Survey of Household Finances: is Spain not a country for the young? (part 2, two years later)

The financial position of Spanish households has improved in aggregate terms: incomes have grown significantly, wealth continues to recover, indebtedness has decreased, and the financial burden is at a minimum. However, generational inequalities persist.

Generation gap: a persistent phenomenon in income and wealth

Two years ago, we published in our Monthly Report the Focus «Survey of Household Finances: Spain is not a country for the young», in which we analysed the evolution of differences between young Spanish households and those of other generations – the so-called generation gap – in terms of income and wealth, as well as divergences in home ownership rates and levels of indebtedness. The analysis was based on data from the 2022 Survey of Household Finances (EFF, in Spanish), conducted by the Bank of Spain.

The article documented a deterioration of the relative position of young households compared to other generations, particularly with regard to wealth. Two years on, with the ninth edition of the EFF conducted in 2024 now available, based on 6,250 household surveys that enable a characterisation of the distribution of the main income and wealth variables among Spain’s 19.5 million households, it is time to revisit those results and analyse whether our conclusions remain valid.

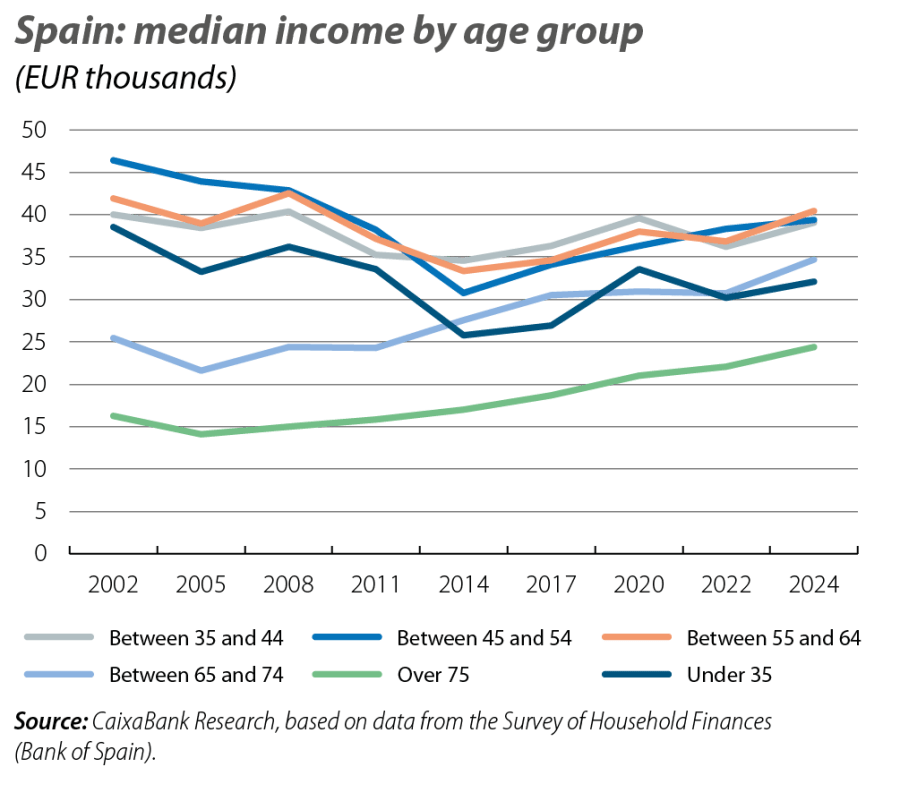

At an aggregate level, the EFF reports that the median income1 of Spanish households reached a historic high in real terms in 20232,3 (36,100 euros, at 2024 prices) and surpassed its 2001 level after growing by a notable 3.8% annually between 2021 and 2023. The median gross wealth of households has also increased, reaching 195,650 euros in 2024, after growing by 0.9% per year in real terms since 2022. It is practically at 2014 levels, albeit still far from the peak of the bubble.

