The Spanish economy: between resilience and slowdown

The Spanish economy closed 2025 with solid growth and has kicked off 2026 with figures that remain strong, albeit somewhat lower than those of last year. Together, the indicators published to date are consistent with CaixaBank Research’s forecast scenario, set out in the Focus «The Spanish economy in 2026» in this same Monthly Report, which anticipates GDP growth of 2.4% for this year. This allows the economy to tackle the potential consequences of the war that has erupted in the Middle East from a somewhat more comfortable position compared to other economies, but it is still too early to assess the consequences it could have. These will largely depend on the duration of the conflict and its impact on energy prices, trade routes and, ultimately, on global financial conditions and agents’ confidence. Right now, the risks are clearly skewed to the downside.

The Spanish economy closed 2025 with solid growth and has kicked off 2026 with figures that remain strong, albeit somewhat lower than those of last year. Together, the indicators published to date are consistent with CaixaBank Research’s forecast scenario, set out in the Focus «The Spanish economy in 2026» in this same Monthly Report, which anticipates GDP growth of 2.4% for this year. This allows the economy to tackle the potential consequences of the war that has erupted in the Middle East from a somewhat more comfortable position compared to other economies, but it is still too early to assess the consequences it could have. These will largely depend on the duration of the conflict and its impact on energy prices, trade routes and, ultimately, on global financial conditions and agents’ confidence. Right now, the risks are clearly skewed to the downside.

Consumption and employment on the rise

The available indicators for Q1 show an economy that remains resilient, especially in the face of the bad weather that has affected several regions at the start of the year. On one hand, the CaixaBank Research Consumption Tracker reflects the impact of the adverse weather during the first few weeks of February, although the latest data already show a clear improvement. Thus, while in the first fortnight of the month consumer spending barely grew in year-on-year terms, in the second week, it gained momentum and increased by an average of 3.2%. For reference, in Q4 2025, the growth rate stood at 4.6%. Beyond the aggregate figures, it is worth noting that the slowdown was concentrated in fashion, transport, and leisure and hospitality, while spending in other categories has rebounded.

