European households’ well-being: greater reliance on public support amid higher inflation

Between 2013 and 2019, the recovery that followed the financial and sovereign debt crises enabled gradual but sustained improvements in household purchasing power, supported by an improvement in employment and a contained inflation environment. The pandemic disrupted this dynamic, and while nominal income and the labour market showed resilience, the inflation shock exacerbated by the invasion of Ukraine eroded purchasing power and strained households’ well-being, hitting low-income households particularly hard. In this context, real actual individual consumption per capita – a broad indicator of material well-being that includes both private expenditure and individual goods and services provided by the public sector – allows us to analyse how the living conditions of European households have evolved before and after the pandemic, as well as the role of public redistribution.

From post-crisis recovery to inflation shock

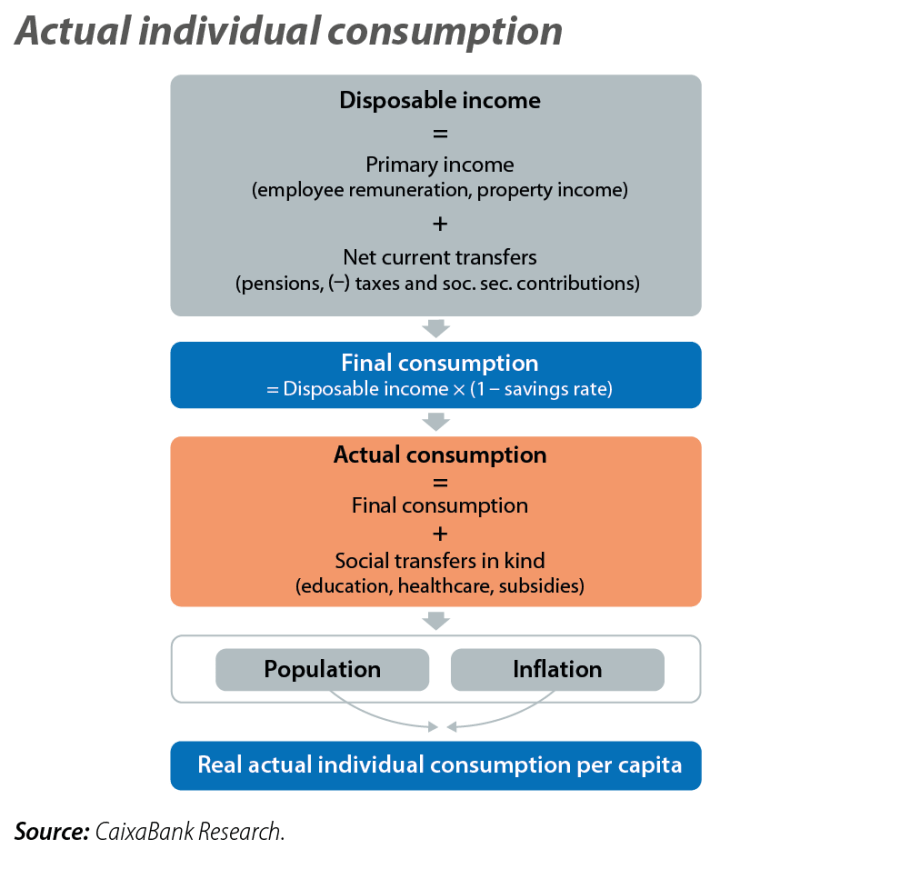

Real actual individual consumption per capita is an indicator that reflects the material well-being of households more accurately than GDP, disposable income, or final consumption (see the first chart for definitions). It is a measure that is less sensitive to temporary deviations between production, household income and savings, which are particularly relevant after the pandemic and during the recent inflation shocks.1 Unlike other metrics, it includes public sector transfers in kind – such as education and healthcare, as well as subsidised housing or transport – so it better reflects households’ access to goods and services.

- 1

IMF (2020). «Measuring Economic Welfare: What and How?».

