How are Spain’s economic sectors exposed to the Iran war shock?

After a 2025 marked by uncertainty around trade policy, in 2026, the conflict in Iran has emerged as the main source of risk for the global economy. We analyse the exposure channels of Spain’s various economic sectors to this shock. We focus on four transmission channels: the rising cost of fossil fuels, global trade tensions, direct supply risks stemming from the blockade of the Strait of Hormuz, and the potential tightening of financial conditions.

Fossil fuel prices

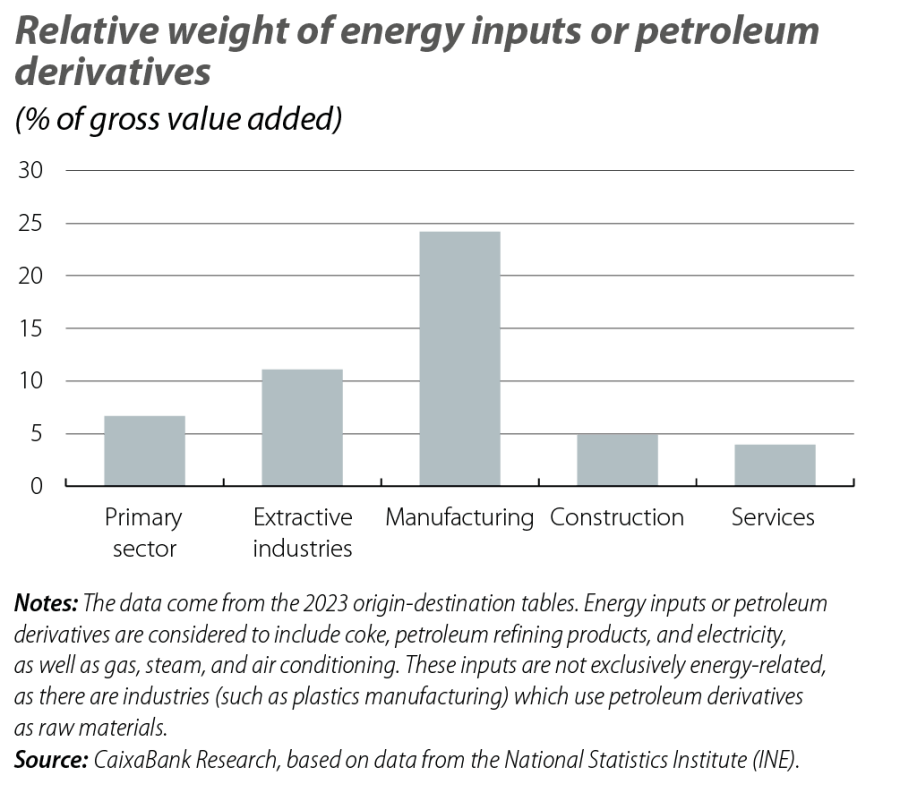

The most significant factor is the rising cost of fossil fuel inputs, particularly oil and gas.

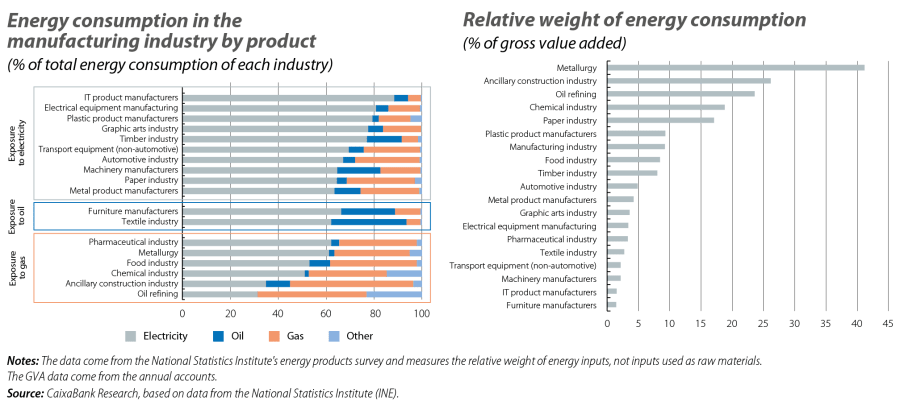

The exposure varies widely by sector. Manufacturing is the most vulnerable sector: it combines high energy intensity with extensive use of petroleum derivatives as intermediate inputs. This is particularly relevant in sectors such as refining, plastics, and parts of the ancillary construction industry, where energy is not only an operational cost but also a raw material.