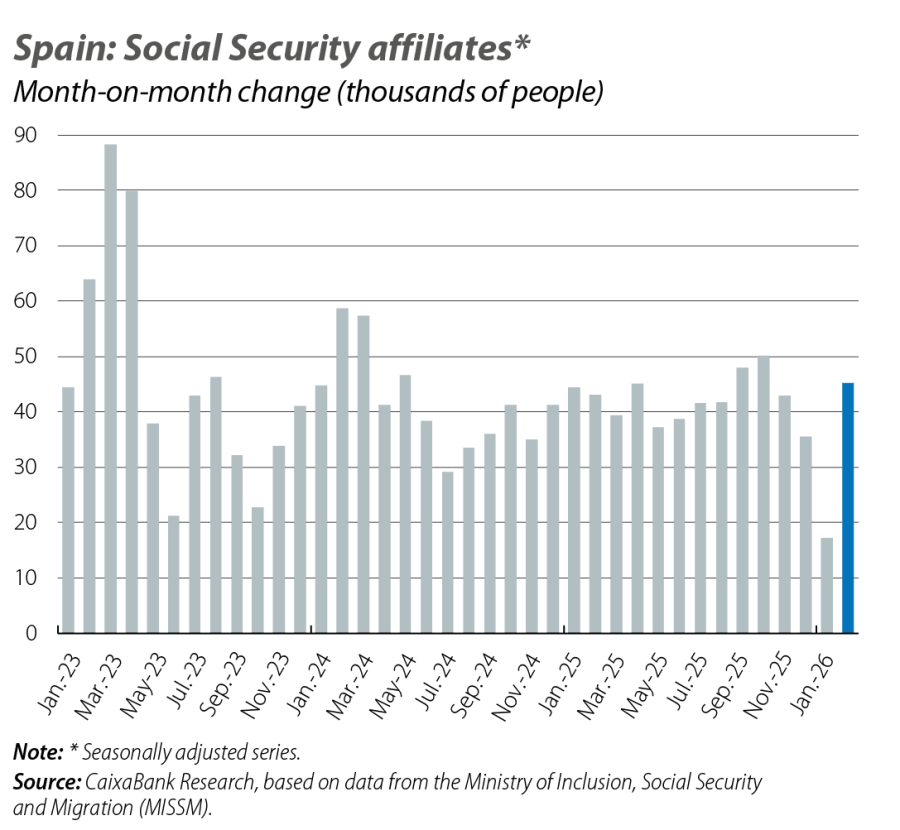

The labour market has also shown improvement at the start of the year. In January, the rate of job creation was just 17,000 social security affiliates in month-on-month and seasonally adjusted terms, far from the 42,000 recorded on average in 2025. In contrast, in February the increase was 45,000 affiliates, a figure consistent with the dynamic growth rate of the past year and indicating that the dip at the beginning of 2026 was temporary. In fact, in the first two months of the year, the average seasonally adjusted rate of job creation reached 31,000 affiliates per month. If this trend continues throughout the year, new registrations in 2026 would exceed approximately 375,000, only just shy of the forecast of 400,000 net affiliations, excluding the effect of the exceptional amnesty announced by the government.

