The Spanish economy at a crossroads: slowdown or recovery?

The partial reopening of the Strait of Hormuz following the recent agreement signed between the US and Iran has significantly eased tensions in the energy markets, reducing the pressure that has been building on the economy and dispelling the spectre of a slowdown.

The improvement in the outlook for the US-Iran conflict reduces the early warnings of a slowdown in our economy

Four months after the outbreak of the conflict, signs began to emerge last month indicating that the economic growth rate might be affected by the conflict’s impact on the energy market, confidence and financial conditions. However, the partial reopening of the Strait of Hormuz following the recent agreement signed between the US and Iran has significantly eased tensions in the energy markets, reducing the pressure that has been building on the economy and dispelling the spectre of a slowdown.

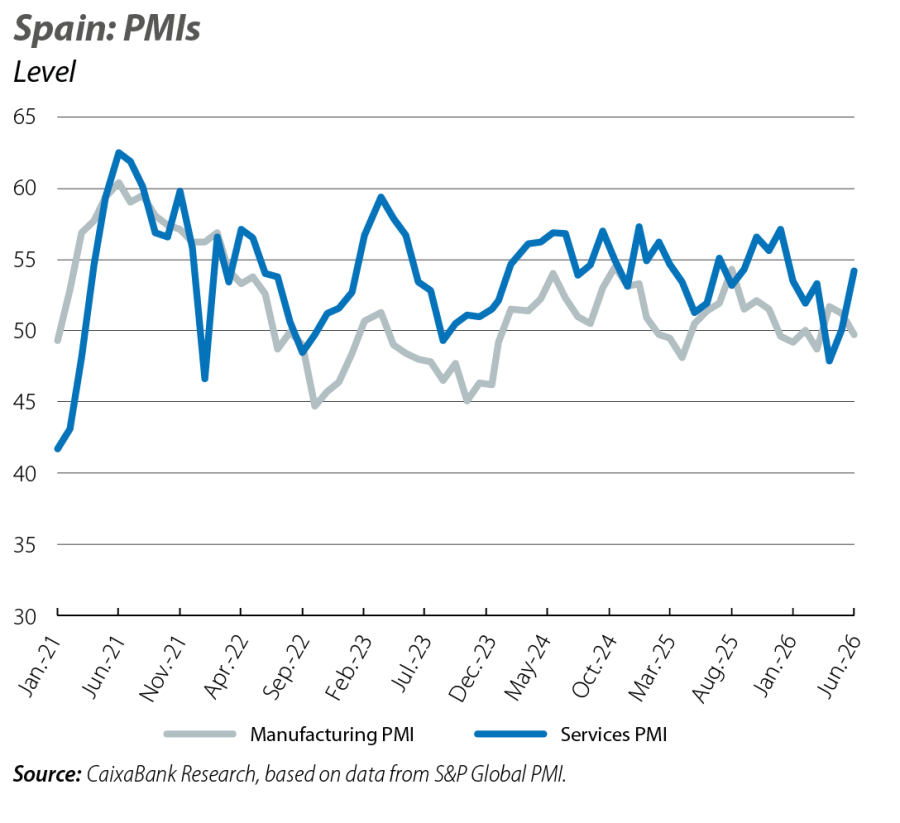

Activity indicators have improved compared to the previous month

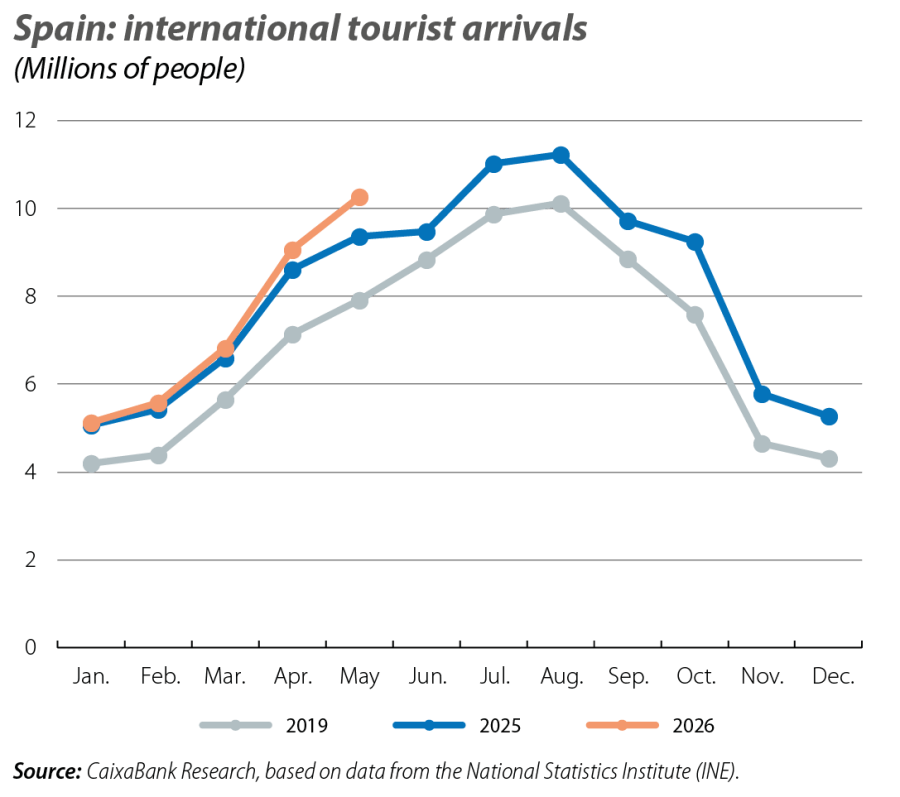

On the consumption side – the area expected to be hardest hit by rising inflation – we observed good performance in May. The retail trade index rose by 0.6% month-on-month, recovering some of the ground lost in April’s poor result (–1.5%). However, the average for April and May remains 0.5% below the average for Q1. In the same month, industrial production recorded strong growth, with the year-on-year rate accelerating from 2.3% to 3.4%. The data for the tourism sector were very encouraging. In May, international tourist arrivals were up 9.5% and 