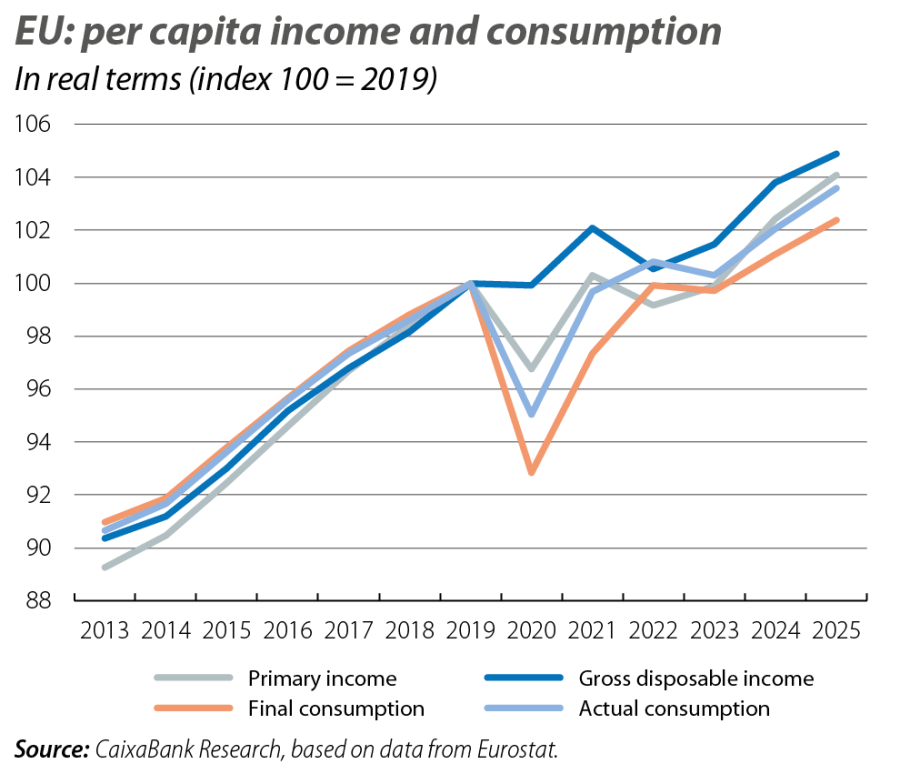

Between 2013 and 2019, actual individual consumption per capita in the EU grew steadily at around 1.5% annually. This was in line with a phase marked by rising incomes and a gradual normalisation of the economy following the financial and sovereign debt crises (see second chart). The progress of this measure of well-being was somewhat less pronounced than that of GDP, but it was nonetheless steady, supported by an improvement in employment and a moderate inflation environment (less than 1% annually on average). This dynamic changed abruptly with the pandemic. The initial collapse in private consumption in 2020 was followed by a relatively swift recovery, driven by expansive fiscal policy, although heightened uncertainty may have led to a structurally higher savings rate.

However, the real turning point was not the pandemic itself, but the subsequent inflationary episode. Between 2021 and 2023, the sharp rise in energy and food prices eroded household purchasing power. The EU’s average annual inflation reached a historic high of 9.2% in 2022, creating a persistent gap between the trends of variables in nominal and real terms. In turn, this inflation shock had a distinctly regressive nature. Households with lower incomes faced significantly higher inflation rates as they devoted a larger share of their spending to basic goods, which were precisely the category that registered the biggest price increases during this period.2 Furthermore, in some countries there was a deterioration in housing affordability.3

- 2

ECB (2024). «The unequal impact of the 2021-22 inflation surge on euro area households».

- 3

See the Focus «There are reasons why housing has become the top concern among European citizens» in the MR02/2026.