Economic activity growth moderates

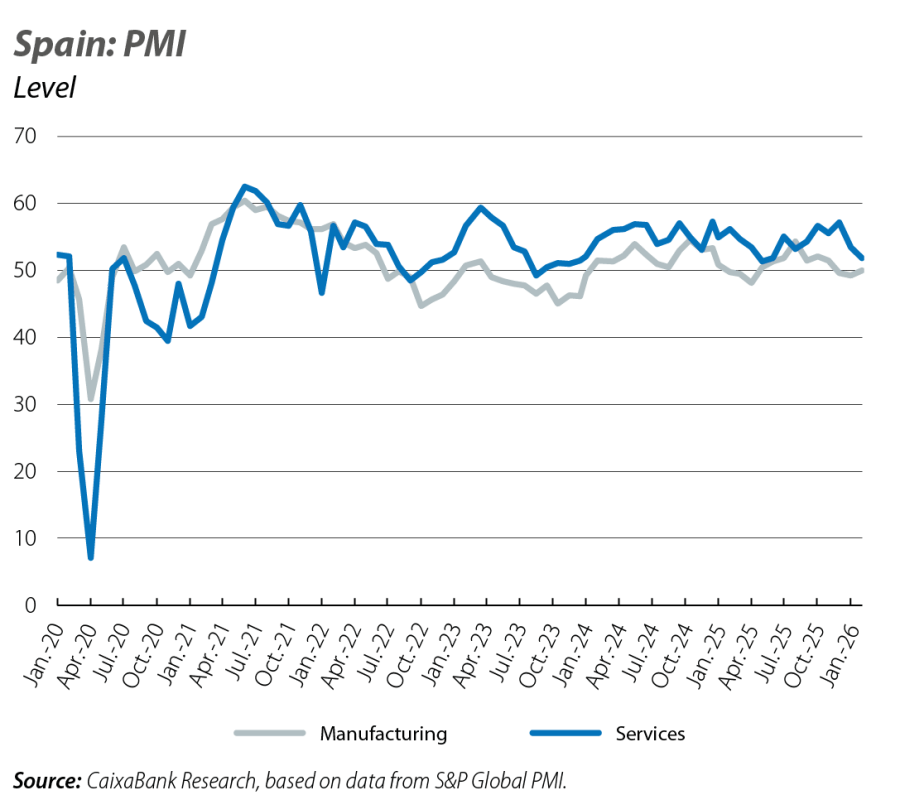

On the supply side, the PMIs also suggest that the growth rate remains positive and relatively dynamic, albeit probably somewhat more moderate. On the one hand, the manufacturing PMI appears to have bottomed out after several months of weakening, although it remains at relatively low levels. Specifically, in February it stood at 50 points, a level that typically delineates expansive territory from the contractive one, and slightly higher than the January figure. However, the average for Q1 stands at 49.6 points, well below the 51.1 points of Q4 2025. The services PMI is also weakening compared to the figures recorded at the end of 2025. In February, it stood at 51.9 points, leaving the average for the first quarter of 2026 to date at 52.7 points, well below the figures recorded at the end of 2025.

