The shortage of new homes continues to strain Spain’s housing market

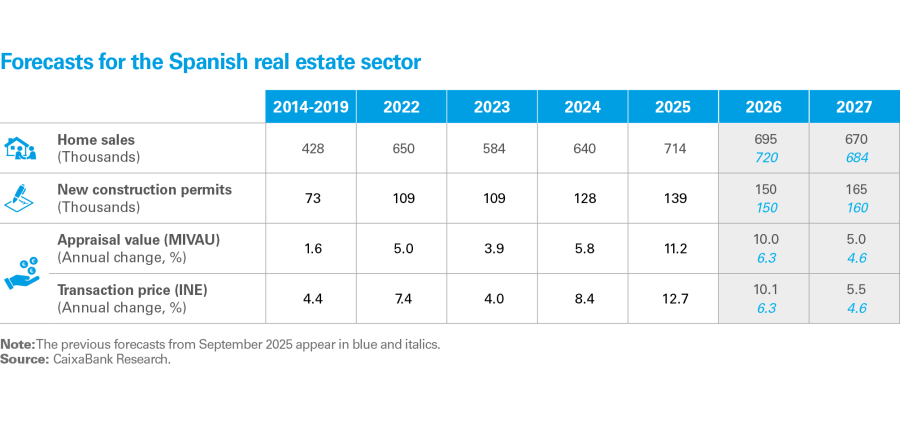

Spain’s housing market ended 2025 with exceptionally high levels of activity, exceeding 714,000 transactions, the highest figure since 2007. The strength of demand – driven by population growth, improved purchasing power and favourable financial conditions – sustained high activity, particularly in the first half of the year. However, on the supply side, significant limitations persist: despite the increase in permits, the construction of new homes remains insufficient to keep up with new household creation. This imbalance between supply and demand is exerting significant upward pressure on prices, which are accelerating across the board, particularly in the most dynamic and touristic areas. Looking ahead to 2026-2027, transactions are expected to stabilise at high levels and there will be a gradual improvement in supply, although it will remain insufficient. As such, prices will continue to rise, albeit at a more moderate rate.

A highly dynamic market with initial signs of stabilisation

The demand for housing in Spain remained very strong throughout last year and reached figures not seen since before the financial crisis. In 2025, 714,200 home sales were recorded, representing 11.5% growth and adding to the 9.7% increase registered in 2024. This considerable dynamism was supported by the confluence of several factors: stable and low interest rates, steady population growth (with around 500,000 additional inhabitants per year since 2021) and the recovery of real household disposable income in line with intense job creation. This combination of factors placed activity in 2025 at its highest level since 2007, reflecting particularly dynamic demand during the first half of the year, with year-on-year growth rates exceeding double digits.

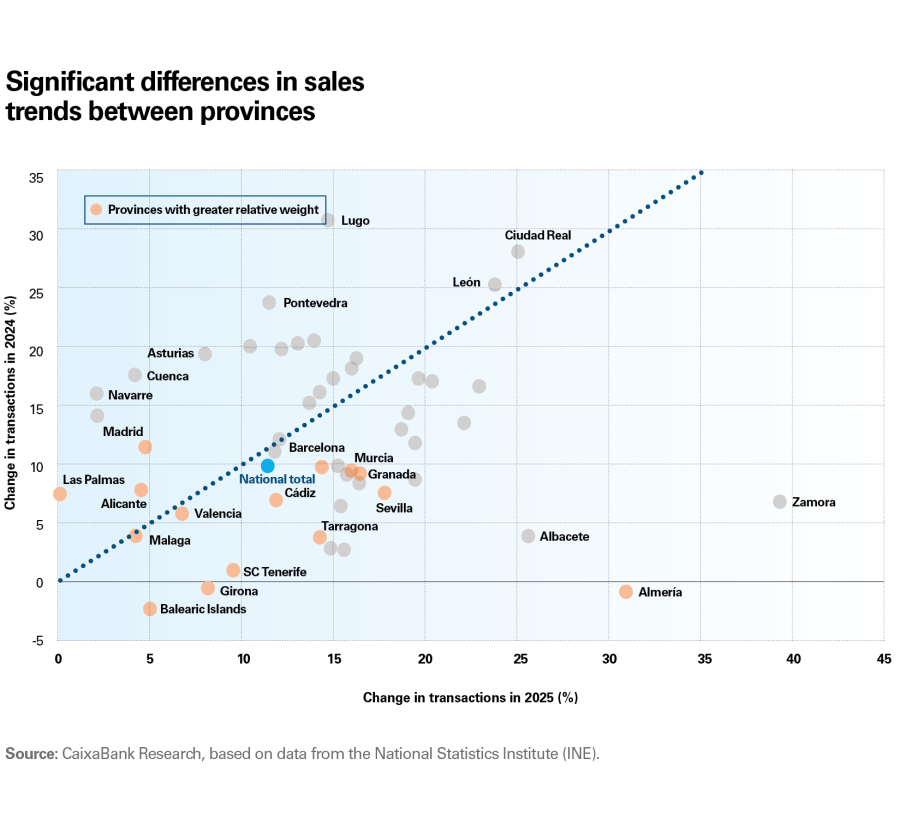

Sales transactions soared in 2025 but are beginning to show signs of stabilisation

