Household savings, income and finances in Spain: how did they fare in 2025 and what can we expect for 2026?

In this article, we analyse the factors behind the recent evolution of Spain’s household savings rate and the outlook for 2026, in a context marked by the conflict in the Middle East, which could lead to higher inflation and potential interest rate hikes.

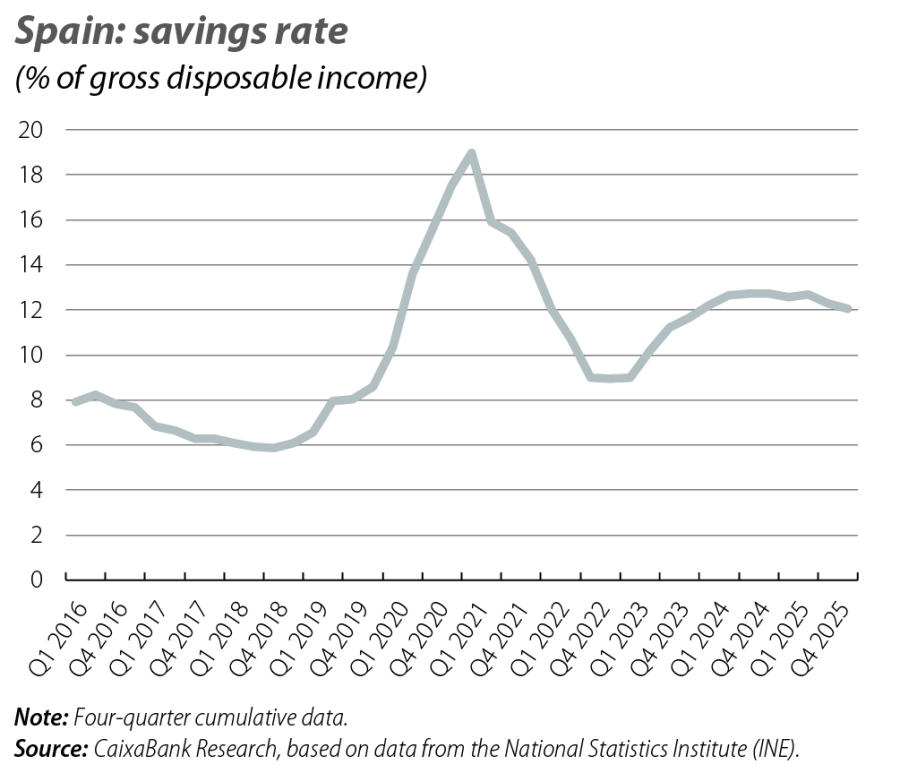

The household savings rate, measured as gross savings as a percentage of gross disposable income (GDI), decreased moderately in 2025, from 12.7% to 12.0%, as a result of the growth of consumption expenditure outpacing that of disposable income. In aggregate terms, gross savings amounted to 128 billion euros in 2025 – a notable figure (7.6% of GDP), albeit 700 million less than the previous year. This reduction is consistent with the context of lower interest rates and stabilisation of inflation, factors that can act as a spur to boost consumption. Despite the decline, the savings rate remains well above the historical average of 8.6% observed between 2000 and 2019, suggesting that households retain a significant financial buffer. In this article, we analyse the factors behind this pattern and the outlook for 2026, in a context marked by the conflict in the Middle East, which could lead to higher inflation and potential interest rate hikes.

