The Spanish economy endures

Geopolitical instability complicates the macroeconomic scenario, while economic activity indicators point to dynamic growth in Q1. Where the impact of the conflict in the Middle East and the government's measures is most evident is in the rise in inflation. The reduction of the budget deficit in recent years helps to face the new shock, and the relatively low levels of indebtedness is another distinguishing factor compared to previous crises. Employment remained robust in March.

Geopolitical instability complicates the macroeconomic scenario

The complex international context of recent years has once again been shaken by the war in the Middle East, accentuating the downside risks to our scenario, particularly due to the rising cost of energy. Although it is still early to assess its impact on the economy, given the significant uncertainty about its duration and scope, we are facing the situation from a relatively favourable starting point: the Spanish economy showed very robust dynamics at the end of 2025, which led us to revise our GDP growth forecast for 2026 upwards to 2.4% in February, prior to the outbreak of the crisis. Furthermore, the economic activity indicators for Q1 have remained buoyant. Added to this is the reduction of the budget deficit and of external indebtedness in recent years – distinguishing factors compared to previous crises.

At CaixaBank Research, we estimate that if the rise in energy costs is temporary and moderate, in line with what oil and gas futures indicated during the month of March, then the growth forecasts for the Spanish economy would only be weakened by a few percentage points. Even so, the impact would not be uniform across the entire economy, with energy-intensive industry and the transport and agrifood sectors being the hardest hit. The effect would be less pronounced than in the euro area, given Spain’s lower dependence on energy flows originating in the Middle East (around 5% of the oil and less than 2% of the liquefied natural gas arriving in Spain passes through the Strait of Hormuz) and the greater weight of renewables in the energy mix. Additionally, to mitigate the effects of the crisis, the government has approved a package of measures valued at around 5 billion euros, which includes tax reductions on fuels, gas, and electricity production, as well as direct aid to sectors and households (see the Focus «The crisis in Iran: how much could it affect the Spanish economy?» in this same report). In any case, it will be necessary to closely monitor how the conflict develops, whether the war is resolved quickly or becomes prolonged and, above all, the severity of the damage caused to energy infrastructure.

