The global economy in search of a new balance

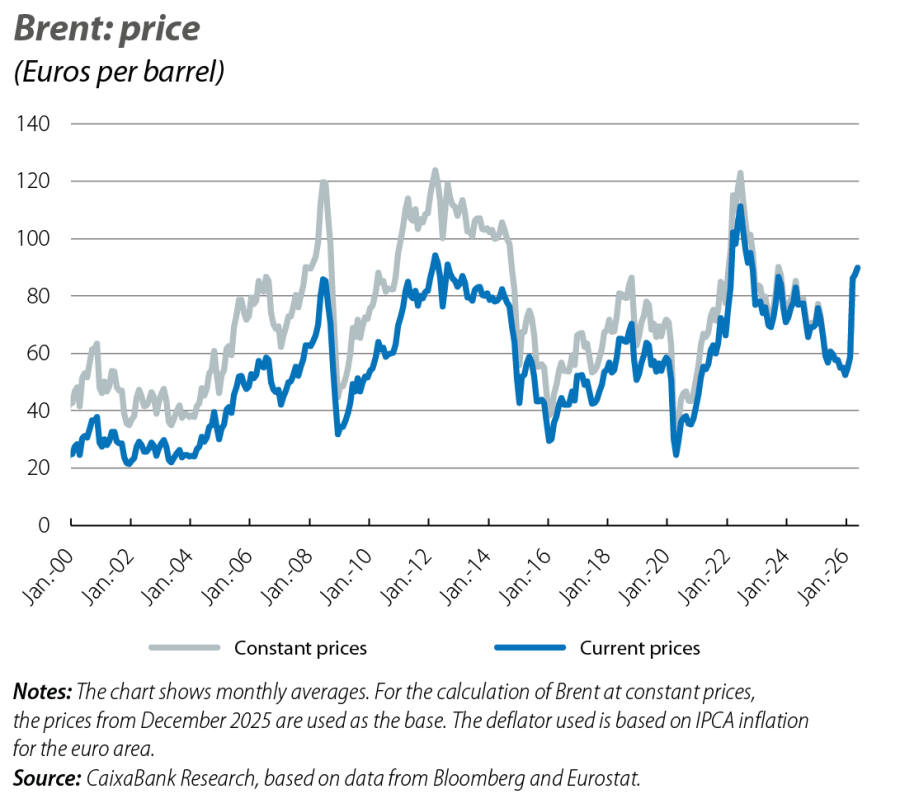

The closure of the Strait of Hormuz since the start of the conflict has driven up the oil price to around 100 dollars per barrel in recent months, while the reduction in inventories has helped absorb part of the energy shock. The indicators suggest that the energy market will remain strained and that geopolitical risk will continue to apply upward pressure on prices.

The reopening of Hormuz, a necessary but insufficient condition

The closure of the Strait of Hormuz since the start of the conflict has driven up the oil price to around 100 dollars per barrel in recent months, while the reduction in inventories has helped absorb part of the energy shock. In recent weeks, news of an extension to the ceasefire and negotiations between the US and Iran have led to a perception that the strait could soon reopen, allowing energy flows from the region to resume. However, restoring the balance between supply and demand would require a sustained increase in flows through the Strait of Hormuz, and returning inventories to their pre-conflict levels will not be quick. Overall, the indicators suggest that the energy market will remain strained and that geopolitical risk will continue to apply upward pressure on prices.