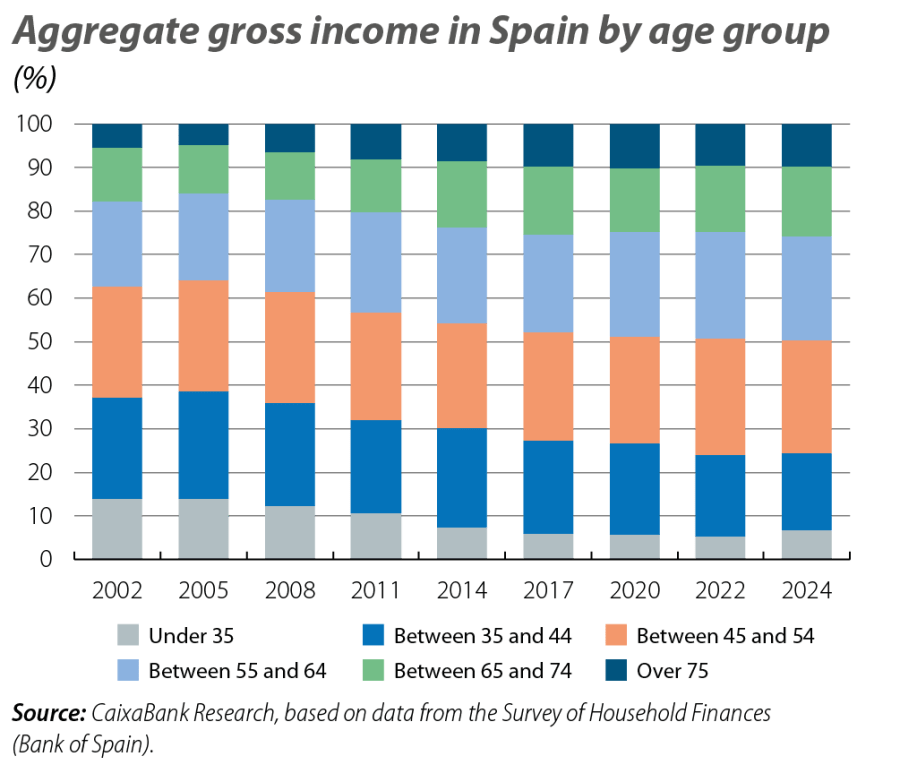

This overall trend in both income and wealth masks significant generational differences. In the more recent period, between 2021 and 2023, the gross income of young households4 (with a head of household under 35 years old) has grown at an annual rate of 3.1%, slightly below the aggregate; that of households aged 35-44 years, by 3.9%, in line with the aggregate; and that of households aged 45-54 years, by just 1.4%. In contrast, the income of households aged 65-74 has increased by a notable 6.3% annually, driven largely by the indexation of pensions to inflation.

The comparison with the previous historical income peaks – reached in 2001 – continues to reveal a marked generation gap. Only households with a head aged over 65 have managed to exceed this maximum, while those aged 35-44 have almost matched it (a decline of 2.1%). In contrast, young households and those aged 45-54 continue to have a gross income well below the 2001 level, with declines of 16.8% and 15.0%, respectively.

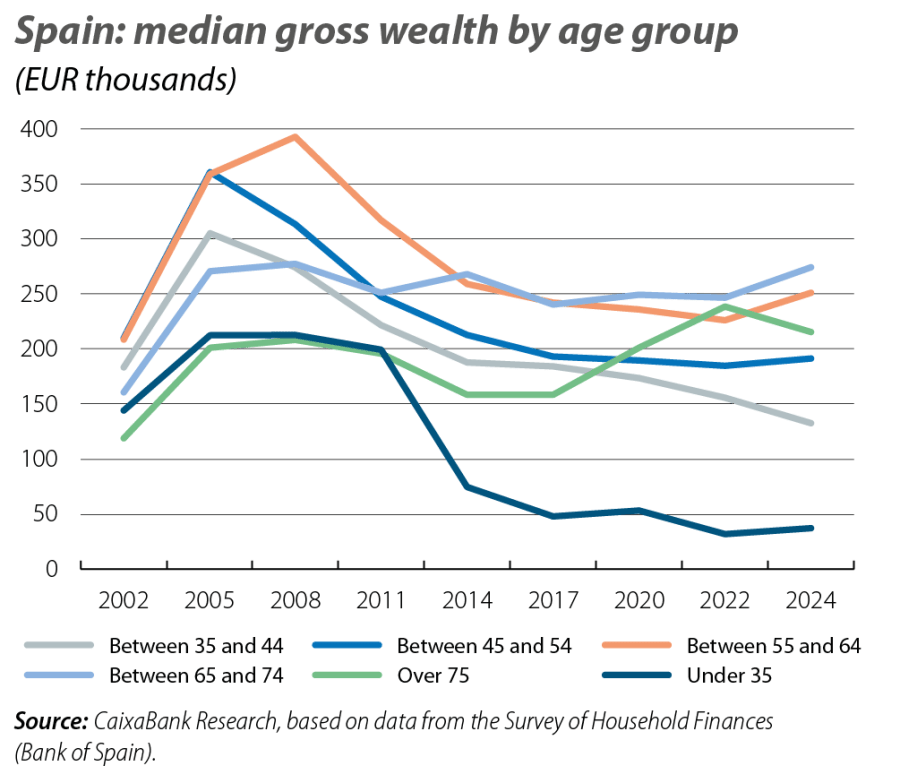

In the more recent period, from 2022 to 2024, the gross wealth of those under 35 has grown at a remarkable annual rate of 8.3%, far outpacing the aggregate rate of 0.9%. This increase has been driven by some of this group entering the housing market during a boom in the property cycle. Meanwhile, it has decreased at an annual rate of 7.9% among households aged 35-44, while it has increased by 5.4% annually among those aged 55-74.

