Geopolitics prevails over international economic data

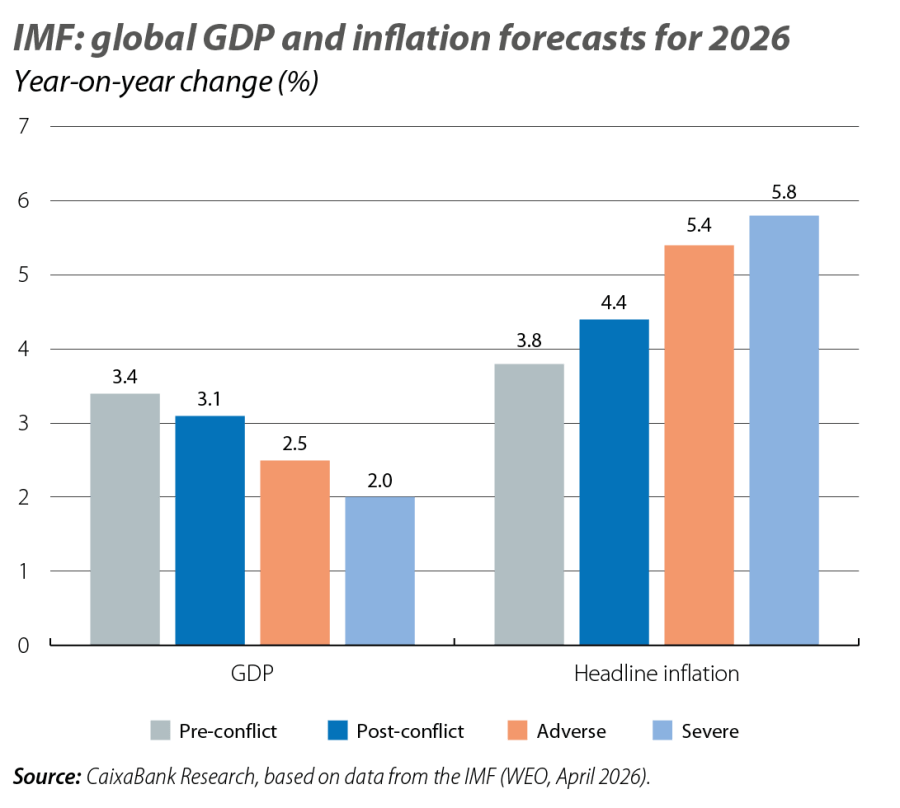

As of the close of this report, military and economic pressure continues around the Strait of Hormuz, a key route for the global supply of oil, gas, and derivative products. The IMF, in its April outlook report, points out that despite the strong start to 2026 globally, there is a risk of a severe energy shock if hostilities persist.

Attention in the past month has refocused on the Middle East

As of the close of this report, military and economic pressure continues around the Strait of Hormuz, a key route for the global supply of oil, gas, and derivative products. The IMF, in its April outlook report, points out that despite the strong start to 2026 globally, there is a risk of a severe energy shock if hostilities persist. In its baseline scenario, it assumes a relatively quick normalisation, with an average oil price of around 80 dollars per barrel in 2026, global GDP growth of around 3%, and an increase in inflation of 0.3 pps. It also warns, however, that more adverse or severe scenarios could push the global economy to the brink of stagflation.