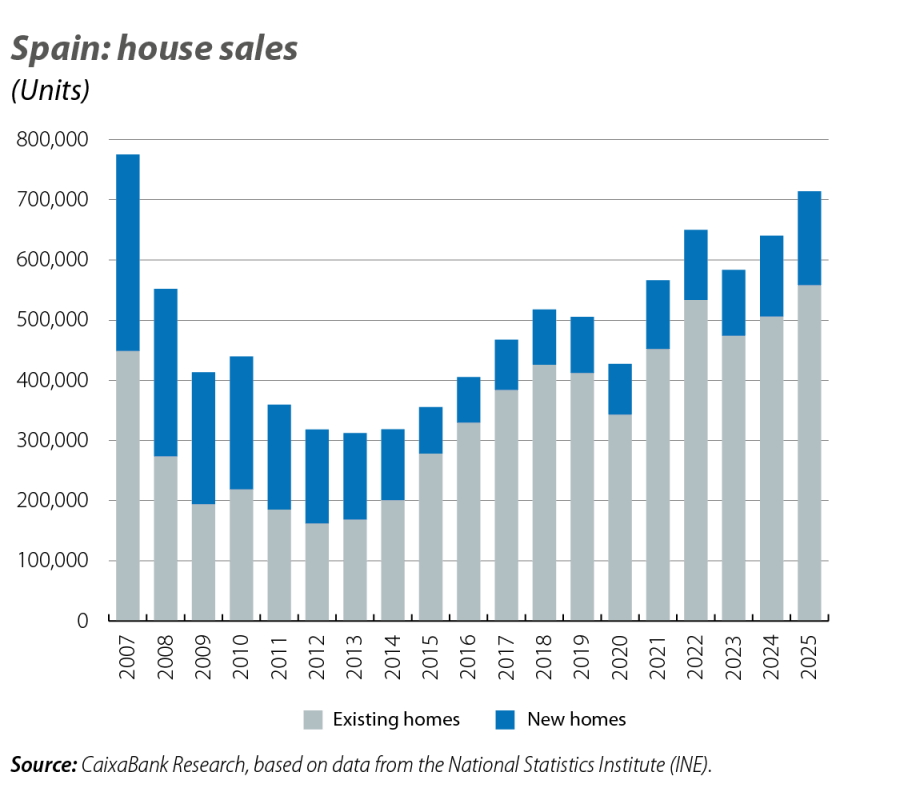

The demand for housing stabilises

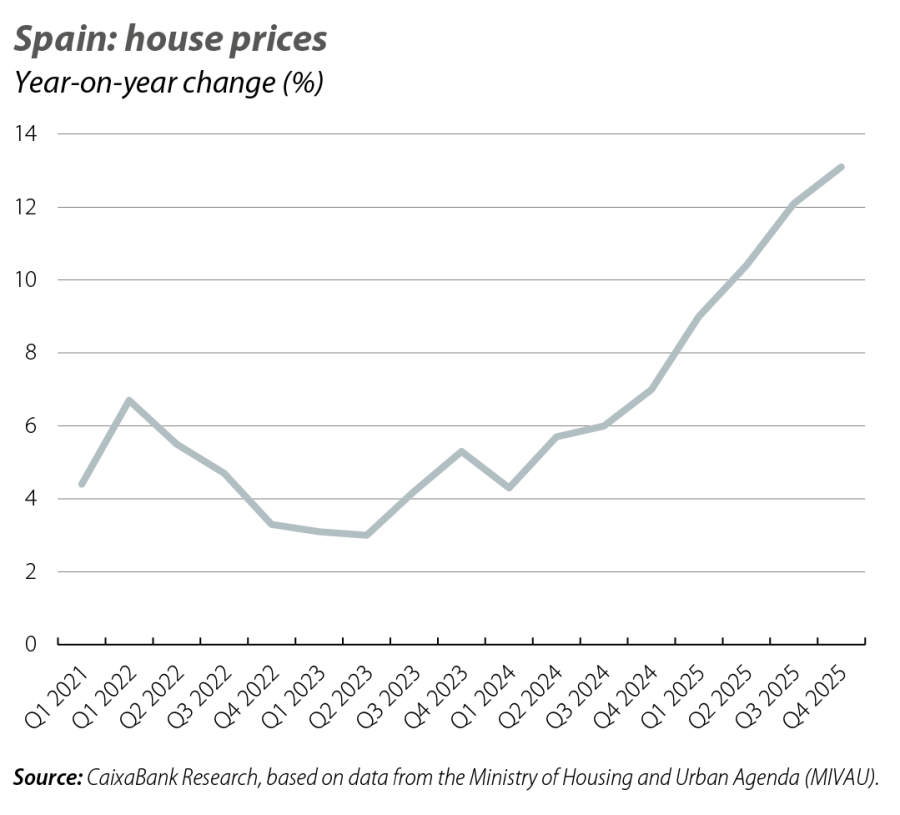

The housing market is showing a trend similar to that of other indicators: the level of activity is high, but the growth rate is losing momentum. This is reflected in the trend in sales: 2025 closed with 714,237 transactions, a historically high level (between 2014 and 2019 an average of 428,000 sales were closed per year). However, the growth rate has been weakening in recent months: during the first half of the year, the average growth in sales was 20.9% year-on-year, a figure that contrasts with the 4.5% average in the second half.

In any case, the pressure from demand continues to be reflected in prices in a context where supply is growing at a more moderate pace. The appraisal value of unsubsidised housing according to the Ministry of Housing and Urban Agenda (MIVAU) rose by 13.1% year-on-year in Q4, the largest increase of the current cycle. Although prices are reaching new nominal highs, in real terms they remain 25% below 2007 levels. Taken together, the recent data reinforce a scenario characterised by the structural housing deficit, which is likely to continue exerting pressure on prices.