Less convergence and more dispersion between countries after the pandemic

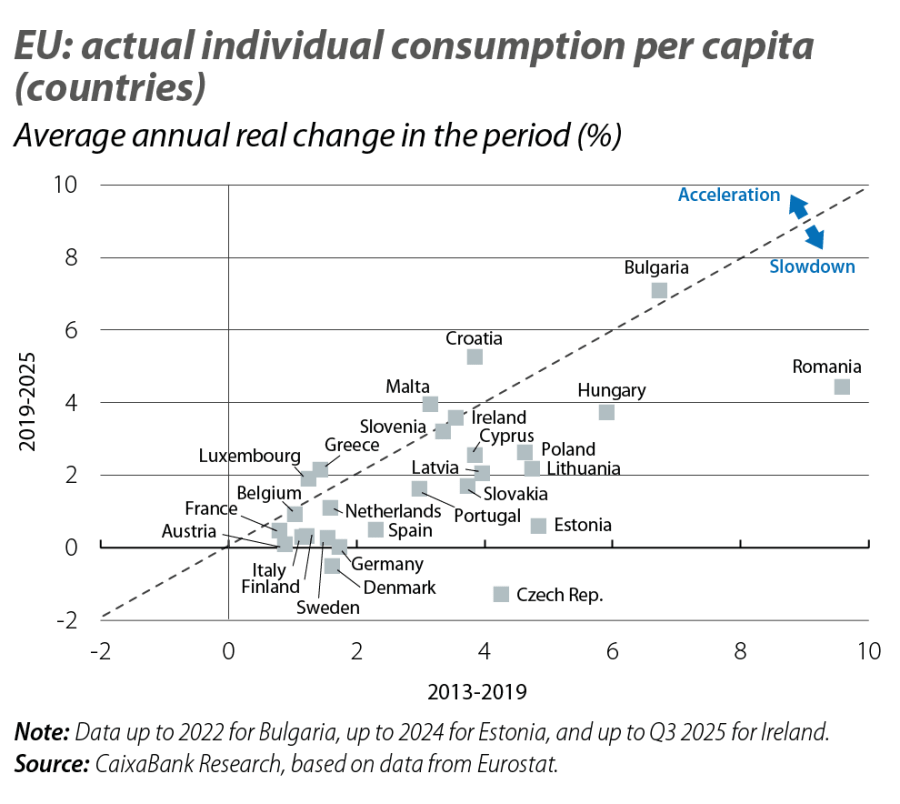

Beyond the European aggregate, the comparison between countries reveals significant changes in growth and convergence dynamics. This is largely explained by the uneven impact of inflation and the varying fiscal space that was available to countries to respond. Generally speaking, the average growth of real actual individual consumption per capita during the period 2019-2025 was significantly lower than that recorded in the years prior to the pandemic for most of Member States (see third chart). Only a few countries have managed to sustain growth in actual individual consumption, while others have experienced a more pronounced slowdown, mainly in Eastern Europe. The four major EU economies (Germany, France, Italy and Spain) have shown stagnation in recent years.

