Spain maintains solid growth despite heightened uncertainty

The macroeconomic outlook is once again influenced by increased geopolitical uncertainty due to the conflict in Iran, which is primarily affecting energy prices. Spain is facing this scenario from a solid starting position, following a dynamic 2025 and a better-than-expected Q1 2026.

Growth: slightly less, yet dynamic

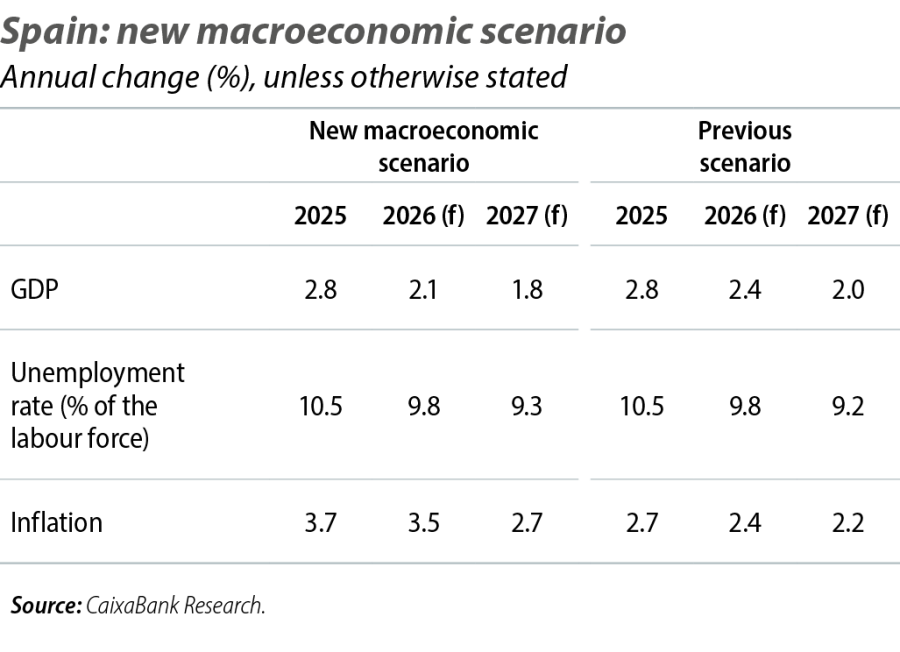

The macroeconomic outlook is once again influenced by increased geopolitical uncertainty due to the conflict in Iran, which is primarily affecting energy prices. Spain is facing this scenario from a solid starting position, following a dynamic 2025 and a better-than-expected Q1 2026. Growth is supported by strong private consumption and employment, the good performance of service exports, and investment that continues to benefit from European funds. These factors, along with significant accumulated household savings and support from fiscal policy, act as buffers amid a deteriorating international environment. Nevertheless, the surge in energy prices and weaker foreign demand will dampen economic activity and push inflation upwards. Consequently, we have moderately revised down our GDP growth forecasts to 2.1% in 2026 and to 1.8% in 2027, versus 2.4% and 2.0% previously. Despite this, the underlying assessment remains unchanged: the Spanish economy is expected to continue growing at a relatively strong pace, supported by multiple factors and clearly outperforming the European average, which is projected to remain below 1%.

