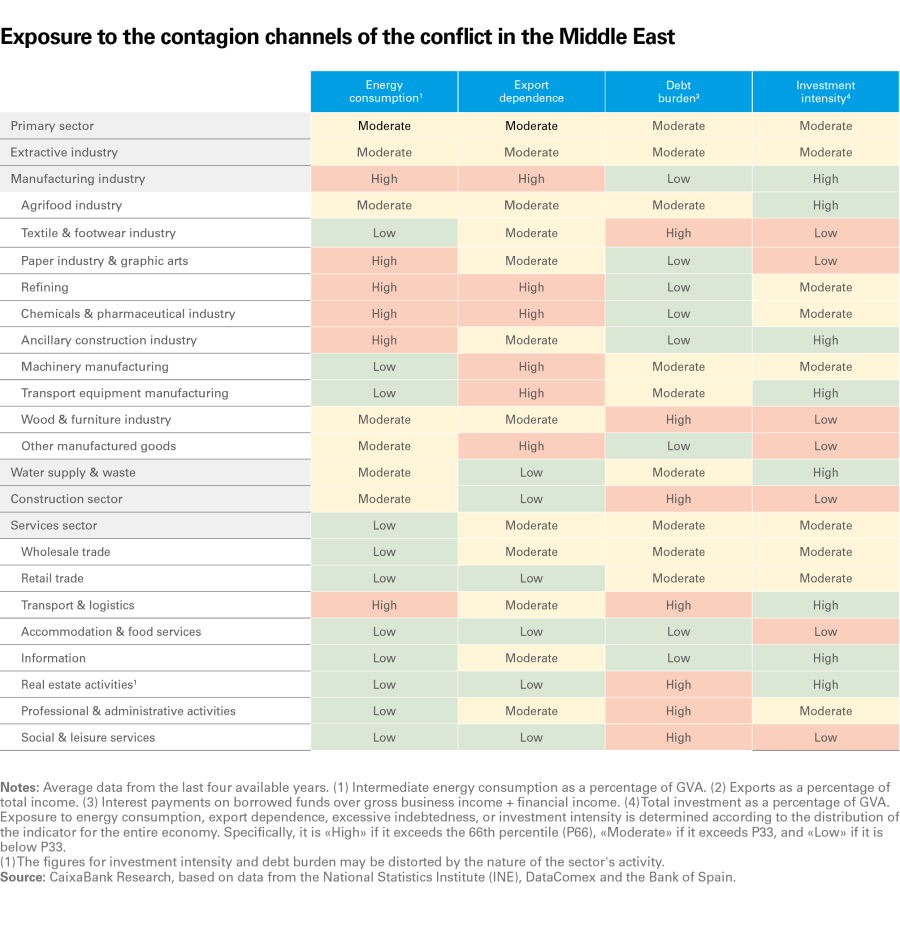

The energy shock amplifies sectoral differences

The Spanish economy is facing 2026 from a strong starting position, supported by the momentum of buoyant growth in 2025, a dynamic labour market, strong domestic demand and relatively contained inflation despite the energy shock. The outbreak of the war in Iran has introduced a new supply shock, increasing uncertainty and forcing us to revise downwards the projected GDP growth for this year to 2.1%, 0.3 pps below the previous forecast. In any case, the intensity of the slowdown is expected to vary depending on the sector. Manufacturing sectors, which are more energy-intensive, outward-facing, and with a weaker cyclical position, will be the most affected. In contrast, services and other activities linked to domestic demand are starting from a more solid position and are less exposed.