10.9% year-on-year, compared to 1.2% and 4.6% recorded in May of the previous year. This improvement aligns with the view that Spain’s tourism sector should benefit from the Middle East conflict due to the redirection of tourist flows, hinting at a record high season. Finally, the composite PMI rose significantly in June, reaching 53.3 points (50.1 the previous month). This places it well above the threshold indicating no change (>50 points) and is the highest level since December 2025. Overall, and considering the labour market data discussed below, the set of indicators suggests that GDP growth in Q2 2026 could exceed the 0.3% quarter-on-quarter rate envisaged in our forecast.

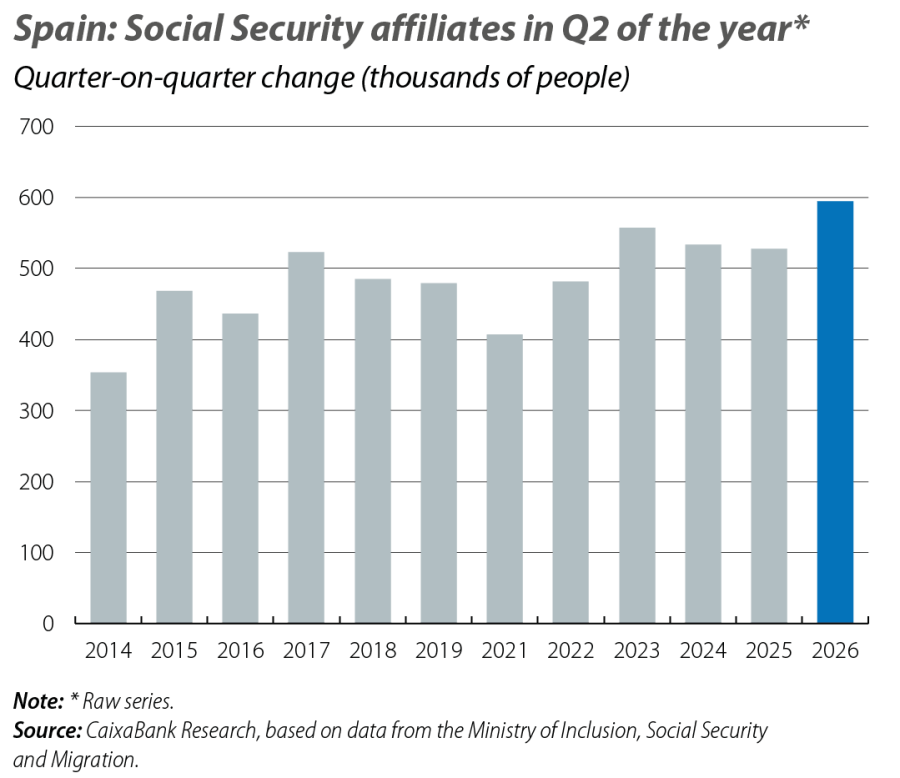

The labour market ends Q2 with strong growth in registered employment due to the impact of the regularisation of undocumented workers, although even without this effect the growth rate remains dynamic

In Q2 as a whole, the number of registered workers grew compared to the Q1 average by around 595,000 people. This growth exceeds the figure of 540,000 recorded on average in the second quarters of 2023 to 2025. However, according to the government, some 160,000 workers were registered due to the exceptional regularisation process. Therefore, net of this effect, the quarter-on-quarter change stands at around 435,000 workers, which is slightly below the usual figure for this quarter of the year. In seasonally adjusted terms, we estimate that the corrected figure represents a quarter-on-quarter growth in affiliates of 0.5% in Q2 – a dynamic growth rate in line with that of the previous quarter.