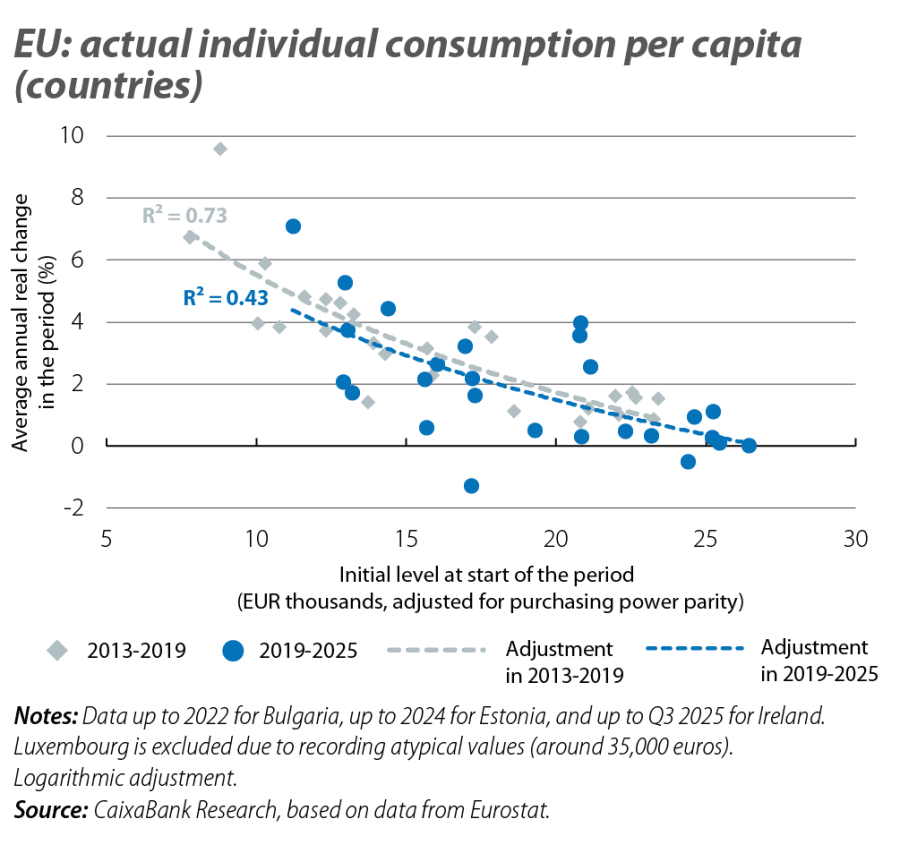

In the years leading up to the pandemic, countries with lower initial levels of actual individual consumption per capita tended to record significantly higher growth rates, indicating a gradual convergence in well-being (see fourth chart). This trend weakens after 2019. The asymmetric impact of the inflation shocks, combined with differences in fiscal space, has led to less uniformity in outcomes among Member States. The pandemic and the subsequent shocks have not reversed previous progress, but the result has been slower convergence (see in the chart how the blue dotted line lies below the grey one and the how the slope is steeper for lower levels of well-being) and less uniformity (greater dispersion of the blue scatter plot), with significant structural differences persisting within the EU.

Sustaining well-being in an inflationary environment: limits of redistribution

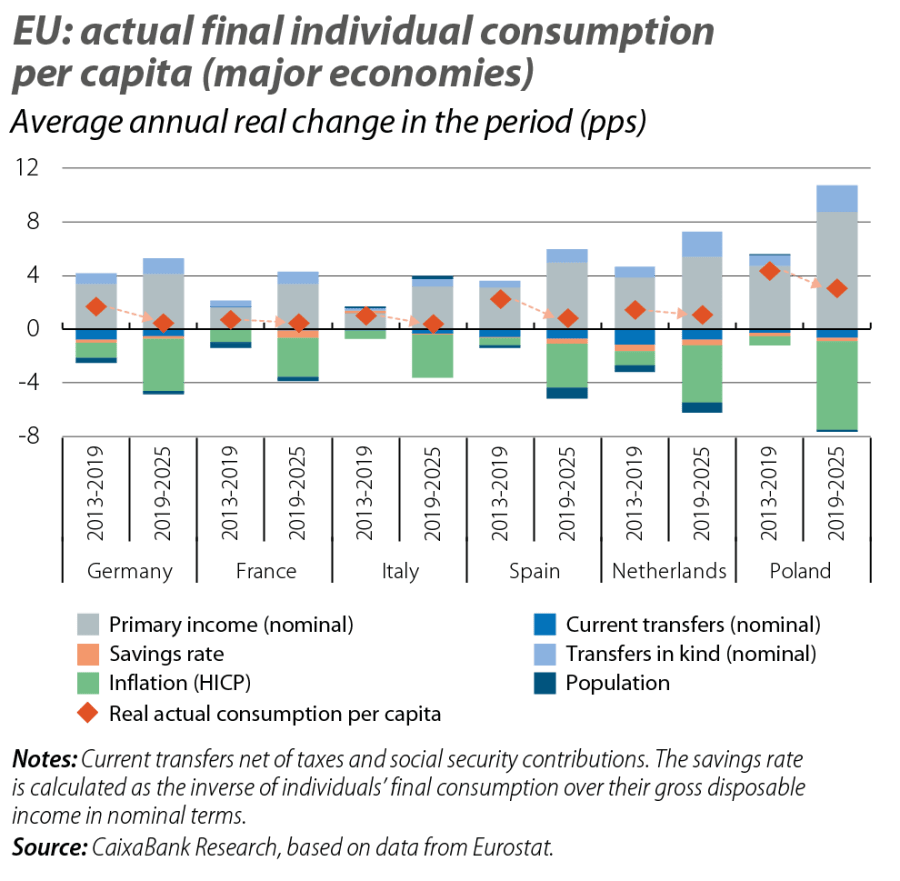

The analysis of the main EU economies clearly shows the shift in pattern between the two periods. Between 2013 and 2019, the growth in real actual individual consumption per capita was mainly supported by the increase in real incomes and contained inflation. However, following the pandemic, the key differentiating factor is the sharp rise in inflation, which has significantly eroded purchasing power despite the strength of the labour market (see fifth chart). In response, public transfers have played a greater cushioning role – particularly in the Netherlands, Poland, and Germany – alongside a gradual decline in the savings rate following the sharp rise in 2020-2021, which is more pronounced in France, Spain, and Italy. In the case of Spain, the per capita results are also influenced by the rapid population increase due to higher migration flows in the recent period.