The strength of the Spanish economy before the conflict in the Middle East

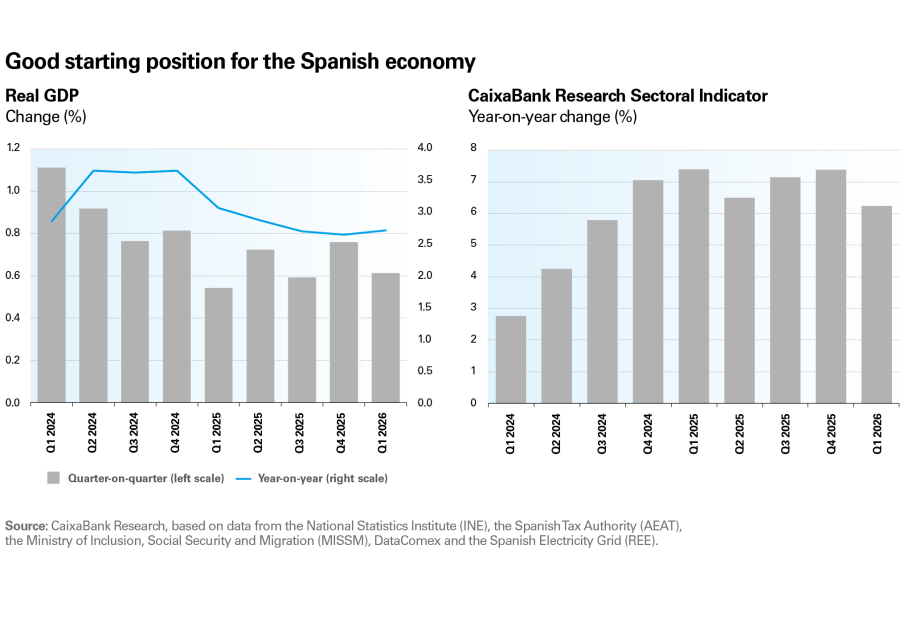

The economy kicked off 2026 supported by favourable momentum following the strong performance of the previous year, in which GDP grew by around 2.8%, well above the euro area average. The initial data available for the year indicate that economic activity remains in expansionary territory. In Q1, GDP grew by 2.7% year-on-year, driven mainly by domestic demand. The labour market also continues to perform well and consumption indicators reflect a broadly dynamic tone, albeit with a slight loss of intensity in Q2 of the year. The CaixaBank Research Sectoral Indicator also reflects a slight loss of momentum and suggests that the peak of the cycle may have passed by the end of 2025.

In fact, the sectoral breakdown shows a decrease in the number of sectors growing above their potential, while a larger proportion are now advancing at a rate close to their historical average.

The percentage of sectors growing above their long-term average has decreased significantly: after being at 77% in 2025, it has fallen to 27% in 2026.1 This decline reflects that the dynamism is no longer as widespread and is now concentrated in a smaller group of sectors: the extractive industry, water supply, construction, real estate activities, and professional and administrative activities are showing the most dynamic growth.

The Sectoral Heat Map indicates an increase in the proportion of activities that are in a position of weakness (35% of sectors in the opening months of the year), meaning they continue to grow but at a rate below their historical average. The economy is thus shifting from a phase with broad-based growth to one in which it is more mixed: some sectors continue to expand, but others are cooling due to the shock in energy prices.

- 1

We consider a sector to be growing above its long-term average when the Sectoral Indicator for that sector exceeds the 50th percentile of its growth distribution since 2010.

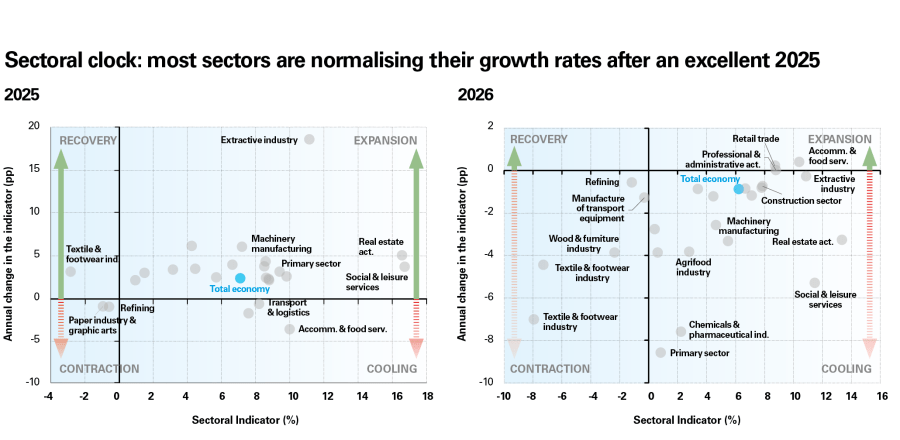

Normalisation of the sectoral cycle following the rapid growth of 2025

The Sectoral Clock helps to outline – and provide greater insight into – the latest developments in each sector.