Although in recent years the industry has electrified and has reduced its reliance on fossil fuels, there are activities, such as the chemical industry, that directly depend on oil or gas as raw materials, or which require high-temperature industrial heat, and therefore continue to face significant cost increases. Other industries, such as the paper industry, have a high energy consumption relative to their value added.

Although construction and the primary sector have less direct exposure to fossil fuel inputs, they remain sensitive to a price shock through indirect channels. In both cases, a significant portion of their costs come from intermediate goods that are highly energy-intensive. In construction, the ancillary industry is particularly intensive, and its inputs accounted for 18.8% of the sector’s value added in 2023. In the agricultural sector, indirect exposure is concentrated in fertilisers and other chemical products whose production largely depends on gas and other energy inputs; these accounted for 10.0% of the sector’s value added in 2023. Consequently, both sectors are vulnerable to the pass-through of higher energy costs along their supply chains.

Services, on the other hand, have a more limited aggregate exposure due to their lower energy intensity. The main exception is transport, where the cost structure still heavily relies on fuels. Some services related to tourism, distribution and logistics could also be affected, as they absorb higher mobility and supply costs.

Global trade

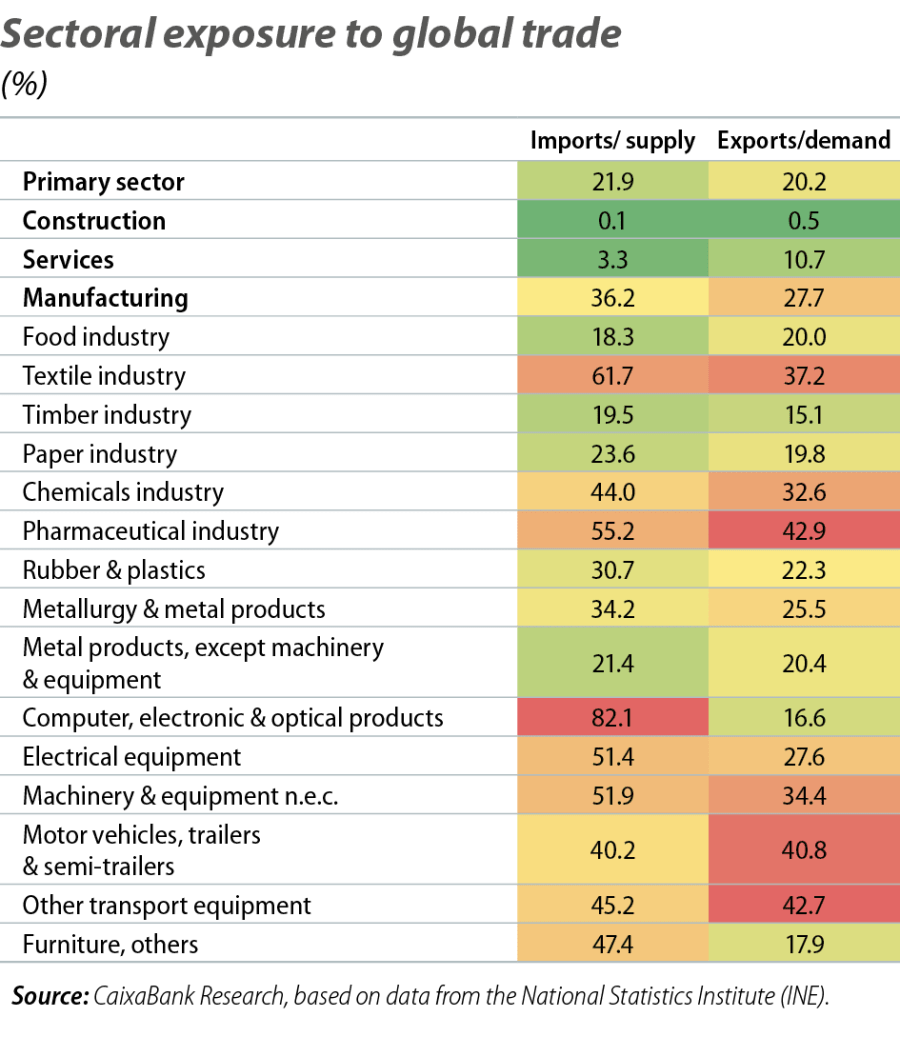

The complexity of the geopolitical environment introduces risks to global trade on both the demand and supply sides. On the demand side, weaker global growth and its uneven impact across markets increase the vulnerability of more export-oriented sectors. On the supply side, while we do not anticipate a widespread disruption of global value chains comparable to that seen after the pandemic, certain value chains could come under strain.

