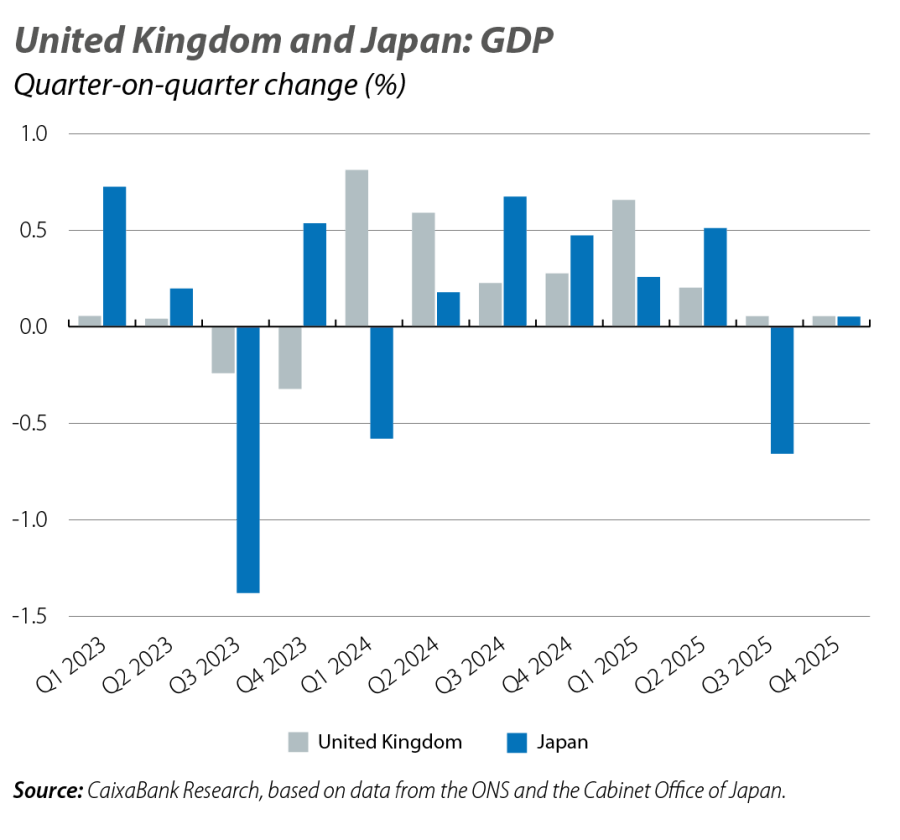

In the United Kingdom, GDP grew by 0.1% quarter-on-quarter in Q4 2025, confirming a steady slowdown over the course of the year that has led to a growth rate of 1.3% for 2025 overall (0.3% in 2024). The weakness observed in the main business and consumer surveys does not give us cause to anticipate any significant acceleration in activity in the short term. In Japan, growth in Q4 2025 barely reached 0.1% quarter-on-quarter, following the previous –0.7%, placing the 2025 average at 1.1% (–0.2% in 2024). Hopes for a revival of activity rest on the fiscal stimulus announced by the government, although the rise in sovereign interest rates may limit the effectiveness of fiscal and monetary policy in stimulating economic growth.