Economic activity cools in the face of a new shock

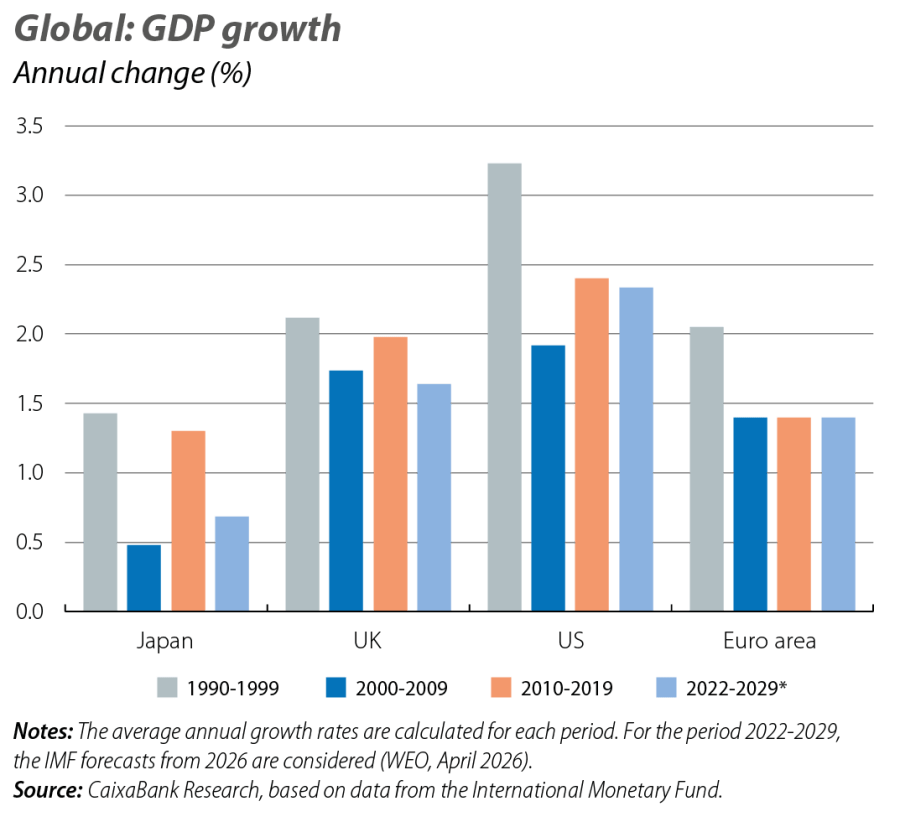

The available indicators for advanced economies point to a slowdown in activity in Q2. In the EU, the economic sentiment indicator showed a slight recovery in May (93.7 points vs. 93.4 previously), but it remains close to the lows observed in recent years and below its historical average of 100 points. Business sentiment indicators point to further deterioration. The euro area PMI fell to its lowest level in nearly three years, reaching 47.5 points (vs. 48.8 previously), weighed down primarily by weakness in the services sector (at its lowest since late 2020), amid uncertainty and rising inflation. On the manufacturing side, activity continues to hold steady, while the price subcomponents indicate an increase in production costs. In its spring report, the European Commission highlights the deteriorating macroeconomic scenario due to the conflict in the Middle East and an environment still characterised by high uncertainty, which reinforces the downside risks to growth. At CaixaBank Research, we forecast euro area growth at 0.7% for 2026 (–0.5 pps vs. our previous forecast, due to a combination of slightly lower-than-expected GDP data and the impact in the Middle East) and at 1.2% for 2027 (–0.3 pps). See the Focus «International economic outlook» in this same report.