Economic activity indicators point to dynamic growth in Q1

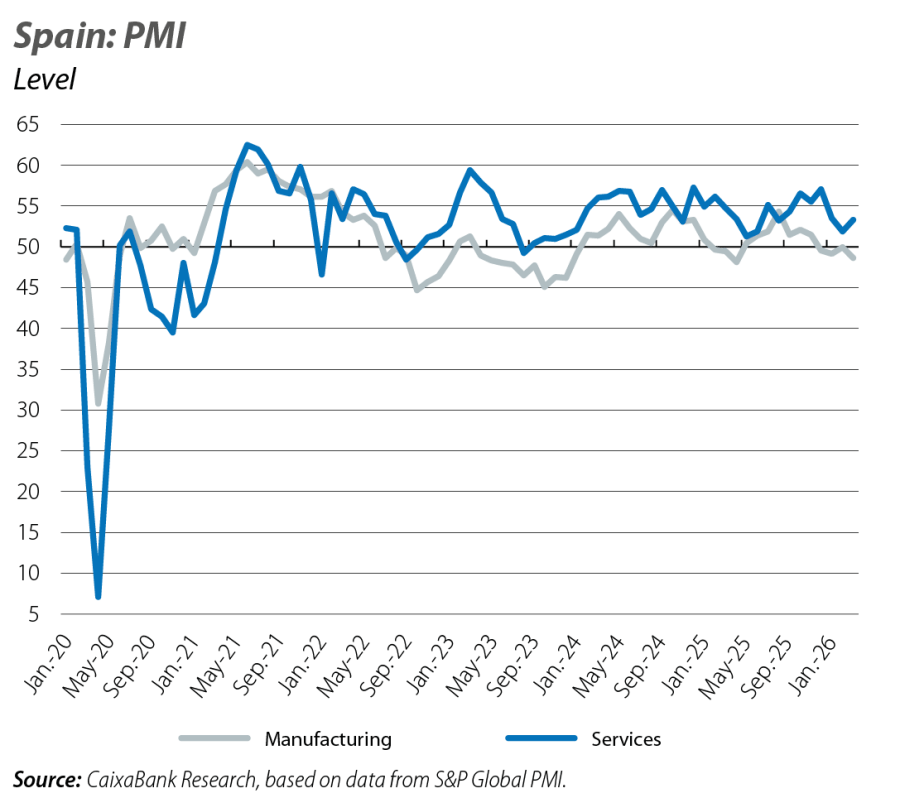

Adverse weather conditions and disruptions to rail traffic hampered economic activity at the start of the year, but it has gradually picked up and the quarter ended up closing with dynamic growth. On the services side, the PMI index rebounded in March to 53.3 points, offsetting much of the decline experienced in February: it stands 3.5 points below the previous quarter’s level, but still indicates notable growth in the sector (above 50 points marks expansion). The manufacturing PMI, for its part, fell by 1.8 points on average in Q1 compared to Q4 2024, reaching 49.3 points, indicating a potential decline in the industrial sector driven by increasing uncertainty. On the consumption side, retail sales excluding service stations, in volume and seasonally adjusted terms, fell by 0.4% in January-February compared to the average for Q4 2025, marking the first decline since Q1 2023. However, the CaixaBank Research Consumption Tracker, with data for the entire quarter, grew 3.5% year-on-year. This falls short of the 4.6% recorded in the previous quarter, although the monthly profile is particularly revealing: in January it grew by a robust 4.0%; in February it plummeted to 1.8%, largely due to the bad weather in the first half of the month; and in March it rebounded to 4.7%. Overall, the available indicators suggest GDP growth in Q1 of around 0.4%-0.5% quarter-on-quarter.

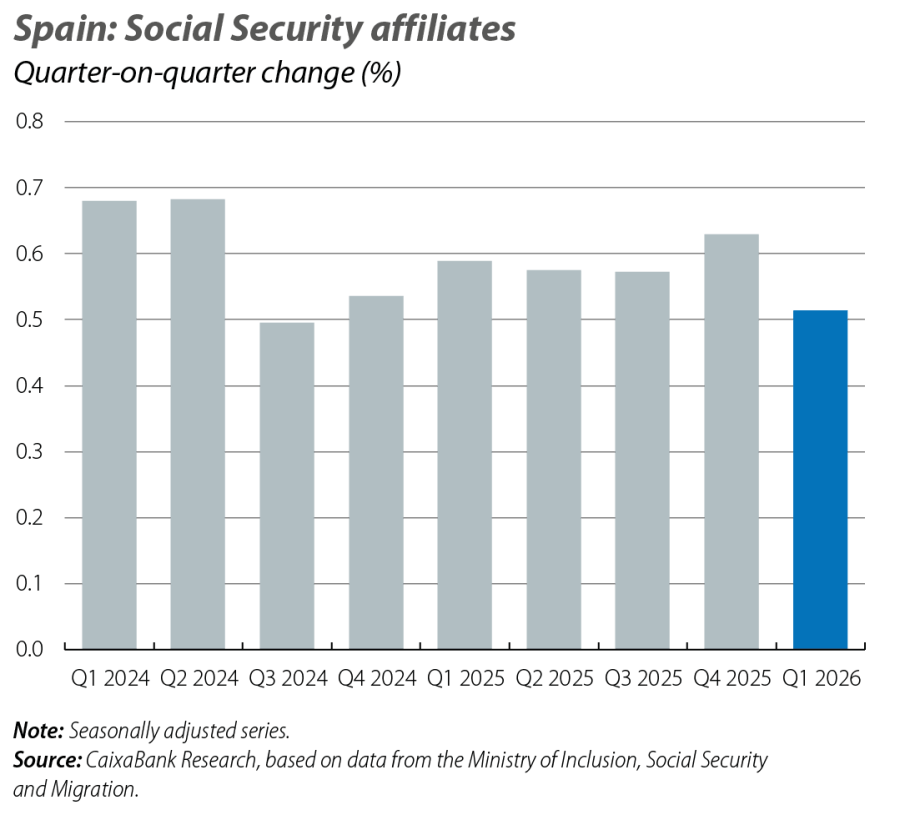

Employment remains robust in March

The number of Social Security affiliates increased by 211,511 people in March (0.98% month-on-month), slightly above the usual growth for this month in recent years (0.91% on average in 2023-2025). Thus, in Q1 as a whole, affiliation in seasonally adjusted terms registered a slight deceleration of 0.1 pp in its growth rate, placing it at 0.5% quarter-on-quarter.