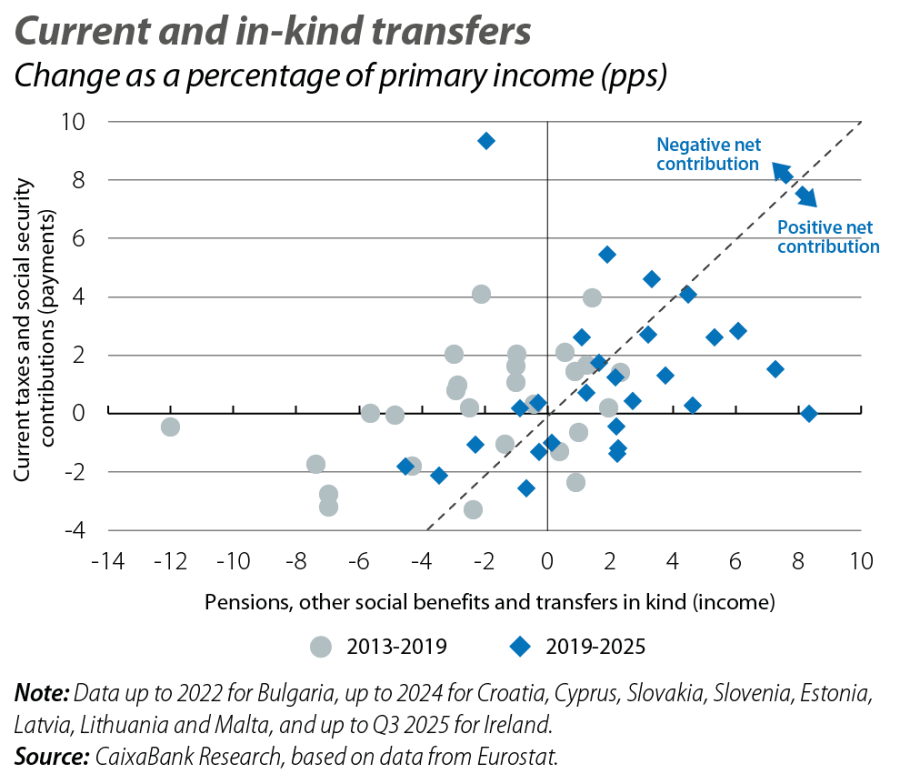

Across Member States, the more active role of redistribution following the pandemic has been a widespread but uneven phenomenon (see sixth chart). In most countries, the increase in transfers – whether monetary or in kind – has been accompanied by higher contributions through taxes and social security. However, in many cases, this increase has not been fully offset on the fiscal revenue side. In contrast, only a minority of countries have shown a negative net contribution from transfers to the growth of actual individual consumption in recent years.

Implications for cohesion and pursuit of the competitive agenda

Since the pandemic, EU government action has helped cushion the impact of a series of unprecedented shocks on households’ material well-being, preventing an abrupt fall in actual individual consumption per capita. However, this result has increasingly relied on public redistribution mechanisms and has occurred in a context of reduced convergence between countries. The erosion of purchasing power caused by inflation has highlighted the limits of a model based on ex post cushioning of well-being. Looking ahead, preserving economic cohesion will require stronger EU competitiveness fundamentals: boosting productivity and deepening the single market.4 Without progress in boosting potential growth and job creation, maintaining well-being will become increasingly costly and more difficult to align with European convergence in an environment of high public debt.5

- 4

See the Focus «How far has the EU progressed on the Competitiveness Compass?» in the MR04/2026.

- 5

See the article «Europe’s medium-term fiscal dilemma» in the Dossier of the MR11/2025.