The US-Iran agreement alleviates adverse scenarios for the international economy

The evolution of the conflict in the Middle East remains key for the global outlook. Following the reopening of the Strait of Hormuz, the data show a somewhat erratic increase in trade flows, consistent with warnings from various international agencies that normalisation will take months. In addition, geopolitical uncertainty remains high and the complex dynamics surrounding the US-Iran agreement highlight its fragility.

The evolution of the conflict in the Middle East remains key for the global outlook

In mid-June, the US and Iran signed a Memorandum of Understanding (MoU), which is not a definitive or binding treaty, but rather a statement of intent outlining the terms of their future collaboration. The MoU marks the beginning of a 60-day period for negotiations on a range of highly sensitive issues, including Iran’s nuclear programme and the lifting of sanctions. One of the first decisions taken was to reopen the Strait of Hormuz and end the US naval blockade, providing significant relief to energy markets and reducing the likelihood of the worst-case scenarios materialising. The key will lie in how quickly trade flows passing through the Strait can recover. The data show a somewhat erratic increase in flows, consistent with warnings from various international agencies that normalisation will take months. On the other hand, geopolitical uncertainty remains high and the complex dynamics surrounding the US-Iran agreement highlight its fragility.

The peak impact of the rise in energy costs on inflation may have been in May

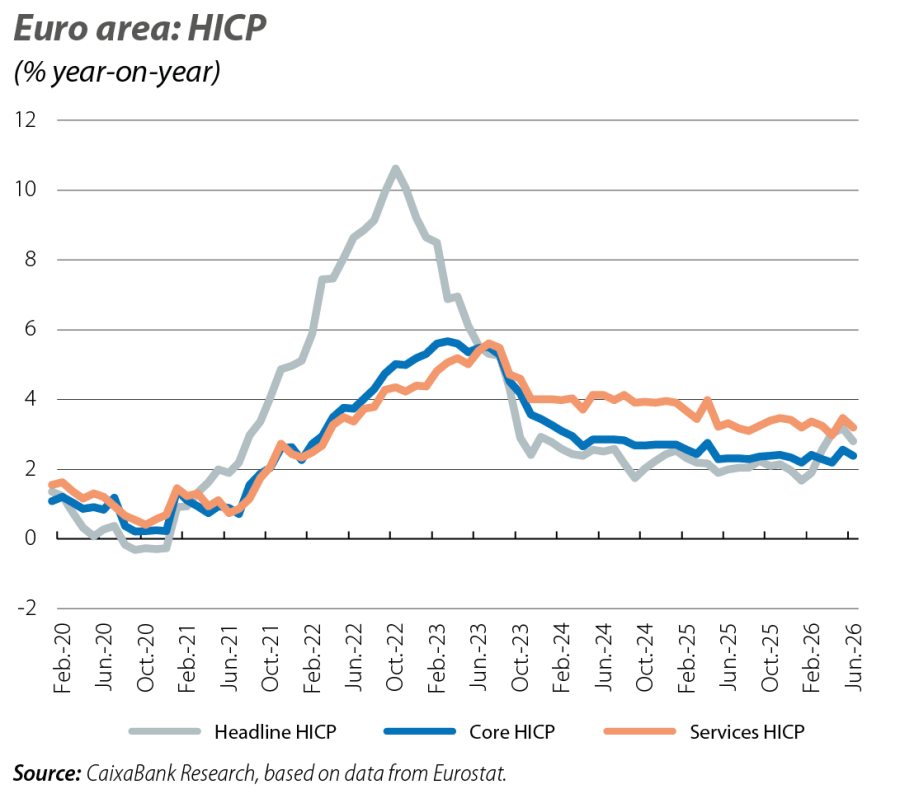

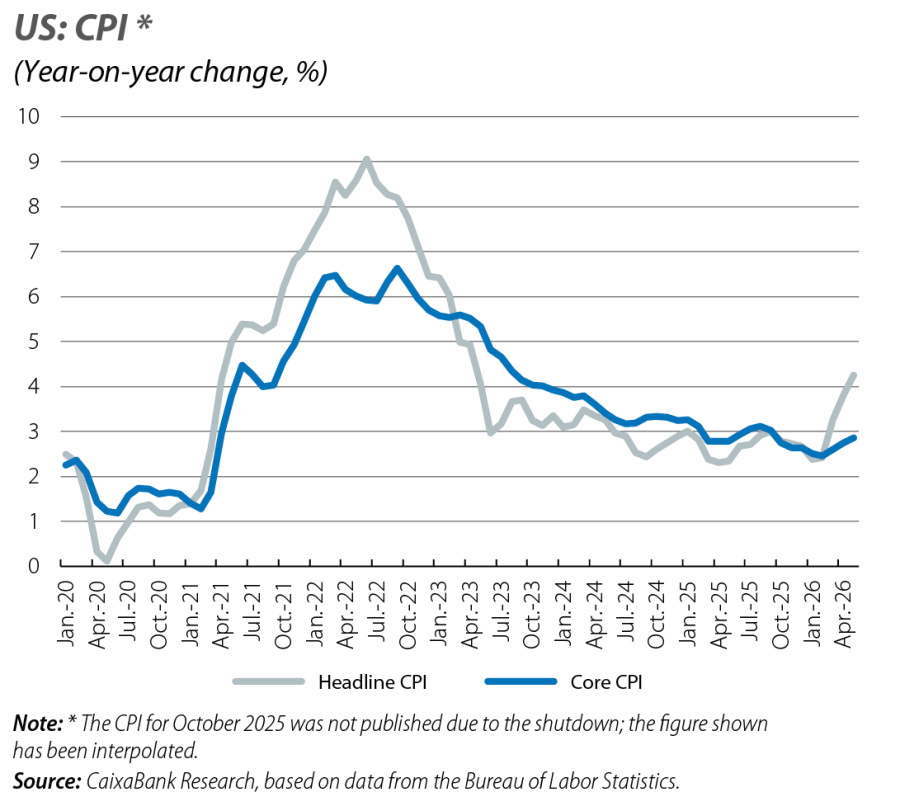

In the euro area, headline inflation reached an almost three-year high in May at 3.2%, driven by the energy component (which contributed nearly 1.0 pp). However, in June it fell by 0.4 pps to 2.8%, largely due to a slight easing in that component (–2.1 pps to 8.7%). In the US, headline inflation, driven by energy, rose by 0.4 pps in May to 4.2% (a three-year high), while core inflation was more contained (+0.1 pp to 2.9%). However, the price components of the main business climate and opinion indicators for June suggest that the peak of inflation may already be behind us.