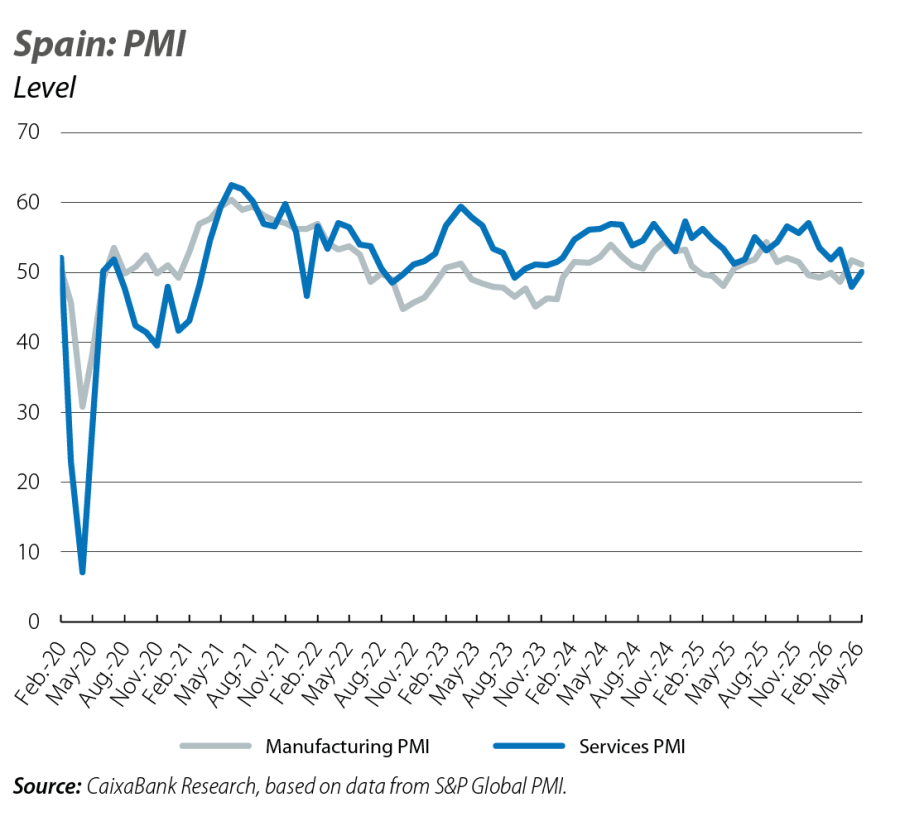

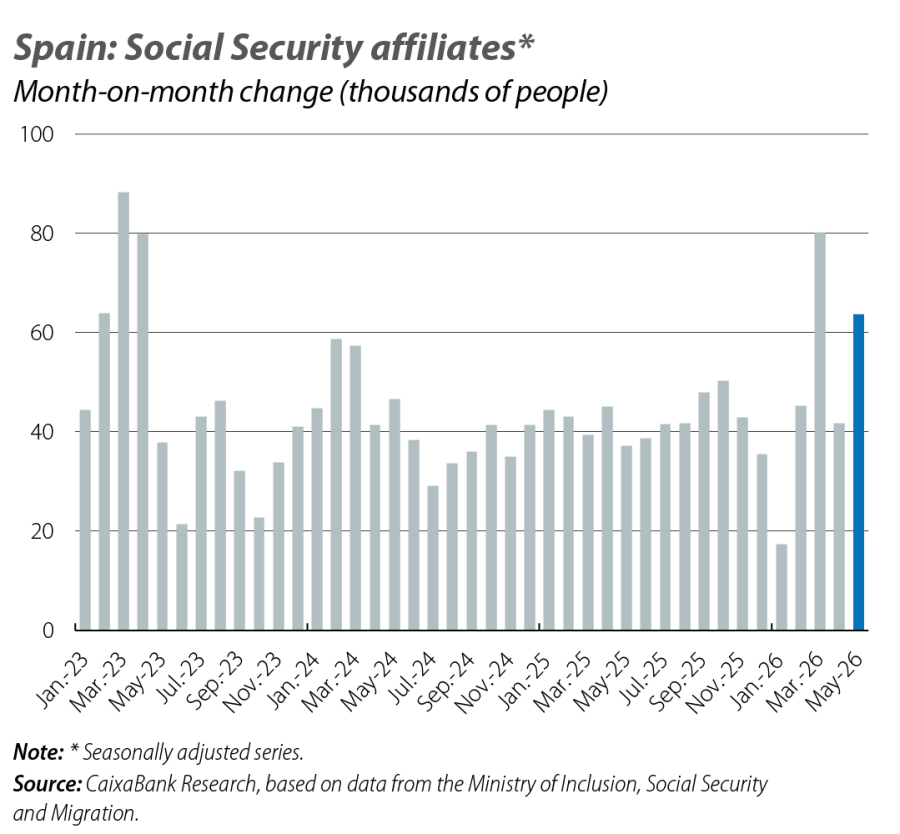

The economic activity data for Q2 are relatively positive

The economic activity data for Q2 are relatively positive, revealing a strong labour market, but also emerging signs of weakness in private consumption. So far in the Q2, seasonally adjusted Social Security affiliation has increased by 0.6% quarter-on-quarter, 0.1 pp more than in Q1. In May, the integration of immigrants following the exceptional regularisation of undocumented workers has begun to be reflected, but even excluding these new entries, the figures remain dynamic. We estimate that, of the more than 63,000 new registrations, approximately one-third (in seasonally adjusted terms) are due to the regularisation process. Excluding this group, the increase in registered workers would be 0.2% month-on-month, a rate comparable to that of Q1. The PMIs suggest positive momentum in Q2: the manufacturing PMI stood at 51.2 points in May, meaning the sector remains in expansion, as it is above 50 points. Production continues to increase slightly, offsetting weak demand, declining orders, and rising costs in the wake of the Middle East conflict. The services PMI rebounded in May, returning to expansionary territory at 50.1 points, after April’s 47.9, ahead of a summer tourism season that is expected to be very good if the conflict in the Gulf is resolved in a timely manner. However, the impact of the shock is beginning to be seen in consumption indicators. In April, retail sales fell by 1.5% month-on-month, and year-on-year growth slowed significantly, from 4.1% to 0.8%. Our internal indicator for domestic consumption also aligns with this loss of momentum: in April and May, consumption growth was 1.6% year-on-year, far short of the 3.5% recorded in Q1, although part of the observed trend is due to temporary factors (base effects and the Easter calendar).