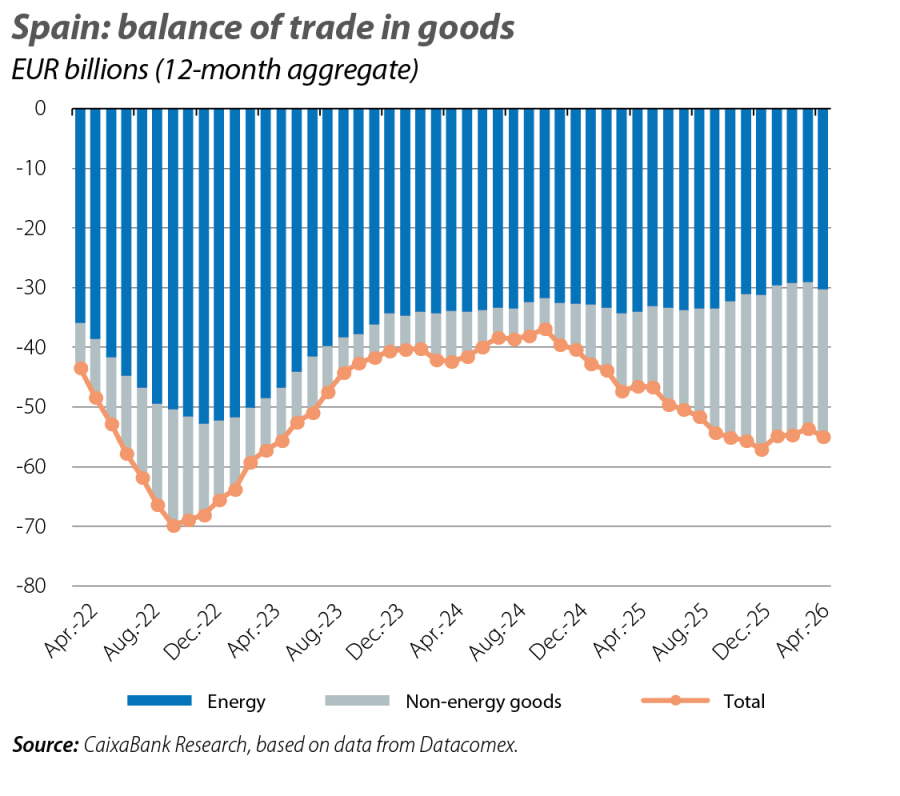

The rise in energy prices is beginning to show in external sector data, but without disrupting the steady improvement in the trade balance since the start of the year

In April, the trade deficit stood at 5.172 billion euros, up from 3.882 billion euros a year earlier, due to import growth of 8.7% year-on-year, compared to a 5.8% increase in exports. This import growth was driven by the surge in energy product imports (+32.2%), mainly due to higher prices. Despite the deterioration due to the energy component in April, the cumulative trade balance between January and April shows a deficit of 16.85 billion euros, lower than the 18.982 billion recorded in the same period of 2025. However, the May and June figures are expected to show a continued deterioration in the energy balance, hindering any improvement in the overall trade balance.