The euro area was already in a rather delicate situation before the conflict

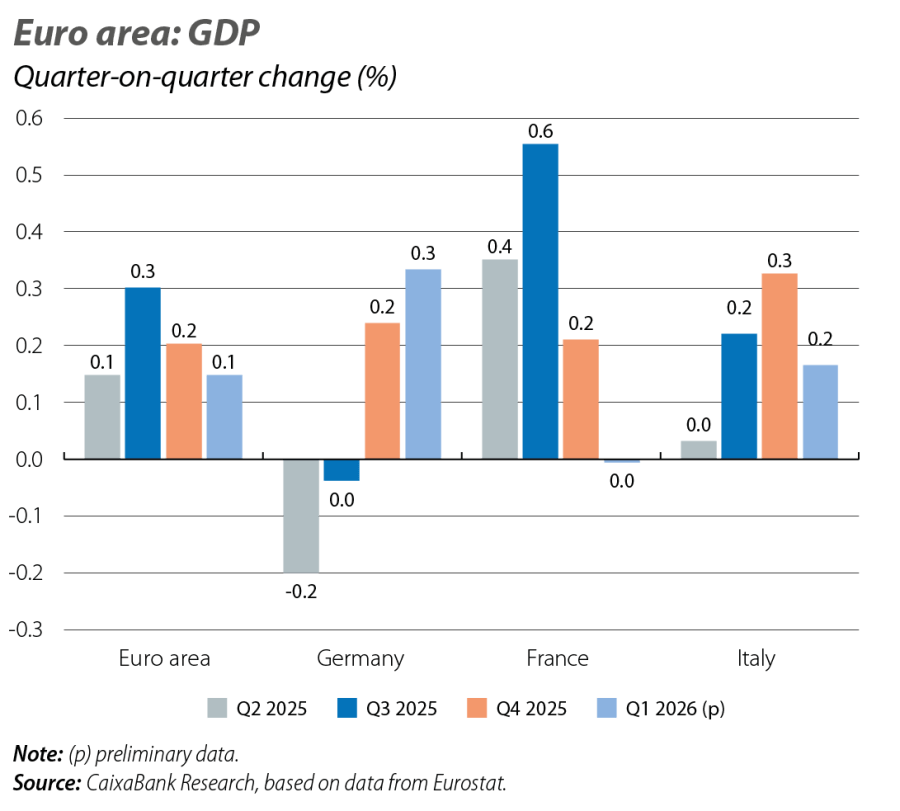

Euro area GDP moderated its growth in Q1 2026 to 0.1% quarter-on-quarter (previously 0.2%), but excluding Ireland it would stand at around 0.2% (previously 0.4%). By country, Germany grew by 0.3%, but important hard data for March (industrial production, orders, exports, etc.), which could affect the final GDP figure, are yet to be published. Italy grew by 0.2% and France stagnated. The euro area has had a modest start to the year, placing the region in a delicate position to face the new energy shock. Moreover, the latest indicators reveal an even weaker start to Q2 2026: in April, the PMIs (which reflect the business climate) fell into recession territory (–2.1 points, to 48.6, with 50 being the threshold) and the Commission's economic sentiment indicator recorded three consecutive months of decline, reaching its lowest level since November 2020 (93.0, with 100 being its historical average). To mitigate the impact of rising energy costs, the main euro area economies have opted for temporary and targeted measures (direct aid to vulnerable households or tax cuts), with a much lower fiscal cost than those deployed during the crisis of 2022-2023.

Germany will see how rising energy costs limit the impact of its infrastructure plan

Moreover, this plan is already struggling to take off: total cumulative federal spending to March has grown by almost 6.0% year-on-year, but infrastructure spending is still 14% lower than a year ago. Optimism about the German economy continues to cool: in April, the ZEW confirms a sharp rise in the proportion of surveyed investors who expect the situation to deteriorate further (almost 35 pps in two months, exceeding 38% of those surveyed), while the Ifo fell to its lowest level since June 2009 (84.4, with 100 being its historical average). Even the government has halved its growth forecast for 2026 to 0.5%.

Italy, which is more exposed to fossil fuels (as they generate almost half of the electricity it consumes), will feel the impact of rising energy prices more acutely in the middle months of the year. France, meanwhile, was already stagnant before the conflict and a substantial recovery is not expected (the consensus among analysts points to GDP growth of 0.1%-0.2% quarter-on-quarter going forward). Furthermore, the capacity of fiscal policy to support both economies is limited by the unfavourable state of their public accounts.