Compared to 2025, in 2026 there is a clear shift of sectors towards the «cooling» quadrant. A certain moderation in growth was already anticipated for this year, but the energy shock will likely accelerate this process in some sectors more than initially expected. In any case, the Sectoral Indicator remains, overall, at levels compatible with a positive growth rate.

The manufacturing sectors are slowing down, with a more pronounced deterioration in the paper, textile and wood industries

If we analyse the trends by major sector groups, several patterns emerge. Firstly, several manufacturing sectors are slowing down and approaching stagnation: these include the chemicals, ancillary construction, and agrifood industries, among others. In any case, the sectors that continue to perform the worst are paper, textiles and wood, which show a negative indicator and a deterioration compared to 2025.

Secondly, the industrial sectors most closely linked to investment are in an intermediate position, with a weaker tone compared to previous years, but still holding up despite the challenging international context. Specifically, sectors such as the extractive industry and machinery manufacturing remain in a high activity zone, but with a significant moderation in their growth rate.

Construction, trade and professional services, more closely linked to domestic demand, continue to show greater resilience

Meanwhile, construction, trade, and professional services remain on the right side of the chart, with high activity levels, indicating that the group of sectors more closely linked to domestic demand continue to show significant resilience.

The performance of consumer services reveals a particularly mixed pattern. Activities such as hospitality and retail trade are holding up relatively well compared to industry, but other sectors (such as social services and leisure or real estate activities) show a loss of momentum. In any case, all of them remain highly buoyant and are among the most dynamic sectors in the Spanish economy.

Sectoral outlook: the Middle East conflict widens divergences

In the current context, energy prices are one of the key factors that will determine the pace at which the economy will be able to grow. In the new forecast scenario, we take as a reference the prices quoted in futures markets in recent weeks. Specifically, we assume an average price for this year of 90 dollars/barrel for oil and of 43.4 euros for gas. Both figures are above the benchmarks used in the previous forecast scenario, of 67 dollars and 31 euros, respectively. The new path of energy prices is consistent with a scenario in which they remain relatively strained, but where the conflict is relatively short-lived and ultimately favouring a gradual easing over the coming quarters.

In this context, the Spanish economy would lose some momentum but would nevertheless maintain a reasonably strong growth rate in 2026-2027. Specifically, following the GDP growth of 2.8% in 2025, the new forecast scenario anticipates a gradual slowdown to 2.1% in 2026 and 1.8% in 2027. Although this is a more moderate growth profile, it remains above that expected for the euro area as a whole. The strong starting position – with dynamic domestic demand, an expanding labour market and a sound financial situation – bolsters the economy’s ability to absorb the energy shock and reduces the likelihood of abrupt macroeconomic adjustments.

The rise in inflation that would occur in this context would be noticeable but moderate. Taking into account the measures announced by the government to date, the new scenario envisages a rise in the average inflation rate this year to 3.5%, while in 2027 it should gradually moderate to levels below 3%. The rise in inflation in the euro area would be of a similar magnitude and would compel the ECB to raise interest rates slightly to 2.5%.

At the sectoral level, we expect the differentiation that is already beginning to be observed in some indicators to consolidate in the coming quarters. The sectors where we expect to see a sharper slowdown are those that are more energy intensive. Depending on how the war in the Middle East develops, sectors more open to foreign trade or those more sensitive to changes in financial conditions could also be affected. In this context, the manufacturing industry bears the brunt of the risk, while activities more tied to the domestic market or with lower energy intensity – such as many services – have a more limited exposure.