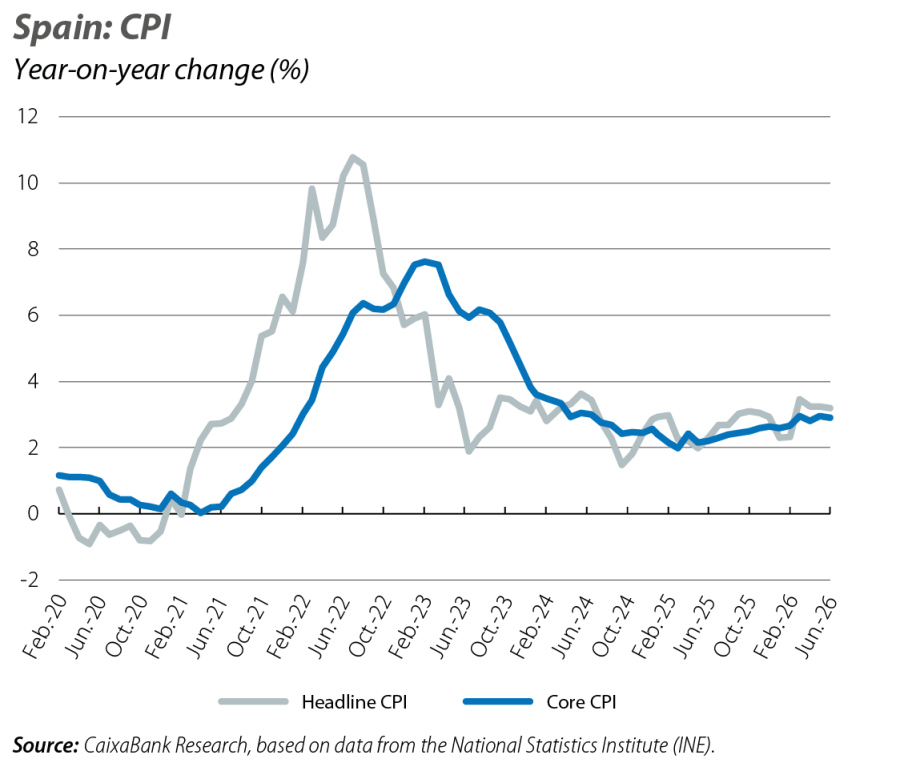

Inflation in June remains stable at 3.2%, but begins to reflect the effects of falling energy prices

Although the tax support measures on gas and electricity bills were withdrawn in June, energy inflation barely accelerated compared to the previous month. This was made possible by the sharp drop in fuel pump prices, reflecting the decline in oil prices in international markets. Core inflation fell by 0.1%, although it remains high at 3.1%, largely due to the services component. This is affected by transport costs, particularly air travel, which is the category most directly impacted by the recent rise in energy prices. Over the coming months, we are likely to see a rise in inflation due to the gradual withdrawal of tax subsidies on fuels. However, the drop in oil futures prices suggests that the inflation path for the rest of the year will be lower than we were anticipating before the US-Iran agreement.

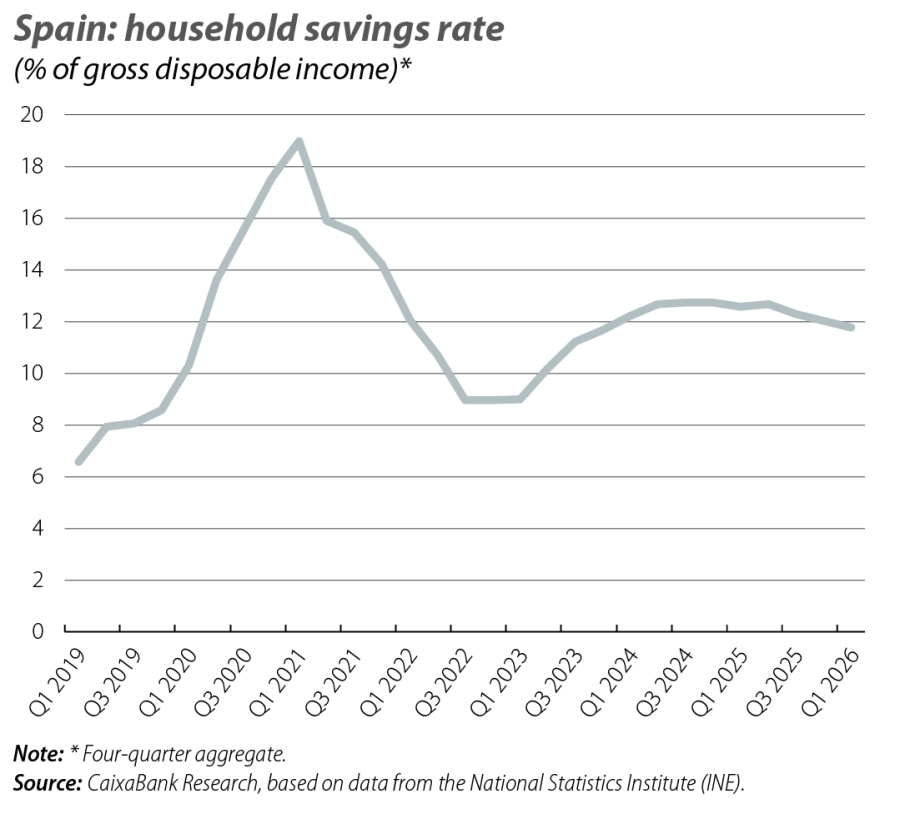

In the lead-up to the conflict in Iran, the household savings rate remained high

In the four-quarter aggregate, the household savings rate stood at 11.8% in Q1 2026, just 0.2 pps below the previous month’s figure and significantly above the 2015-2019 average of 7.3%. This high savings rate provides a buffer for households to cope with the rise in inflation in Q2. Whether or not they will use this buffer remains to be seen. For now, the slight deterioration observed in consumption-related indicators suggests that households may have chosen to protect their savings and adjust their consumption decisions.