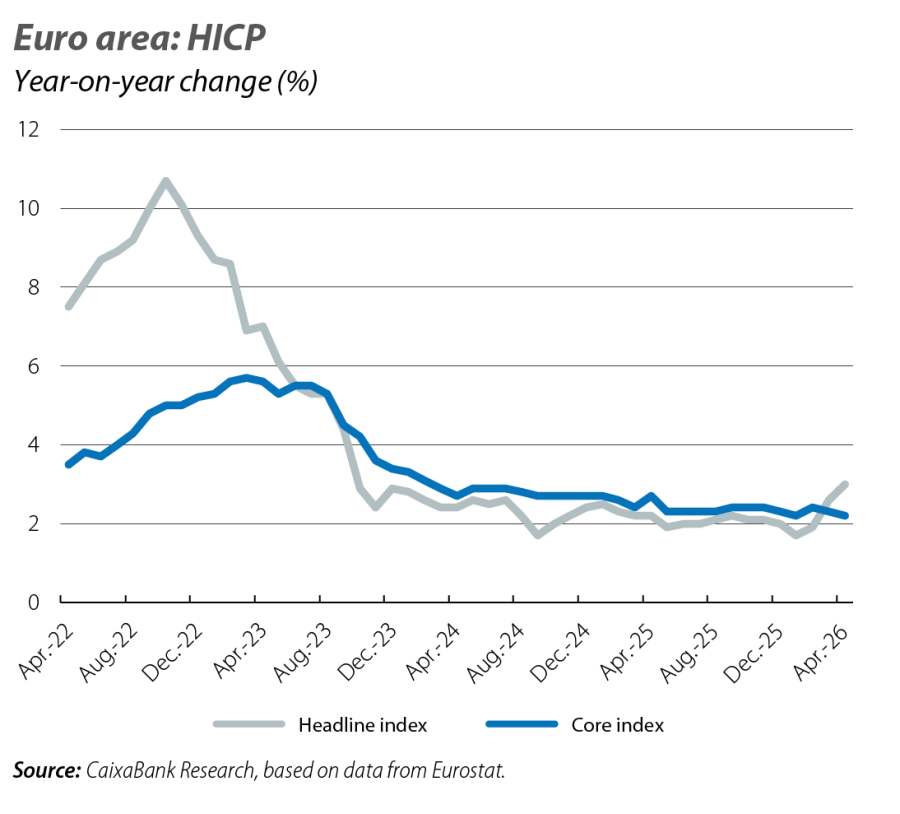

Euro area headline inflation rose by 0.4 pps in April to 3.0%

Euro area headline inflation rose by 0.4 pps in April to 3.0%, driven by energy (10.9% year-on-year in April vs. 5.1% in March), while core inflation fell by 0.1 pp to 2.2%. There is a risk of new inflation spikes: the price components of the PMIs have tightened since the conflict in the Middle East and the inflation expectations captured in the Commission's sentiment indicator are at their highest since the second half of 2022.