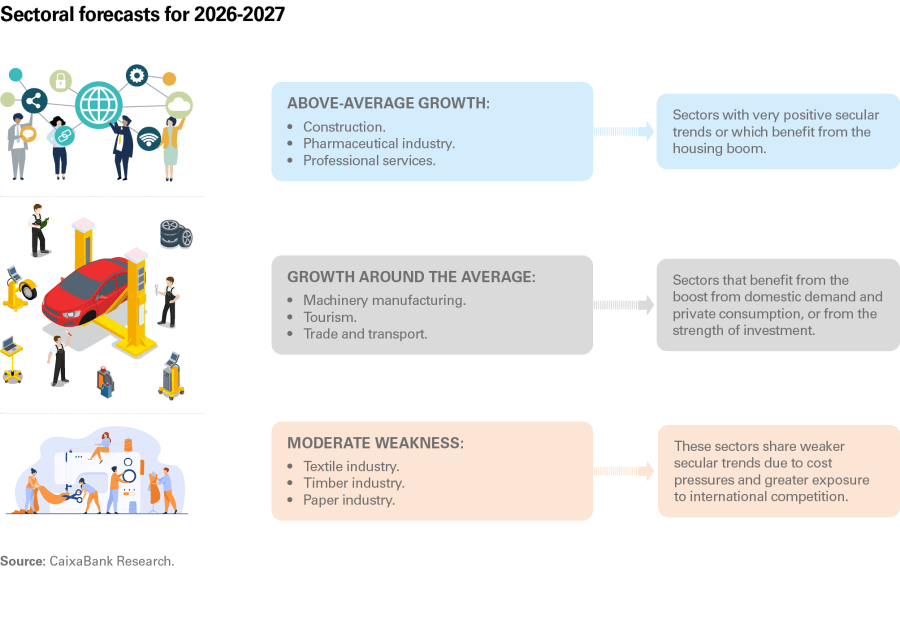

Specifically, for the period 2026-2027, a sectoral map with three distinct blocks is emerging:

Sectors with above-average growth:

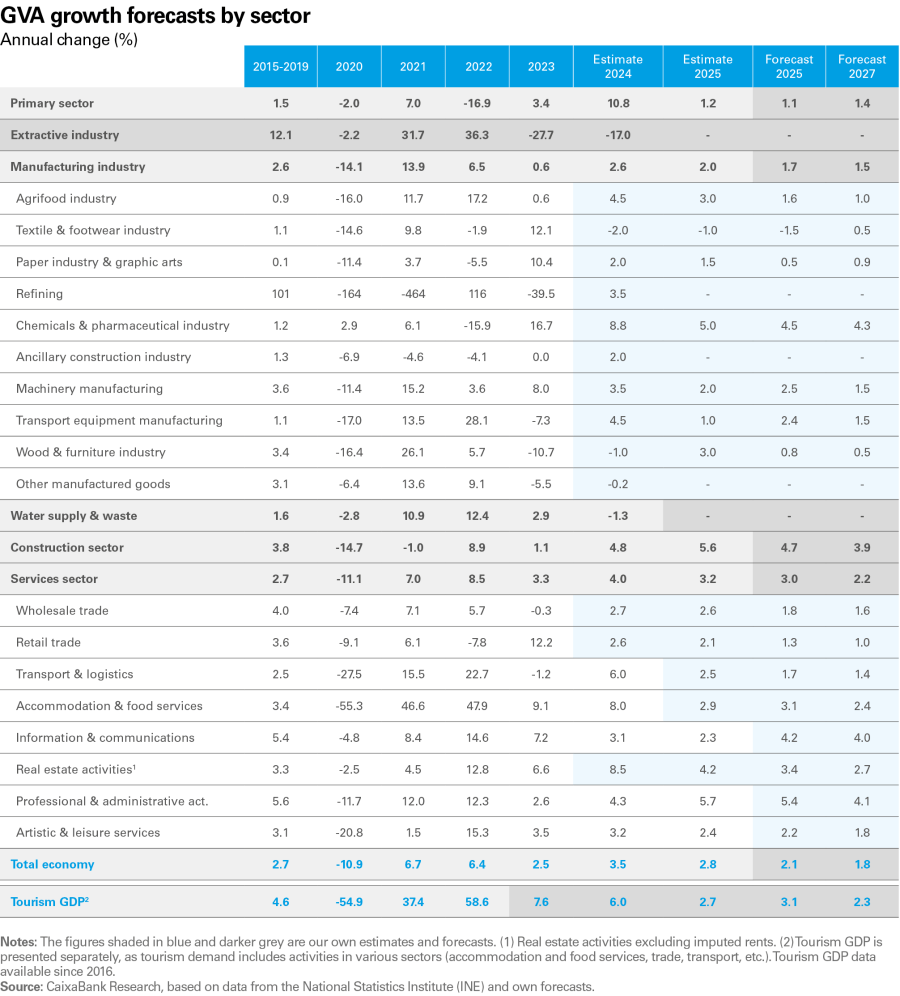

Construction: after recording an excellent growth rate of 5.6% in 2025, the sector is expected to maintain a high growth rate, albeit slightly lower than previously, thanks to strong housing demand. Although the construction sector is highly sensitive to financial conditions and energy prices, a combination of favourable momentum, the current investment cycle and strong housing demand are expected to drive the sector as a whole. Growth is thus forecast to reach 4.7% in 2026 and 3.9% in 2027, keeping it among the most dynamic sectors in the Spanish economy.

Professional and administrative services: after advancing by 5.7% in 2025, the sector is expected to remain highly dynamic (+5.4% in 2026 and +4.1% in 2027). This growth is supported by both a cyclical component – linked to business investment – and a very favourable secular trend (growing demand for specialised services and outsourcing) that will push its expansion well above the economy’s average.

Information and communications technology (ICT): the sector has outpaced the economy as a whole in the last decade and, in a context marked by digital transformation and increasing use of artificial intelligence, it will continue to act as a growth driver. Its lower energy intensity places it in a favourable position to demonstrate resilience in 2026-2027, with projected growth rates of 4.2% in 2026 and 4.0% in 2027.

Pharmaceutical industry: it will continue to be one of the fastest-growing industrial pillars. Its high capacity for innovation, international projection and skilled employment position it as a strategic sector for the economy.

Sectors with growth around the average:

Tourism and hospitality: after consolidating its post-pandemic normalisation in 2025 (+2.7% growth in tourism GDP), the sector’s performance in 2026-2027 will largely depend on developments in the conflict in Iran. Historically, episodes of geopolitical instability have benefited tourism in destinations perceived as safe (redirecting travellers), although this positive effect could be offset if the conflict in the Middle East becomes entrenched and ultimately leads to a further surge in energy prices. In the baseline forecast scenario, the redirection of flows would outweigh the slight erosion of income caused by the rise in inflation, leading to a gentle acceleration of tourism to +3.1% in 2026 and +2.3% in 2027, maintaining its central role in the Spanish economy.

Trade: it is expected to continue expanding in line with private consumption. However, the uptick in inflation associated with rising energy costs will put pressure on real incomes and will moderate growth rates. The competition in e-commerce and the need for digital transformation represent additional structural challenges. Even so, the forecast indicates positive growth exceeding 1% annually in both segments during 2026 and 2027.

Manufacturing industry: we expect it to continue growing, albeit at a more moderate pace, with an increase of +1.7% in 2026 and +1.5% in 2027. These rates are higher than the historical growth of Spain’s industry (around 0.6% annually) and that of its European counterparts. Spain enjoys a competitive energy advantage over other countries (less dependence on Russian gas and a greater share of low-cost renewables), which has enabled its industry to better withstand energy shocks. However, the sector’s high sensitivity to oil and gas prices, along with the gradual erosion of this advantage – for example, through subsidies in competing countries that reduce energy costs for their energy-intensive industries – will cause Spain’s manufacturing to slow down relative to 2025.

Sectors with weaker growth:

Despite the solid forecast scenario overall, certain sectors are expected to lag behind with below-average performance:

Certain traditional manufacturing sectors face structural headwinds (strong global competition from emerging economies, shifts in demand) which will limit their growth. This is the case for the textile, wood and furniture, and paper industries, which are also relatively vulnerable to rising energy costs. In these sectors, the shock in input costs could accelerate adjustment processes that are already underway after years of competitive pressure, possibly resulting in zero or very modest growth over the coming two years.

Primary sector: after advancing by a modest +1.2% in 2025, it is expected to grow by around 1.1% in 2026 and to rebound slightly to +1.4% in 2027. These are low rates, influenced by structural limitations (climate change, rural depopulation, etc.) and by rising energy and fertiliser costs.