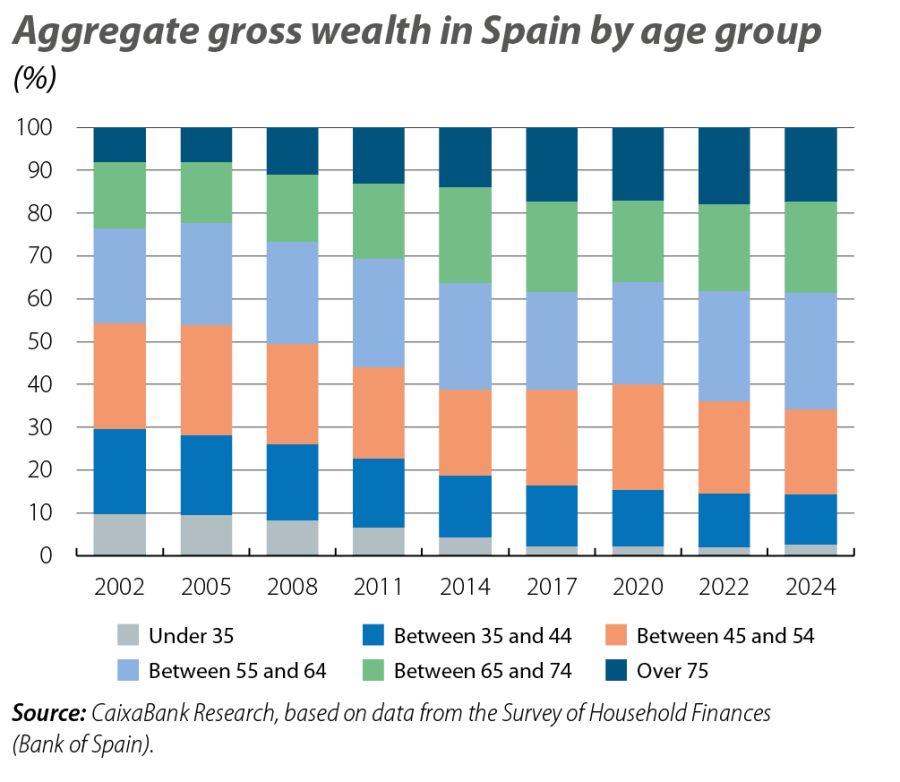

This recent growth has partially moderated the accumulated deterioration since 2014, although it remains very significant: whereas in 2022 the gross wealth of young people was 57% below the 2014 level, 5 by 2024 this gap had reduced to 50%. In comparison, in 2024, gross wealth was 29% lower than in 2014 for households aged 35-44, 10% lower for those aged 45-54, and just 3% lower for those aged 55-64. Finally – and this is where the generation gap is most evident – over the past decade, gross wealth has increased by 2.1% among households aged 65 to 74 and by a remarkable 35.9% among those over 75. Consequently, the generation gap remains significant, both in income and in wealth.

- 1

Gross income, before taxes and social security contributions.

- 2

All amounts in this article are at constant 2024 prices, i.e. adjusted for inflation.

- 3

The income data from the 2024 EFF correspond to 2023, and for previous editions they always correspond to the prior year. For financial variables, the data correspond to the year of the survey.

- 4

The household-level perspective does not include the situation of young people under 35 who have not yet formed a household (i.e. who continue to live with their parents).

- 5

If we take the years prior to the Great Recession as a benchmark, the data are distorted by the housing bubble. Therefore, the comparison is made with a benchmark from 10 years ago.