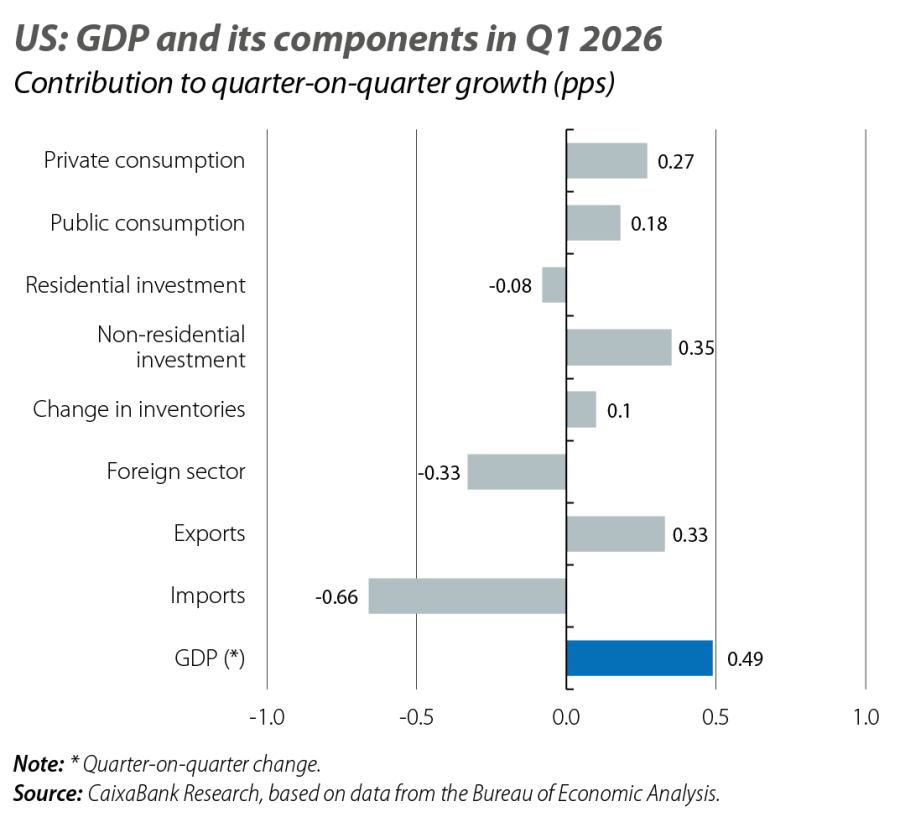

The US kicked off the year with good momentum, placing it in a better position to face the current energy shock

The US economy has overcome the impact of the shutdown: after the 0.1% quarter-on-quarter growth recorded in Q4 2025, it grew by 0.5% in Q1 2026. Private consumption continued to expand at a steady pace, while public spending experienced a rebound as its activity normalised (1.1% vs. –1.4%). The main driver was investment in fixed capital (1.5% vs. 0.4%), driven by the ongoing investments associated with AI: investment in computer equipment, software and research and development contributed almost 0.5 pps to quarter-on-quarter GDP growth. This AI boom is also driving imports (5.0% vs. –0.2%), which explains why external demand subtracted 0.3 pps from growth.

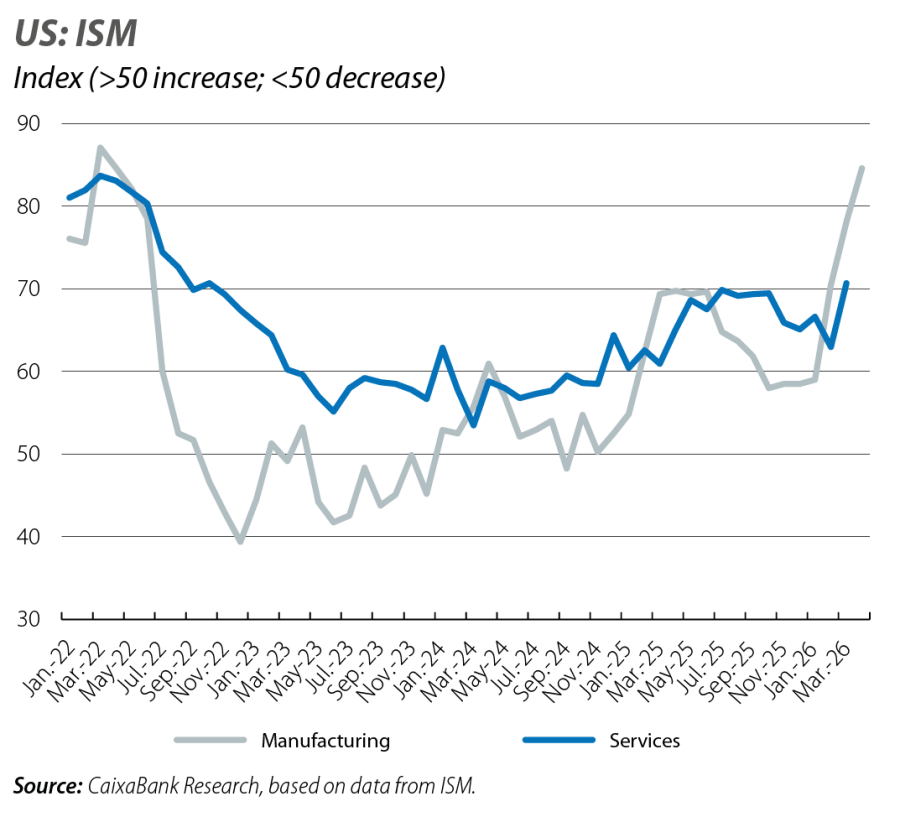

The latest business opinion and climate indicators suggest that this dynamism is set to continue, at least at the start of Q2. In April, the PMIs for both services and manufacturing improved and consolidated at levels compatible with growth rates similar to or slightly above those achieved in Q1. This message is reinforced by the ISM indicators, particularly in the manufacturing sector, which remains at its highest level since August 2022 thanks to the boost from orders.