2025 recap: a healthier financial position

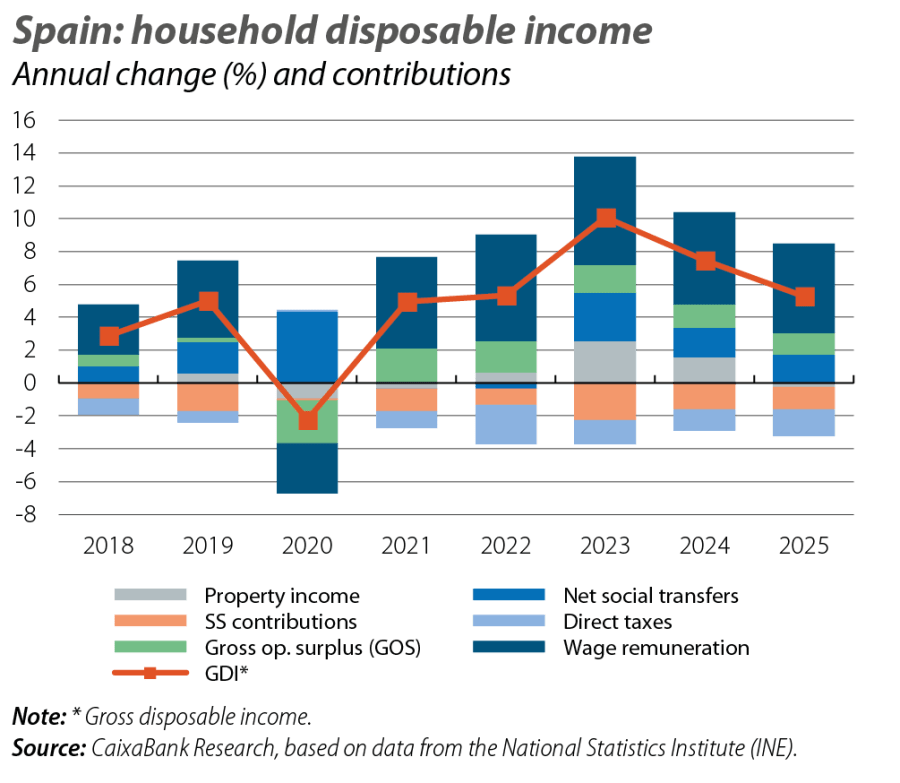

The moderate decline in the savings rate in 2025 is primarily due to a 5.3% year-on-year growth in nominal GDI. This is a solid growth rate, albeit lower than that observed in 2024 (7.5%) and clearly surpassed by the increase in final household consumption expenditure, which was 6.2%. The growth of GDI was driven by the strong performance of the labour market: total wage-earner remuneration increased by 7.2% year-on-year, reflecting both the rise in the number of employees in terms of full-time equivalent jobs (+3.3%) and the growth in remuneration per worker (+3.9%). The gross operating surplus (income from self-employed workers, imputed rents for owner-occupiers, etc.) also contributed positively, growing by 5.1%, as did some components of net property income, such as dividends and other investment income, which recorded strong growth. This vigour was partially offset by the opposing contribution of the public sector: direct taxes paid by households grew by 10.5% in 2025, especially in the second half of the year, more than offsetting the 6.2% increase in social benefits. This increase in taxes is explained by the strength of employment, the good performance of tax revenues on capital and labour, and the lack of updates to personal income tax brackets. As a result, primary gross income (before taxes or transfers) grew by 6.0% in 2025, outpacing the growth of final GDI.