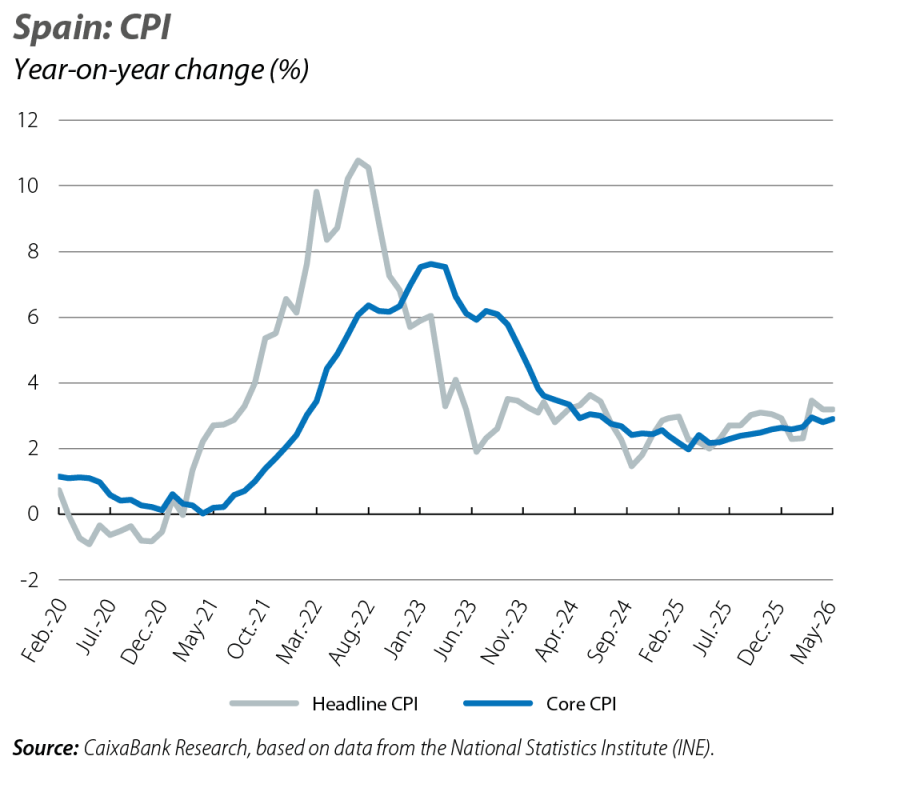

Inflation remains above 3% due to energy

The new CaixaBank Research forecasts raise inflation to 3.5% in 2026 and to 2.7% in 2027, versus the previous 2.4% and 2.2%. This new scenario reflects a direct impact from the Iran war in 2026 through energy prices and, in 2027, through indirect effects (a gradual and moderate spill-over to industrial goods and food). The preliminary data for May were consistent with this scenario: headline inflation at 3.2% (as in April) and core inflation at 2.9% (0.1 pp higher). Of particular note was the increase in services (0.6 pps, to 4.0%) driven by transport and recreational activities. This was partly due to a rebound following an unusually low April caused by calendar effects. In June, we expect to see a temporary rebound focused in energy following the removal of tax discounts on electricity and gas. With prices consistent with current futures, inflation could be around 4% in June, before steadily easing thereafter.

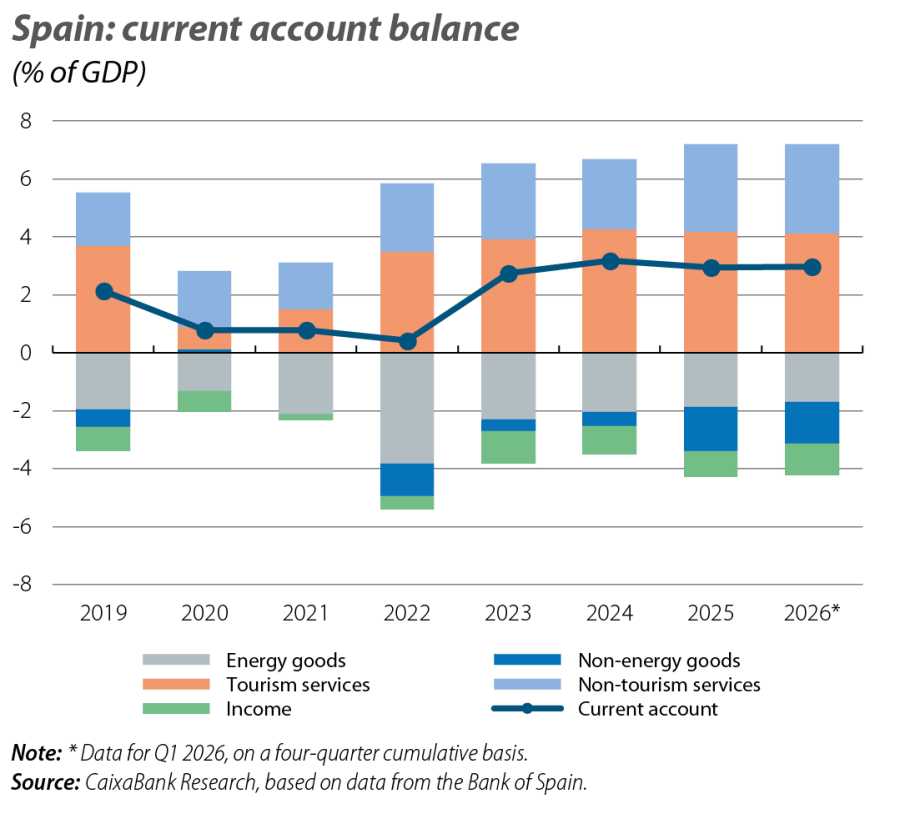

The current account balance performs well, hardly affected by the Iran war with data to March