This optimism in the business sector contrasts with the doubts among consumers

This optimism in the business sector contrasts with the doubts among consumers: the surge in fuel prices (petrol has risen by more than 33% in the year to April and exceeds 4 dollars per gallon, its highest since August 2022) and rising inflation have dented consumer confidence (the Michigan sentiment index fell in April to its lowest since the summer of 2022). In March, headline inflation rose by 0.8 pps to 3.3%, driven by energy (12.6% vs. 0.4%), while core inflation increased by 0.1 pp to 2.6%. The sharp increase in the price components of the main business climate indicators in March and April points to further rises in inflation in the coming months.

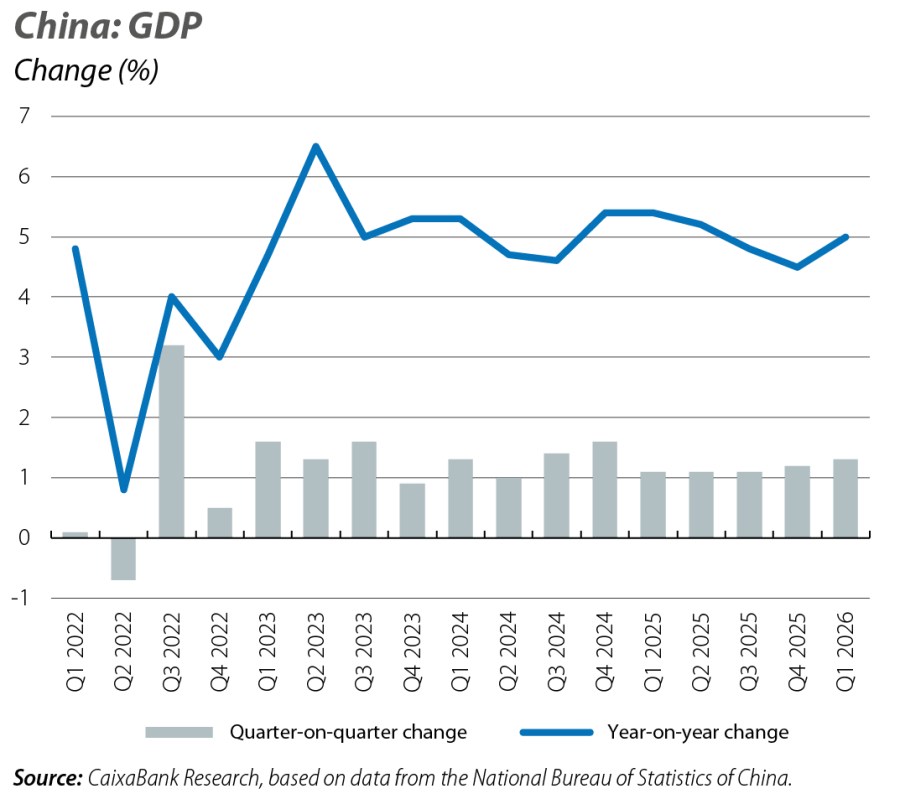

China kicks off the year on a good footing

GDP grew by 1.3% quarter-on-quarter in Q1 2026 (previously 1.2%) and by 5.0% year-on-year, slightly more than expected. Yet domestic demand remains fragile: consumption is slowing down and investment, despite overcoming the setbacks of 2025, remains at historically low levels, weighed down by the real estate sector. Industrial production and exports are showing solid growth, driven by high value-added products such as semiconductors and motor vehicles, which are expected to continue benefiting from the investment boom linked to AI. The positive performance of the main business climate indicators in April suggests that this economic momentum is being maintained at the start of Q2. In this context, inflation remains under control, thanks to a low starting point and measures taken to counteract the rising cost of energy: in March, the headline rate fell by 0.3 pps to 1.0%, and the core rate by 0.7 pps to 1.1%.