Exposure to international markets is particularly high in manufacturing. The sector imports the equivalent of 36.2% of the value of its supply, while exports account for 27.7% of its final demand. Within the manufacturing industry, sectors such as pharmaceuticals, machinery, and motor vehicles stand out due to their greater exposure to global trade, given their integration into complex, international supply chains.

Services, in aggregate, are less exposed to international trade, in terms of both supply and demand. However, the degree of exposure varies widely, particularly in terms of demand. Sectors linked to tourism, such as transport, remain heavily dependent on foreign demand. Similarly, some high-productivity services have a clear international focus: programming and consultancy, for example, show an export dependency of 28.9%, while professional, scientific and technical services have an exposure of 16.4%.

This pattern is relevant because the most productive sectors also tend to be the most internationally-oriented. Therefore, a slowdown in global trade or a more intense fragmentation of value chains would not only impact growth through reduced exports but could also have implications for productivity.

Imports affected by the closure of the Strait of Hormuz

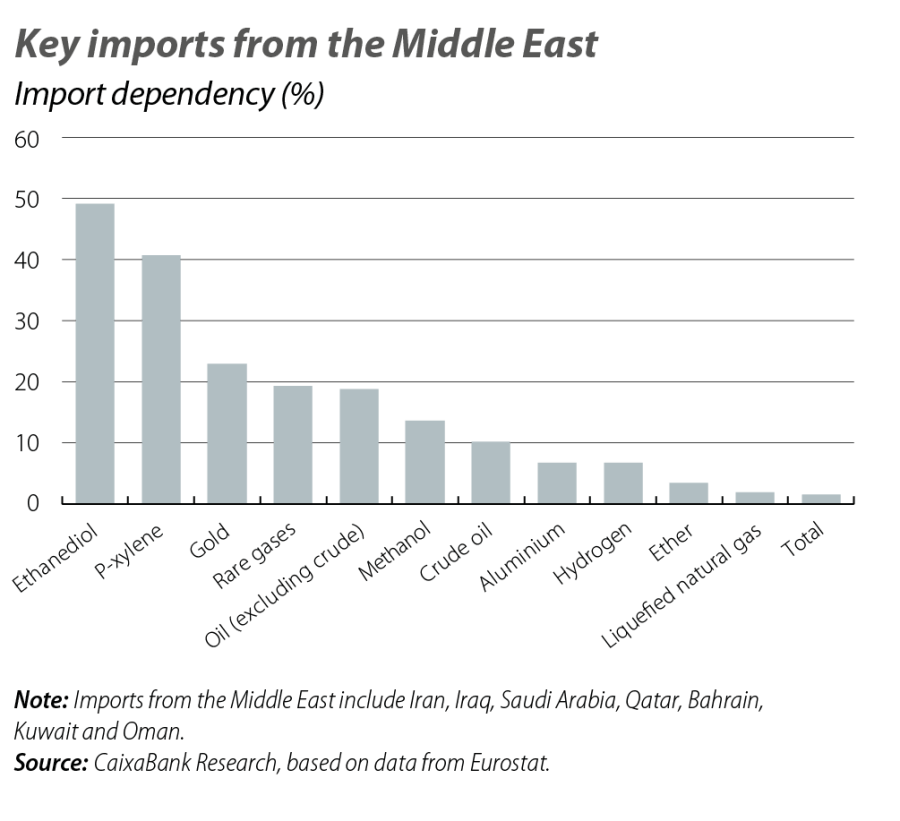

In aggregate terms, the Spanish economy’s direct exposure to the region is limited: only 1.6% of all Spanish imports come from countries affected by the closure of the Strait of Hormuz. However, this exposure is concentrated in a narrow set of sectors such as in energy products and certain chemical inputs, which could lead to disruptions at the sector level.