The current account surplus stood at 3.0% of GDP (annualised), consistent with the figure recorded a year earlier and in line with the fundamentals of our narrative: a resilient economy despite the high uncertainty. Moreover, the economy is still supported by the strong dynamism of services (both tourism and non-tourism), which more than offsets the deterioration in the balance of trade in goods, in a context of stronger domestic demand and geopolitical disruptions. The tourism surplus stood at 4.1% of GDP and remains strong despite a slight moderation due to the increased growth of tourism imports – a trend that could be reinforced by the potential redirection of tourist flows due to the Gulf war. Non-tourism services significantly increased their contribution to 3.1% of GDP, compared to 2.6% a year earlier, thanks to the strong growth in exports. In the trade of goods, the pattern was more mixed: the non-energy goods deficit widened to –1.4% of GDP, in a context of stronger imports driven by rising domestic demand, while the energy deficit moderated to –1.7% of GDP. Thus, despite recent tensions in energy prices, the energy balance (12-month cumulative basis) has not yet deteriorated.

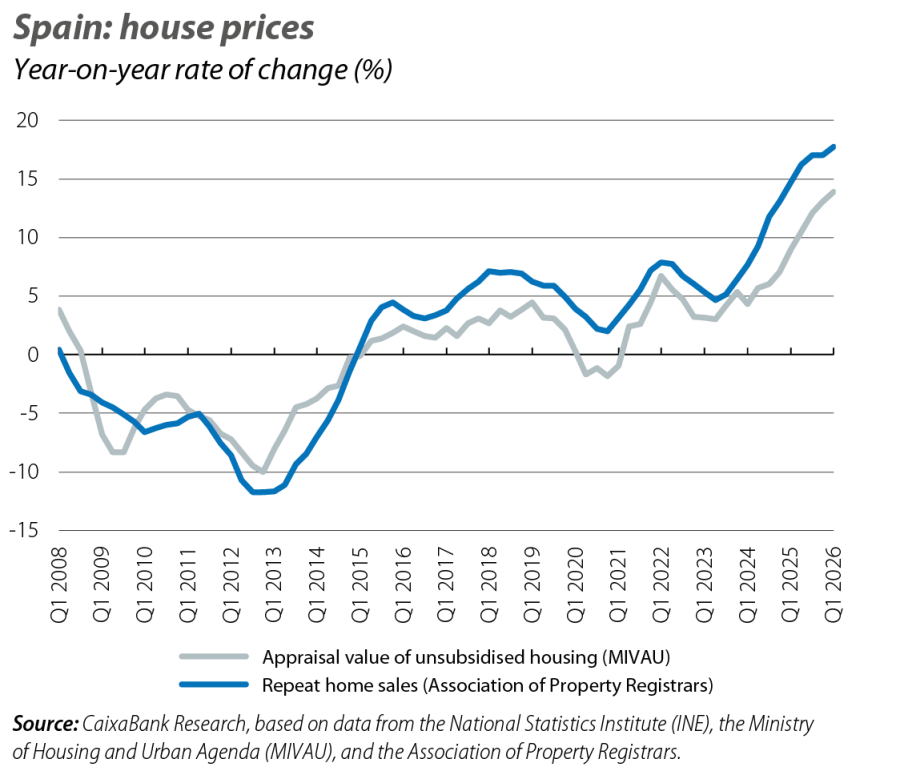

In the housing market, the gap between supply and demand continues to be reflected in price behaviour

Price growth remained high in Q1, with a quarter-on-quarter increase of 3.8% and a year-on-year rise of 13.9%, amid a persistent imbalance between insufficient supply and highly dynamic demand. Several factors already analysed have driven demand: rising incomes, demographic growth and a strong labour market. Although new construction permits have increased, actual production is still failing to fully meet demand, underscoring the need to accelerate the increase in supply in order to prevent further price pressures. This imbalance leads us to anticipate that house prices will continue to rise significantly in the coming quarters, even with the prospect of the ECB raising rates.