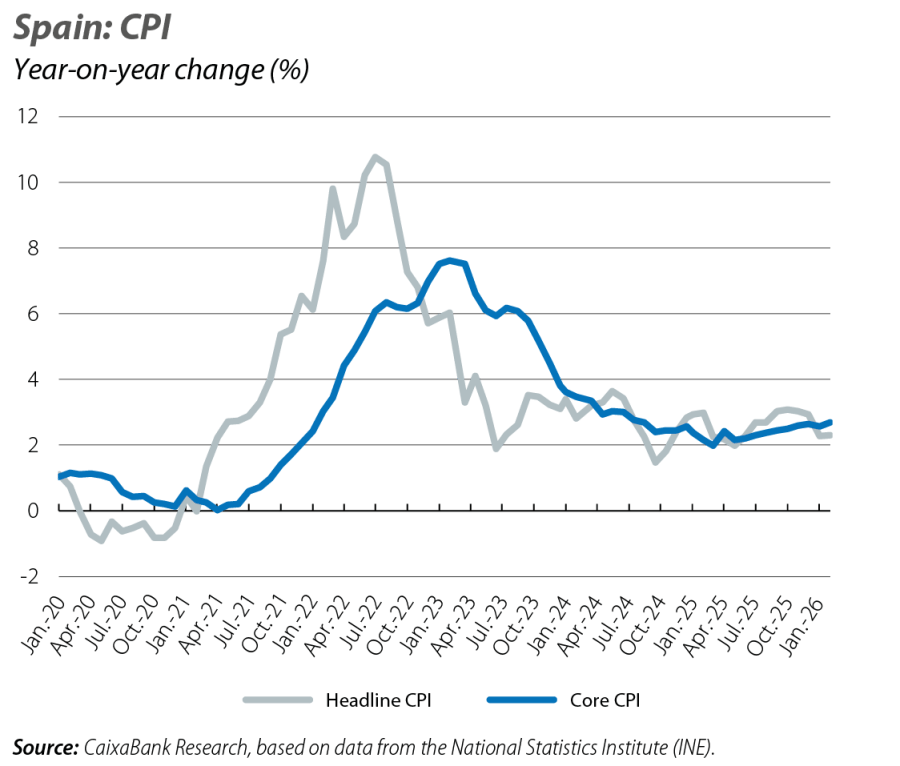

Inflation stabilises at moderate levels

The moderate slowdown of the Spanish economy is being accompanied by a reduction in inflationary pressures. In February, inflation remained at 2.3%, far from the figures of nearly 3% recorded at the end of 2025. Our forecast scenario anticipates that inflation will stabilise at levels similar to the current ones, which should help the growth of private consumption, and that of economic activity in general, to remain dynamic. However, the rise in energy prices triggered by the war that has erupted in the Middle East could reignite inflationary pressures in the coming months.

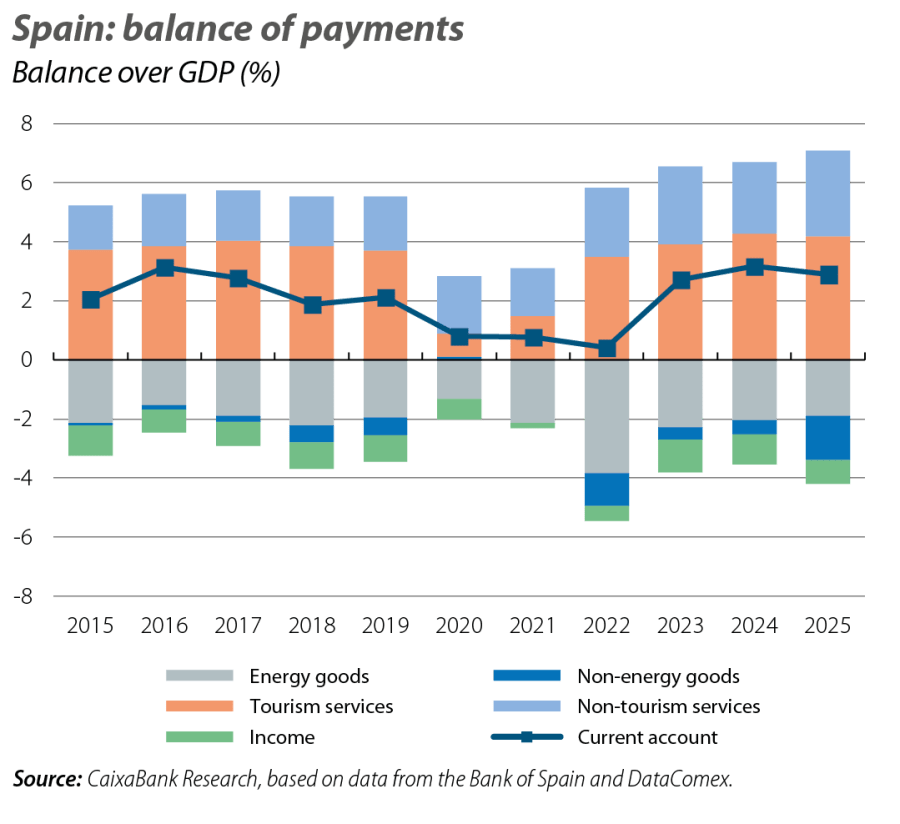

The current account holds up despite the deterioration of the international context

Despite the challenging international context, the foreign sector has remained a source of support for the Spanish economy to date. In 2025, the current account closed with a surplus of 2.9% of GDP, a level slightly below the 3.2% of the previous year, but still above the 2.3% average recorded during the period 2014-2019. Beneath this overall result lie opposing dynamics. On one hand, the trade balance deteriorated significantly in an environment marked by higher tariffs and reduced trade flows with the US. However, this deterioration was offset by the improvement in the services surplus, which reached 7.1% of GDP, thanks to the dynamism of non-tourism service exports, while the tourism surplus recorded a slight slowdown.