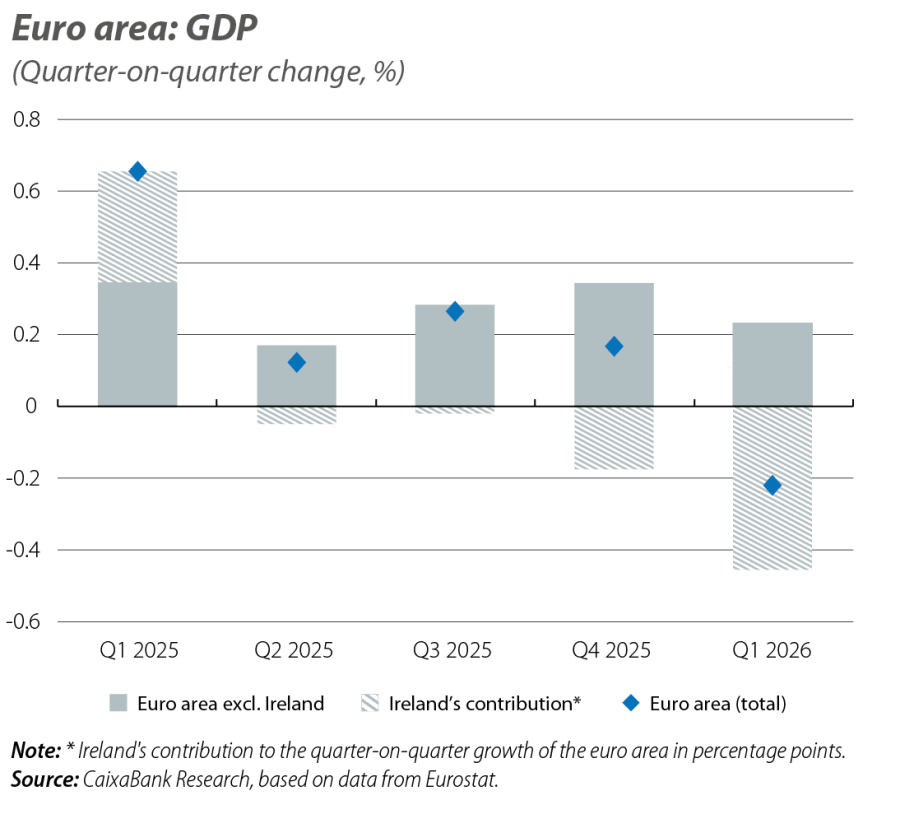

Ireland's volatility influences the euro area's performance

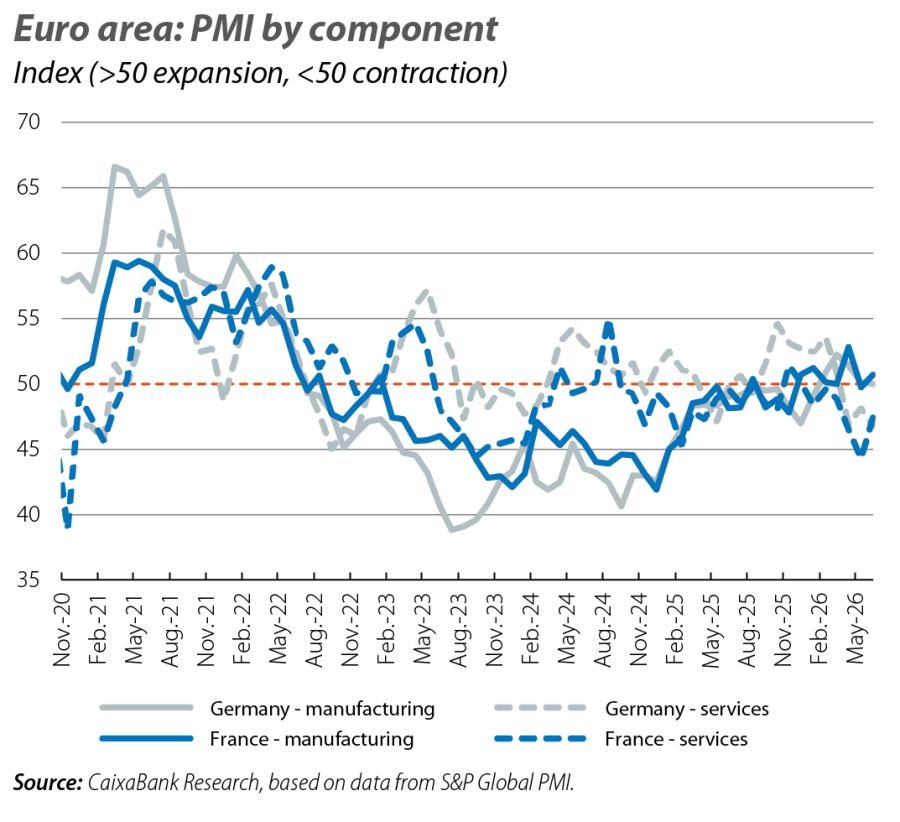

The GDP revision for the euro area shows a 0.2% quarter-on-quarter decline in Q1 2026 (vs. +0.2% per the initial estimate), explained by the collapse of the Irish economy (–12.0% vs. –2.0% initially). Without Ireland, the euro area would have grown by 0.2%, following the 0.3% recorded in Q4 2025. This is still a modest result, indicating that most of the region had not yet achieved the desired acceleration before the outbreak of the conflict in the Middle East. In this context, the available indicators for Q2 2025 suggest an economy that is practically stagnant: the PMIs for the euro area consolidated in June at levels below the 50-point threshold (and clearly below their average for Q1 2025). This was due to the deterioration in services, while the manufacturing PMI reflected how the positive impact of the increase in precautionary orders following the outbreak of war in the Middle East was beginning to dissipate.