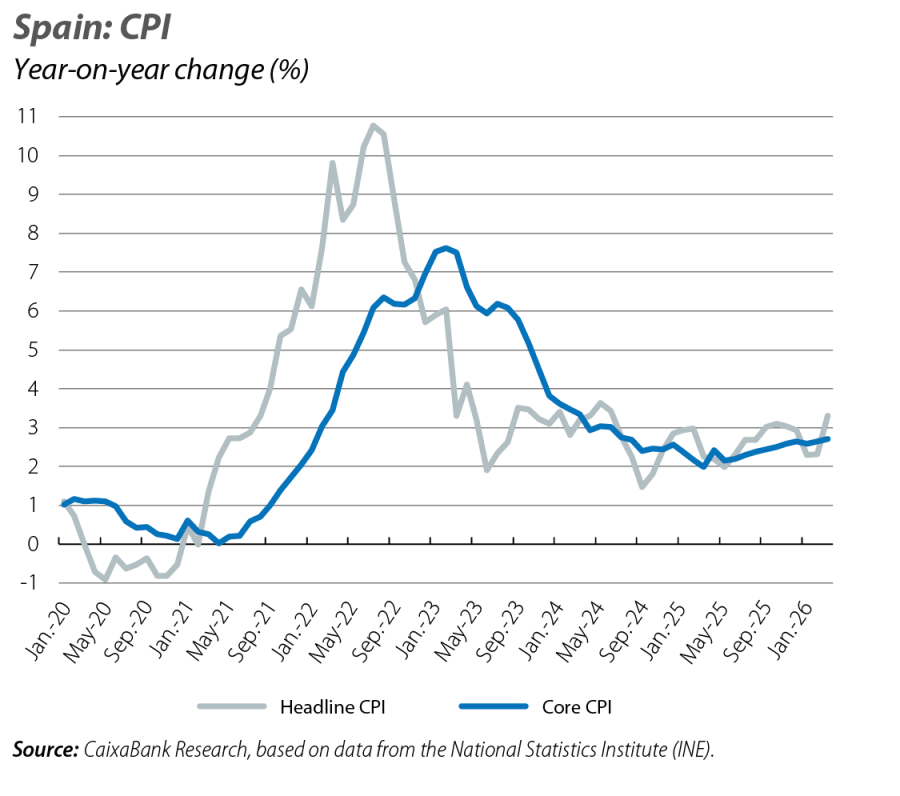

Where the impact of the conflict in the Middle East and the government’s measures is most evident is in the rise in inflation

According to the CPI flash estimate, headline inflation stood at 3.3% in March, 1 point higher than the previous month. However, the rebound would have been even greater without the measures adopted by the government, approaching 4.0%. Core inflation, which excludes energy prices, remained at 2.7%, but if the conflict is prolonged and the pressures on energy costs persist, it could also be affected. The rise in energy prices introduces upside risks to our inflation forecast. The forecast scenario anticipates an inflation rate of 2.4% for the year as a whole, but it could be around 3% if oil and gas prices follow the pattern anticipated during March by the futures markets, although the recently announced truce, if consolidated, could moderate the extent of the increase.