The degree of energy dependence is moderate. In 2025, 10.1% of the crude oil and 18.9% of the refined products imported by Spain came from Gulf countries. In the case of liquefied natural gas, the exposure was much lower, at around 2%. Together, these three products accounted for 67.8% of Spain’s total imports from the region.

Beyond energy, there are intermediate materials with a much higher relative dependency. This is the case for ethanediol, p-xylene, and certain rare gases, whose import shares from the Middle East exceed 40% in some instances. These are essential inputs for the chemicals and plastics industry. Although dependence on these materials is high, the absolute value of their imports is very low. Therefore, the key to determining the level of disruption in certain industrial value chains is substitutability, particularly in the short term.

The sectors most exposed to this risk, therefore, are oil refining, the chemicals industry and, indirectly, manufacturing activities that are intensive in petrochemical derivatives. For 2026, this risk highlights the strategic importance of geographically diversifying suppliers, strengthening critical inventories, and accelerating the development of technological alternatives in order to reduce reliance on imports from geopolitically vulnerable regions.

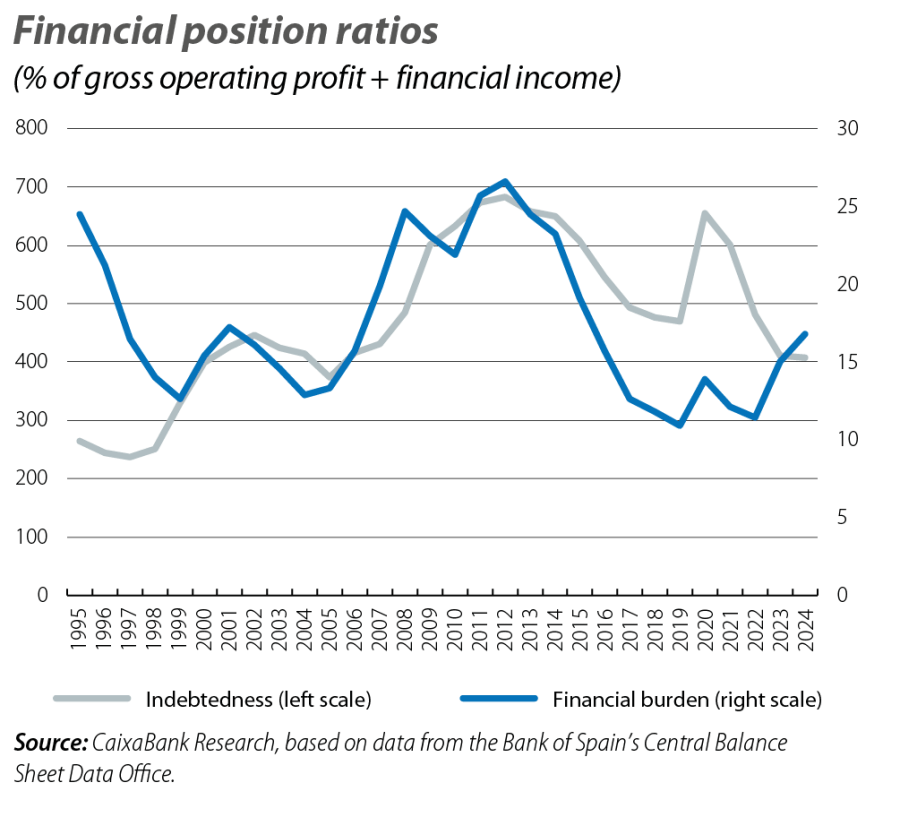

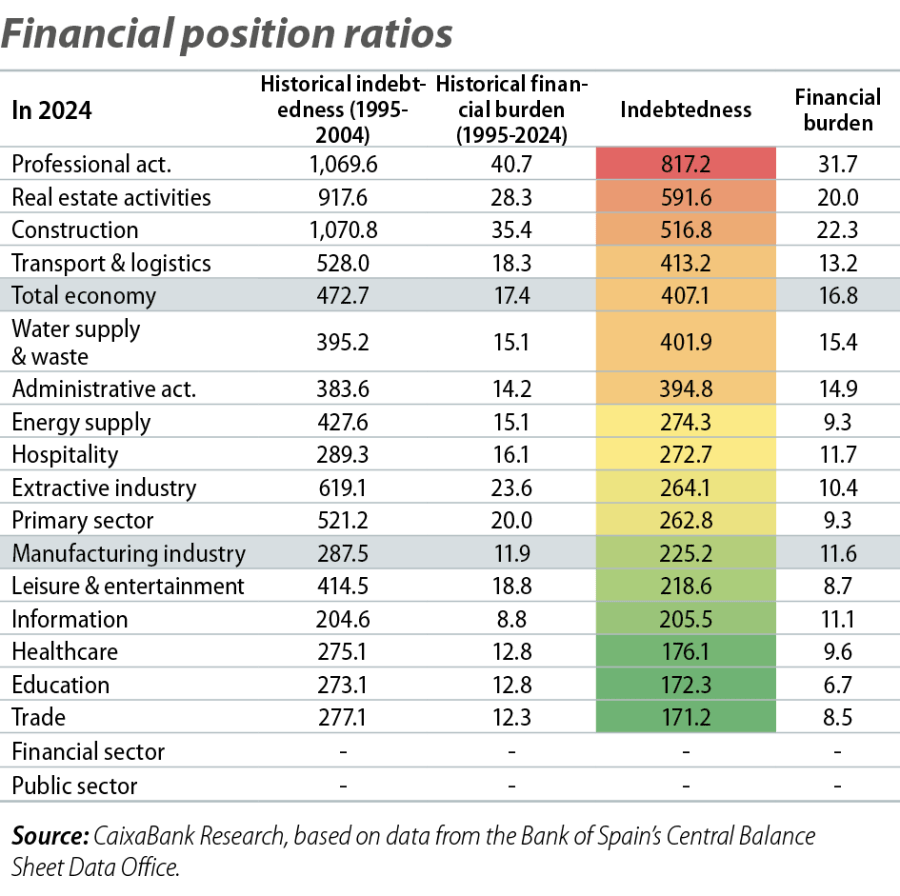

Increase in financing costs

The energy shock has led to increased expectations of interest rate hikes by central banks and has caused a rise in market interest rates (e. g., the 12-month Euribor has increased from 2.2% at the end of February to 2.8% in recent weeks). This increase in financing costs will impact sectors heterogeneously.

Construction, real estate activities, and transport and logistics are capital-intensive sectors and have traditionally shown higher leverage ratios than the economy as a whole. Consequently, they have historically shown greater sensitivity to interest rates. However, the deleveraging accumulated in recent years ought to cushion the impact of a new cycle of rate hikes.

The manufacturing industry, despite its capital intensity, shows more moderate levels of leverage, which would limit the direct impact of rising financing costs. Most service sectors, on the other hand, have low debt ratios.

The hospitality sector stands out, having managed to reduce its leverage below its historical average after the surge in debt levels during the pandemic.

Ultimately, the Spanish economy is facing the shock of the war in Iran from a position of widespread strength. Nevertheless, sectors’ exposure to these transmission channels varies widely. Manufacturing combines greater energy dependence and exposure to global trade, while construction is sensitive not only to energy prices but also to financing costs. We anticipate that services will show greater resilience, although there will be significant exceptions in transport and logistics, which are more exposed to rising fuel costs and a potential slowdown in foreign demand. Overall, the aggregate impact should be contained, but there are significant sectoral risks where energy intensity, low substitutability of inputs, international exposure, and higher leverage converge.

Geopolitics

We analyse the major geopolitical trends and thier effects on the financial markets and the economy.