Germany sees rising energy costs limit the impact of its infrastructure plan

In fact, the increase in energy prices is particularly impacting its industrial sector (in April, industrial production stagnated and orders fell by almost 4.0%), while household consumption remains very weak (April's retail sales are still 1.6% below their 2025 year-end level). Moreover, the implementation of the infrastructure investment plan is progressing very slowly: total accumulated federal spending to May increased by more than 3.0% year-on-year, with defence growing by 22%, but infrastructure spending was still 10% lower. Sentiment regarding Germany's performance remains rather weak, although some indicators suggest that the peak impact of the Middle East conflict may have already passed. In June, the ZEW indicates that the percentage of respondents expecting a further deterioration in the situation has almost halved (to less than 18%), while the Ifo recorded a new increase, although it remains at very low levels (85.6, with 100 being its historical average).

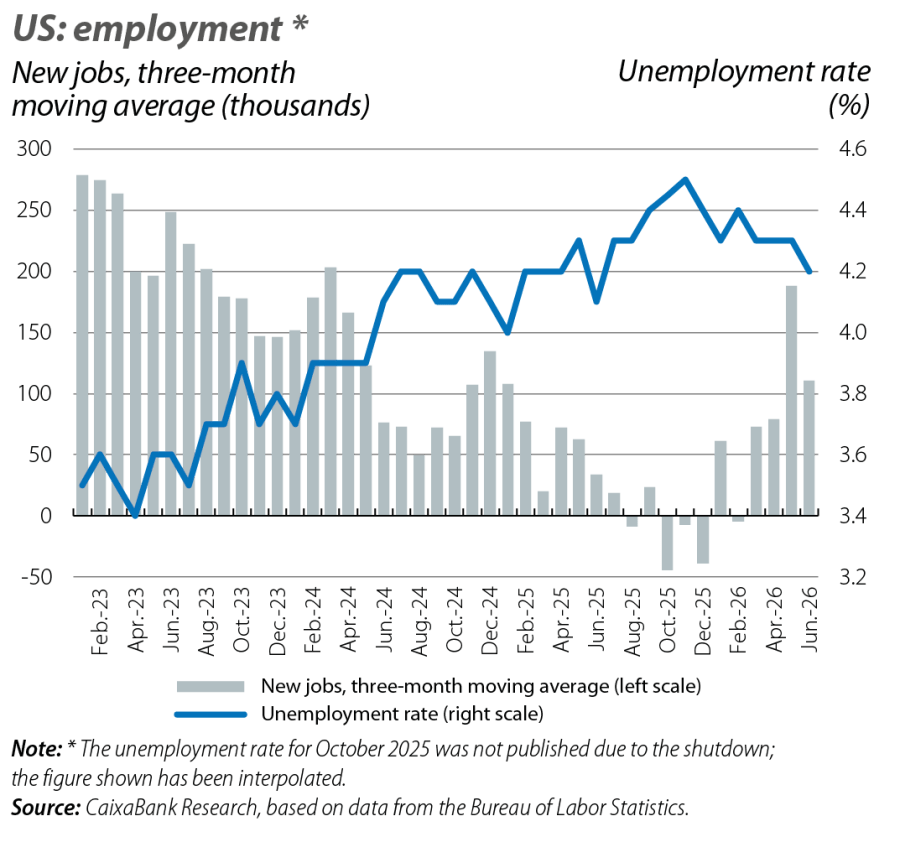

In the US, the labour market shows stability rather than recovery

In fact, 57,000 non-agricultural jobs were created in June, almost half the number expected. Additionally, the figures for the previous two months were revised downwards by more than 70,000 people. Nevertheless, average monthly job creation in 2026 exceeds 90,000, compared to less than 10,000 in 2025, and the unemployment rate fell by 0.1 pp to 4.2%. This stability in the labour market will continue to support household consumption: in May, it rose by a robust 0.7% in nominal terms and 0.3% in real terms, surpassing the average monthly growth recorded in the rest of the year (0.5% and 0.1%, respectively). Industrial production slowed in May (increasing by just 0.1% month-on-month after a previous rise of 0.9%), following several months of strong growth driven by orders being brought forward in response to the war in the Middle East.