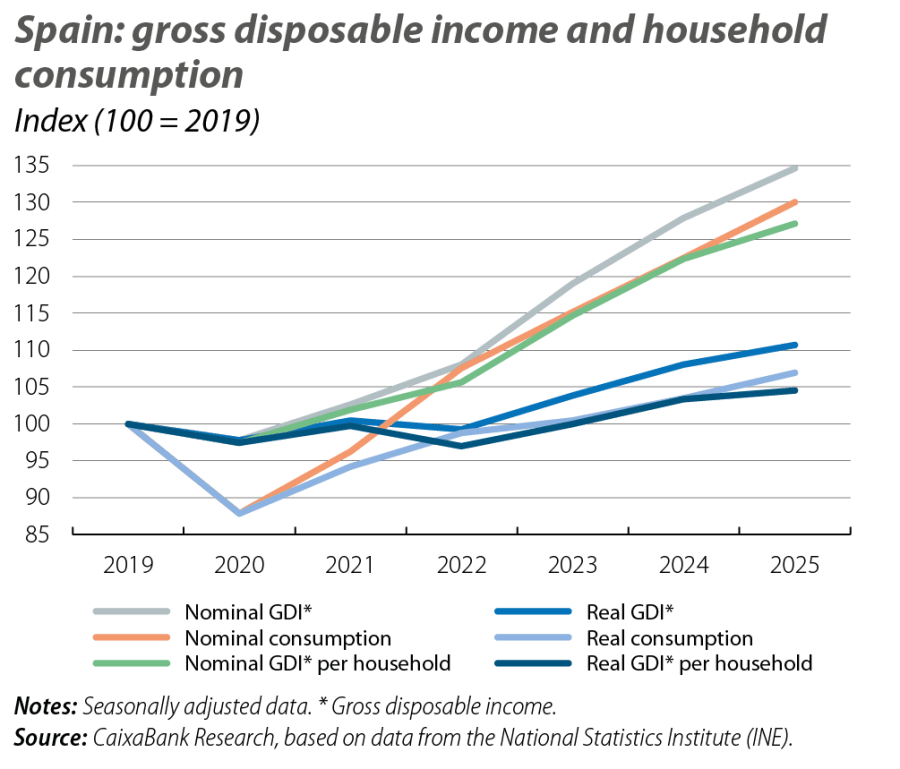

In 2025, GDI grew above the rate of average annual inflation (2.7%) and the growth in the number of households (1.3% according to the LFS), which allowed for a recovery in purchasing power. In this context, real household income has grown by 4.5% since before the pandemic, highlighting that households have continued to gain purchasing power in real terms.