Within this context of widespread strength, transactions exhibited more volatile behaviour and the growth rate lost momentum in the second half of the year. On the one hand, the so-called «step effect» meant that the comparison with the exceptional dynamism of the second half of 2024 was less favourable. On the other hand, the high prices are limiting households’ purchasing power and making housing less affordable for many. In turn, the shortage of product, especially in the new-build segment, is beginning to limit the completion of sales transactions.

At the provincial level, sales are showing a highly varied pattern across the country. In 2025, while in some areas transactions continued to accelerate (Ciudad Real, León, Lugo and Zamora), the major markets showed a gradual normalisation (Madrid, Barcelona, Valencia, Alicante, Malaga and Seville) and tourist areas showed greater disparity following the strong dynamism of 2024 (e.g. growth in Murcia and Cádiz contrasts with moderation in Las Palmas and Alicante).

By type of buyer, data from the Ministry of Housing and Urban Agenda show a gradual weakening of demand among non-resident foreigners, whose purchases have decreased significantly, subtracting more than 1 percentage point from the year-on-year growth in total sales over the last three quarters. As a proportion of the total, their relative weight has decreased from 7.9% in 2024 to 6.8% in 2025. There has also been a significant moderation among buyers of Spanish nationality, although the growth rate remains positive.

On the other hand, a change in the financing pattern can be seen: the proportion of home sales without a mortgage has decreased from 35% in 2024 to around 30% in 2025, indicating a decline in demand from buyers with greater financial capacity of their own, one of the pillars of the market’s dynamism in previous years.

Home sales by buyer’s residence and nationality

Supply fails to take off: bottlenecks and insufficient production in 2025

The shortage of the supply of new housing remains the single factor that is distorting the Spanish residential market the most, and with the available data from 2025 there is still no significant improvement that would suggest a substantial improvement in the short term.

Construction permits are far from meeting current demand and in 2025 they have even moderated slightly

In 2025, new construction permits for unsubsidised housing reached 136,000 units (the highest since 2008) and those for social housing, 23,200 (representing a 40% annual increase). Thus, the total number of permits increased by 6.9% (to 162,200), adding to the 25% advance recorded in 2024. However, net household creation reached 226,000 in 2025, so the housing deficit has continued to grow.

Additionally, a bottleneck is increasingly apparent in the project completion phase. In the trailing 12 months to September, only around 83,500 homes were completed, representing a very moderate increase of around 2% year-on-year, and clearly lower than the 7.6% recorded in 2024. The gap between permits and completed homes (see the following chart) has widened significantly and has now reached its highest levels since 2010, when the property development sector was still absorbing the excesses of the previous expansionary cycle. This widening of the gap points to growing obstacles in the construction process, delaying the delivery of developments underway. In fact, we are unlikely to see completed homes reach above 100,000 units during 2026. Factors such as labour shortages, supply delays, bottlenecks in electrical infrastructure, and the high regulatory burden are contributing to this growing mismatch. To analyse this deficit of new housing in greater depth – including its territorial distribution, the various supply scenarios, and the factors contributing to the construction bottlenecks – we include in this same report the article «Lack of new housing where it is most needed: a growing and geographically concentrated deficit».

While there is broad consensus between the development sector and the general government on the urgent need to increase the housing supply, supply measures are slow to materialise and their effects will be gradual as they depend on execution capacity and the unlocking of land. To accelerate the short-term supply response, it is crucial to decisively streamline the permit and urban planning processes, as well as to kick-start activity on public land that is already available.