US business leaders are more confident about the economic situation than consumers

The main business climate indicators suggest that economic growth in Q2 will have remained at similar or slightly higher rates than in Q1 (0.5% quarter-on-quarter). Specifically, the PMI for June rose to 52.2 points, placing the Q2 average at 51.8, almost the same as in Q1. The ISM indices, for both manufacturing and services, also point in the same direction, standing at around 54 points in May for both sectors (50 is the threshold indicating positive activity growth in both the PMI and the ISM). Additionally, business leaders are starting to notice signs of a moderation in the rate at which input costs are rising. This limits the risks of further rises in inflation, although it will remain high in the coming months. This increase in prices is the main factor undermining consumer confidence, amid a 0.7% year-on-year fall in real wages in May.

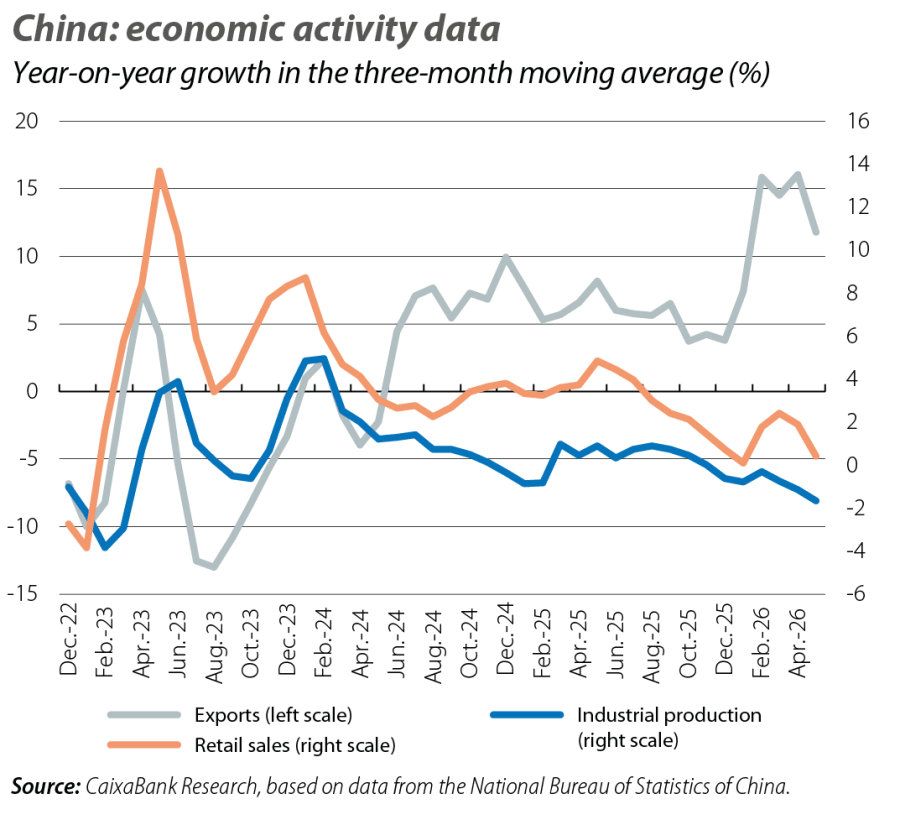

In China, the dynamism of the external sector contrasts with the persistent weakness of domestic demand

Exports in May grew by around 20% year-on-year, driven by demand for technology linked to AI and orders being brought forward, which continues to support industrial production despite a slight slowdown (+4.5% year-on-year vs. 6.0% in Q1). In contrast, retail sales fell by 0.6%, marking the first decline since the end of 2022, partly due to the withdrawal of consumer incentives. Urban fixed investment fell by 4.0% in the year to May, impacted by weakness in real estate and lower infrastructure investment. In this context, inflation remained at 1.2% and production prices reached 3.9%, the highest in nearly four years.