US: focus on private consumption and the labour market

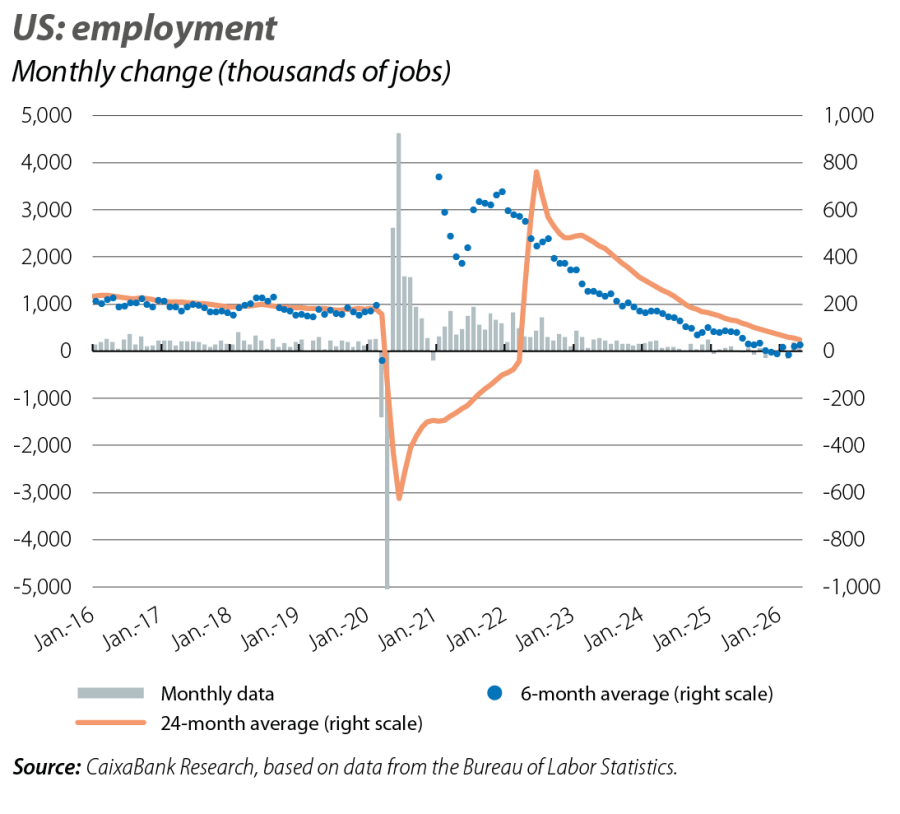

The US economy continues to withstand the impact of the energy shock, despite the deterioration in consumer confidence. Individual consumption was up 0.1% month-on-month in April (vs. 0.3% in March), constrained by weakening household purchasing power, while the labour market remained strong. The unemployment rate remained at 4.3%, while job creation stood at 115,000 people (vs. 63,000 people on average for Q1). The second GDP estimate for Q1 2026 placed growth at 0.4% quarter-on-quarter (–0.1 pps vs. the initial estimate) and indicated a more moderate increase in private consumption (+0.3% quarter-on-quarter, vs. 0.5% in Q4 2025). Fixed investment has been confirmed as the main driver of growth in the quarter. Business sentiment data have indicated levels consistent with a slight cooling of economic activity in Q2, but with positive growth rates. The composite PMI remained unchanged in May (at 51.7 points), although the price subcomponents indicate widespread inflationary pressures, reaching their highest levels since 2022.

Inflationary pressures are accelerating due to rising energy costs

Euro area headline inflation rose to 3.2% year-on-year in May (vs. 3.0% in April), while core inflation stood at 2.5% (+ 0.3 pps). The impact of rising energy prices remains visible (energy once again contributed 1 pp to headline inflation), and notable dynamics were observed in core inflation, where the upward trend in industrial goods was joined by a sharp rise in services inflation. In the absence of a detailed breakdown by component, the rebound in services could be explained by calendar effects and the indirect impact of the conflict in the Middle East on more energy-sensitive services, such as transport. In the US, the PCE, a benchmark used by the Fed, recorded an annual increase of 3.8% in April (+0.3 pps) in its headline index, while the core component was up 3.3% (+0.1 pp). This reinforces the view that the Fed will keep rate changes «on hold» until the end of the year and that the ECB could move towards a first «precautionary» rate hike as early as June (for more details, see the Focus «The financial conditions behind the economic scenario in 2026» in this report).

The United Kingdom and Japan kick off the year on a good footing, but challenges lie ahead

The UK’s GDP grew by 0.6% quarter-on-quarter in Q1 (vs. 0.2% previously), driven by the services sector and dynamic private consumption. However, the political instability following the local elections, combined with the rise in sovereign bonds and greater uncertainty about the direction of economic policy, could pose new challenges for the British economy this year. Japan’s GDP, meanwhile, grew by 0.5% quarter-on-quarter in Q1 (vs. 0.2% previously), supported by strong domestic demand and a rebound in exports. The fuel cap introduced by the Japanese government is helping to keep inflation relatively contained for now. However, the risks are clearly skewed to the upside, as indicated by the PMI price components, which are close to the levels recorded in 2022, and a strained labour market. With global inflation expectations on the rise, factors such as economic uncertainty and a potential deterioration in fiscal outlooks could increase pressure on both countries.

The outlook for emerging economies deteriorates, albeit with exceptions

In China, following a strong first quarter, activity data reveal a slowdown in April. Industrial production slowed, although it still grew at a steady pace (+4.1% year-on-year vs. 6.1% in Q1), while retail sales remained virtually stagnant. On a positive note, the strong performance of services and improved consumer confidence, in an environment in which inflation remains contained, could help sustain activity. On the other hand, Brazil’s GDP grew by 1.8% year-on-year in Q1, driven mainly by private consumption and investment. In the context of a global energy shock, these data reiterate that energy-importing economies, particularly those with greater initial vulnerabilities, could face increased risks to their growth prospects.