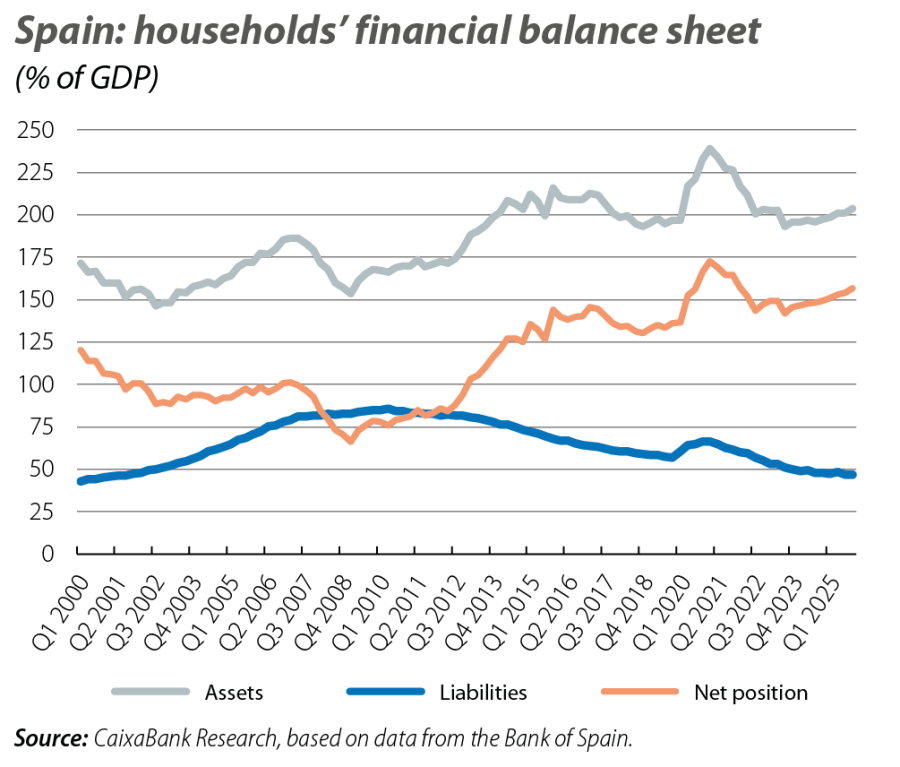

The strong financial position of households is reflected not only in the high savings rate but also in their financial accounts. In this regard, households’ financial wealth continued to increase in 2025: their financial assets amounted to 3.4 trillion euros at the end of the year, versus 3.1 trillion at the end of 2024. This increase of 292 billion euros is broken down into a net acquisition of financial assets amounting to 95 billion, higher than the 21.5-billion average in the period 2015-2019, when interest rates were very low, and a revaluation effect of 194 billion. When breaking down the net acquisition of assets, we note that households invested 42 billion euros in equities and investment funds, just under 9.6 billion less than in deposits, while they disposed of debt securities worth 6 billion following the fall in interest rates.

On the other hand, households continued to deleverage in 2025, and by the end of the year their financial liabilities1 stood at 46.9% of GDP, compared to 47.8% in 2024, the lowest level since the end of 1998. This decline reflects the fact that, in 2025, households took advantage of the interest rate drop to prudently incur debt: net new borrowing amounted to 35 billion euros, representing an increase of 3.8%, which is lower than the nominal GDP growth of 5.8% and the GDI growth of 5.3%.

As a result of the increase in financial assets and the decrease in liabilities as a percentage of GDP, the net financial wealth of households recorded a notable increase of 7.3 points compared to 2024, reaching 156.8% of GDP.

- 1

Financial liabilities include the outstanding balance of bank loans, commercial loans and other amounts payable (accrued loan interest, taxes and social security contributions payable).

2026 outlook: income dynamism and a savings rate with much greater downward resistance than in the 2022 energy crisis

Looking ahead to the remainder of 2026, GDI is expected to maintain dynamic growth, supported by the strength of the labour market. The data for the 2025 year end, together with the strong labour market data for Q1 2026 and the projected increase in pension spending, which AIReF estimates at 5.1% (broken down into 2.7% for value updates and 2.4 pps due to the substitution effect in favour of higher pensions), suggest that GDI could grow by around 4.5% this year.

The evolution of the savings rate will be influenced by opposing forces. On one hand, the resurgence of inflation associated with the tensions in the Middle East could boost nominal consumption growth if households try to maintain their real consumption level, which could reduce the savings rate. On the other hand, an increase in uncertainty and interest rates could cause households to postpone their consumption and investment decisions and could encourage greater precautionary savings. In 2022, with the energy crisis triggered by the war in Ukraine, we saw a sharp decline in the savings rate. However, in that episode, a rebound in consumption was already occurring following the end of the COVID-19 restrictions and the inflation shock was very concentrated in non-discretionary items of the consumption basket, such as electricity prices. On this occasion, given that there are no substantial increases in electricity bills and fiscal policy is cushioning the impact of rising fuel prices, households have more leeway to adjust their consumption decisions in response to the new shock.

Before the war, we expected the savings rate to decline moderately from 12.0% in 2025 to 11.5% in 2026. Following the outbreak of the conflict, however, there is significant uncertainty over where the savings rate will finally settle. For illustrative purposes only, let us suppose that the savings rate absorbs 50% of the shock on real consumption in 2026 – a prudent assumption if we compare it with the experience of 2022, when it absorbed the entirety of the increase in inflation – and that average inflation this year is 1 pp higher than estimated prior to the war. Under these assumptions, which are consistent with a short-lived conflict and a contained macro impact, the growth of nominal expenditure this year would be around 1 pp above that of GDI, and the savings rate would be around 11% of GDI by the end of 2026, half a point less than forecast before the war. Conversely, if the precautionary savings channel becomes more dominant, then the cushioning effect of the savings rate on consumption would be less or could even lead to increases in the savings rate, as occurred in 2008 and 2009 at the start of the financial crisis. All this will depend on the duration and severity of the conflict, as well as the impact on household expectations.

Ultimately, the high savings rate observed at the end of 2025 and the good financial situation of households allow us to face the impact of the war in Iran on consumption from a position of strength, in a context of high global uncertainty.