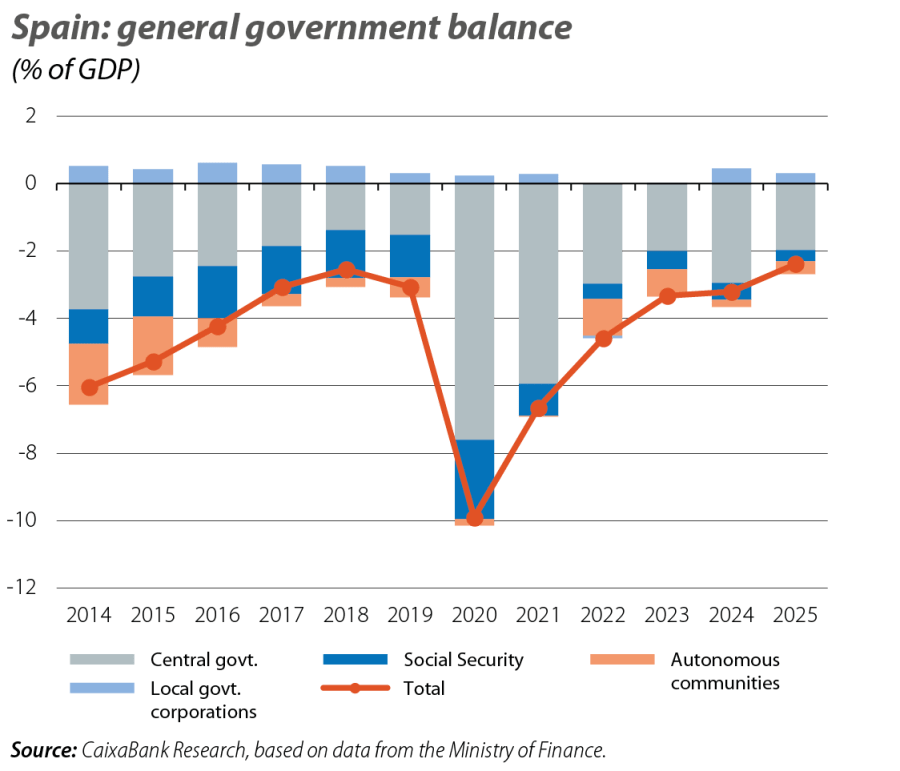

The reduction of the budget deficit in recent years helps to face the new shock

The general government deficit stood at 40.33 billion euros in 2025 (2.4% of GDP), which is 0.8 pps less than the previous year and the best figure since 2007. In this way, the deficit improved on the government’s target by 0.1 pp. If we exclude the budgetary impact derived from the floods in Valencia, which does not count in terms of the European fiscal rules, then the deficit decreases from 2.9% to 2.2%.

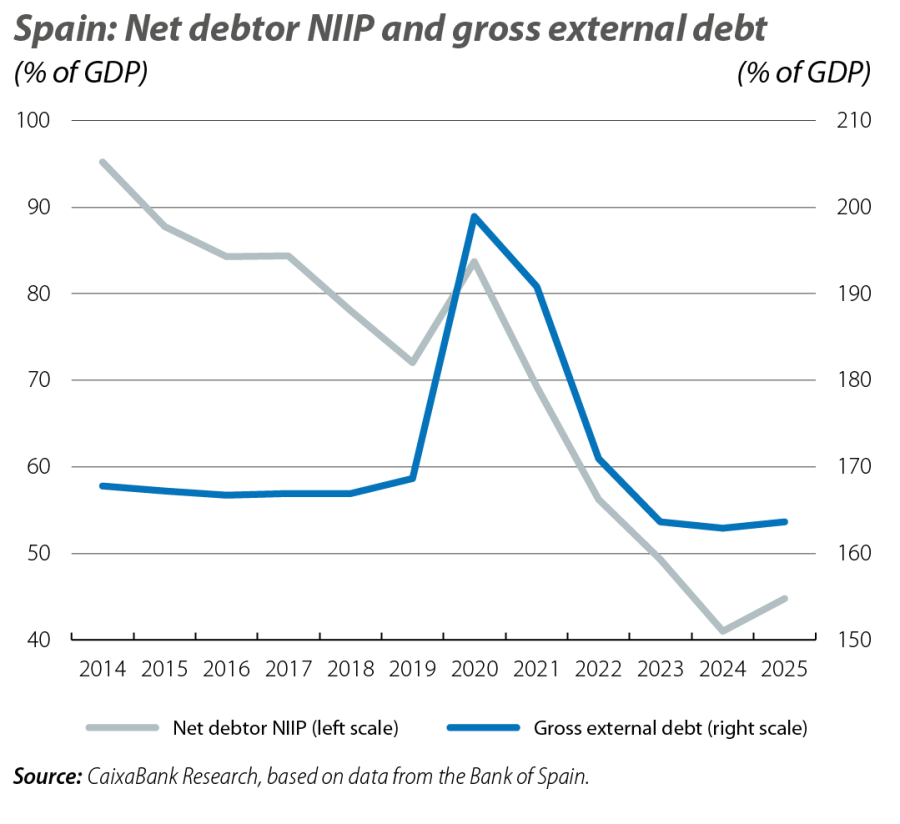

External indebtedness remains relatively low and is another distinguishing factor compared to previous crises

The deficit of the net international investment position (NIIP, referring to the balance of financial assets and liabilities vis-à-vis the rest of the world) increased by 3.8 pps in 2025, reaching 44.8% of GDP. Nevertheless, it remains low compared with previous years (–83.6% on average in 2014-2019) and far from the historical peak of 2009 (–97.2%). The deterioration was exclusively the result of a negative valuation effect, linked to prices and the exchange rate (the increase in value and the appreciation of the euro impacted liabilities more than assets), while net financial transactions were positive (assets increased more than liabilities). Gross external debt (the balance of liabilities that generate future payment obligations) increased slightly to 163.6% of GDP (162.9% in 2024), although it remains below the 2019 level (168.6%).