The delay in completed homes points to increasingly significant bottlenecks

Prices are accelerating, with highly uneven behaviour between regions

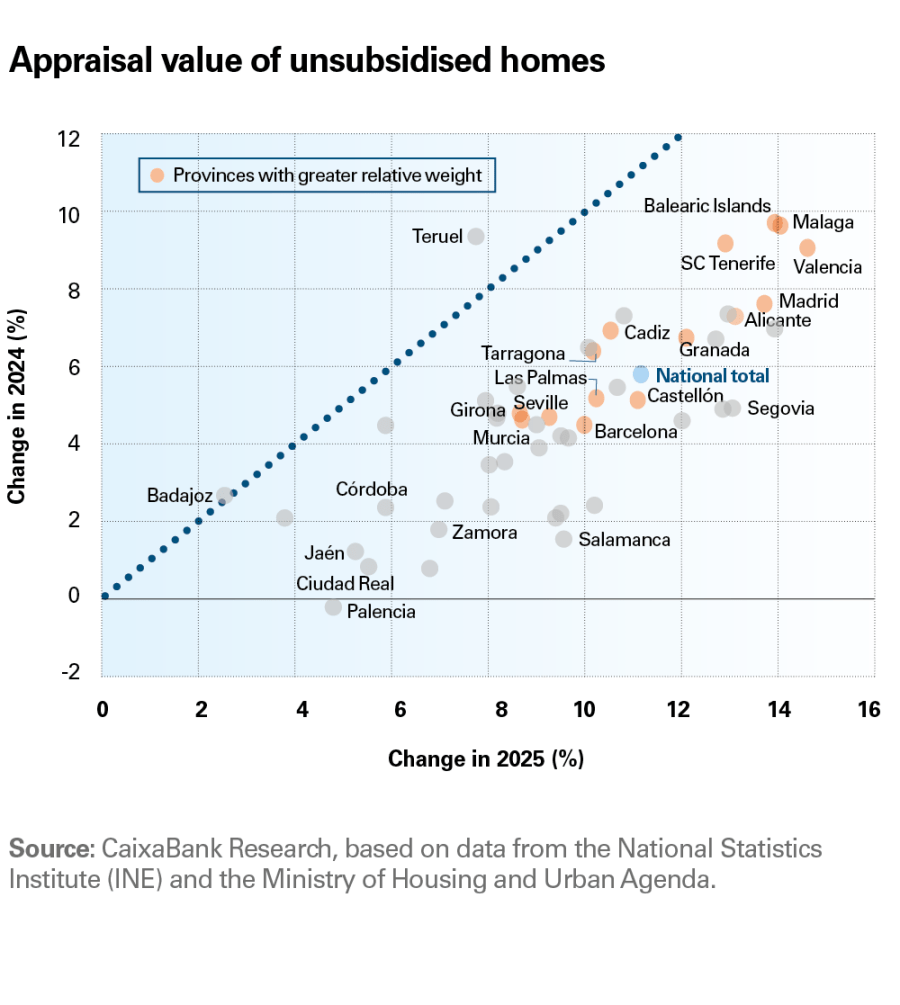

The intensification of the imbalance between supply and demand continues to exert upward pressure on house prices. In Q4 2025, the National Statistics Institute’s transaction price index recorded an annual increase of 12.9% (versus 11.3% in Q4 2024), while the appraisal value of unsubsidised housing rose at a rate of 13.1% in Q4 2025 (up from 7.0% in Q4 2024).

Although prices have accelerated in all regions, the pattern is highly varied, and it is possible to distinguish two large groups of provinces according to the rate of price growth. On the one hand, the most tourist-oriented provinces and the country’s main economic hubs – the Balearic Islands, Malaga, Santa Cruz de Tenerife, Valencia, Alicante, and Madrid, among others – recorded double-digit growth rates in both 2024 and 2025. At the opposite end of the spectrum, there is a second group of inland provinces with much more moderate price growth and where, in some cases, decreases were even observed in 2024. This is the case for Ciudad Real, Palencia, Orense, Jaén and Zamora.

House prices continue to grow rapidly and unevenly between regions

The intensification of the imbalance between supply and demand continues to exert upward pressure on house prices

We update our forecasts for Spain’s housing market

On the demand side, the factors that have been sustaining it over the past two years continue to show a robust tone: a favourable business cycle, with a solid labour market; high population growth driven by migratory flows; low interest rates, and a still relatively high savings rate, which gives some households financial leeway. However, the deterioration of housing affordability, especially in the major cities, could limit the realisation of some of the demand and encourage a shift towards metropolitan outskirts. In this context, in 2026-2027, sales could remain high, albeit slightly below the peaks of 2025 (see the table below).

On the supply side, the scenario assumes a gradual easing of the current bottlenecks and a moderate increase in new housing development. However, this will probably still be insufficient to cover the formation of new households.

Overall, house prices are expected to continue to grow in 2026-2027, albeit at slightly more moderate rates than in 2025, with significant territorial disparity: bigger increases in provinces where demand has so far been more restrained, and more moderate advances in the more dynamic markets, where signs of exhaustion are already evident.

House prices will continue to grow in 2026‑2027, albeit at slightly more moderate rates than in 2025

These forecasts may be affected by the outbreak of the war between the US and Israel and Iran. Although the impact will depend on the duration of – and the degree of disruption caused by – the conflict, a priori the risks are concentrated in the increase in construction costs and a possible deterioration in financial conditions and confidence. The rise in energy costs can be expected to push up the prices of energy-intensive materials – such as cement, ceramics and steel – in a sector already facing cost pressures. This could be compounded by a tightening of financial conditions if greater geopolitical uncertainty raises risk premiums or if inflationary pressures force the ECB to raise interest rates, making financing more expensive for developers and buyers. Finally, a potential deterioration in household and business confidence, although not the central scenario, could delay investment decisions and moderate housing demand.