Housing, the key factor in the gap

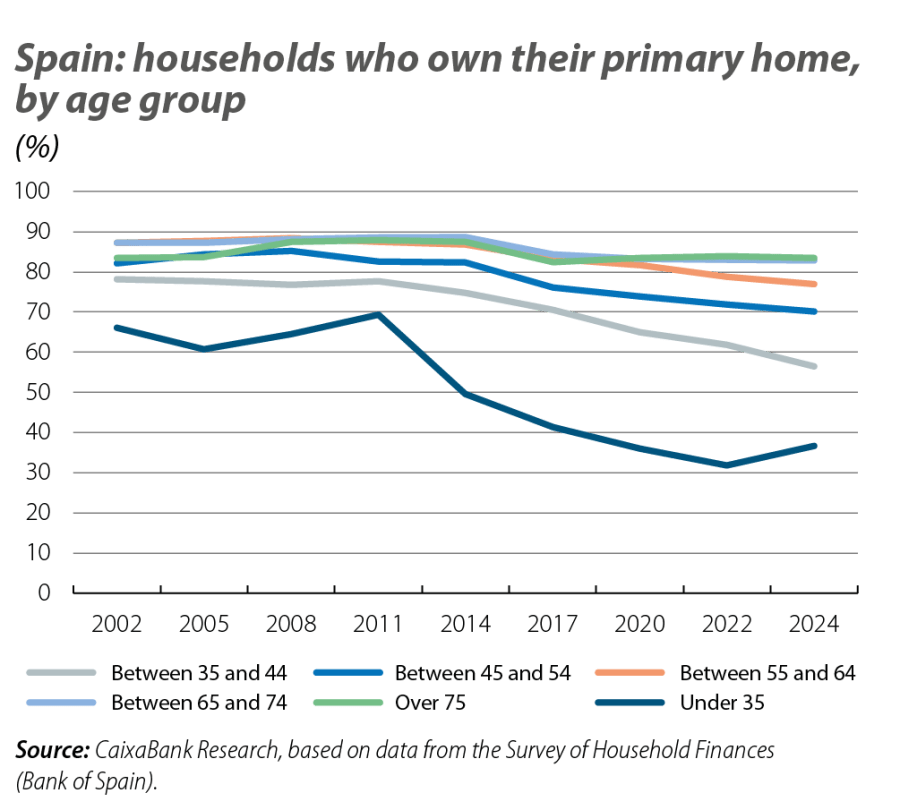

The main reason for this wealth disparity is the difficulty young people face in acquiring a home, given the importance of real estate property in household wealth in Spain. This importance is reflected in the fact that, in 2024, real estate assets accounted for 77% of the total asset value of Spanish households, compared to 23% for financial assets (80 vs. 20 in the case of young households). The proportion of households under 35 years old who own their primary residence fell from 66% in 2002 to 32% in 2022. The 2024 EFF reveals that, for the first time since 2011, this rate increased slightly, reaching around 36% in 2024 for this age group.6 Nevertheless, the level remains very low and a far cry from the 85% for those aged over 64. Interestingly, households aged between 35 and 44, belonging to the millennial generation, saw their ownership rate decrease from 62% to 56% between 2022 and 2024, far below the 78% recorded in 2002. Not owning a home – the main asset of household wealth – means that young people accumulate much less wealth. On the other hand, since financial assets only represent a small fraction of young people’s total wealth (the median value of financial assets among those under 35 is 6,000 euros, and 10,600 euros for those aged between 35 and 44), home ownership remains the determining factor in the generational wealth gap. The percentage of young households who own products such as investment funds or shares is slightly higher than 20 years ago,7 but the amount allocated remains relatively small.

- 6

An interesting factor worthy of further study is the percentage of cases with family assistance. According to the National Notary Council, in 2025 there were 225,000 donations from parents to children, representing a 13% increase over the previous year.

- 7

Furthermore, this is the age category with the highest percentage of ownership of other classes of financial assets, including crypto. 28%

of young households own some kind of other financial assets, compared to 4% in 2022.

Young households: the percentage of young mortgage holders is increasing and the financial burden is decreasing

The EFF reveals that household deleveraging continued in 2024. The percentage of indebted households fell to 54% in 2024 (from 57% in 2022). The median balance of mortgage debt for primary residences in Spain decreased from 69,000 euros in 2022 to 64,000 euros in 2024 (51,500 euros in 2002). Conversely, there is an opposite trend among young people, as mortgage debt increased from 75,000 euros in 2022 to 85,000 euros in 2024 (64,000 euros in 2022) alongside the rise in house prices.

The percentage of young households with a mortgage leads us to draw similar conclusions to those we obtained when looking at the proportion of homeowners. In 2024, 25% of households under 35 had a mortgage (20.6% in 2022), whereas in 2002 the figure was nearly half of young people. In contrast, 28% of young households had consumer loans, very similar to the 2022 figure, and a slight increase compared to 2002 (23%).

Thanks to the reduction in debt and the increase in disposable income, the financial burden on indebted households (debt payments as a proportion of gross income) has fallen to minimal levels, despite the interest rate hikes implemented by the ECB between 2022 and 2024 in response to the rise in energy costs resulting from the war in Ukraine. The median financial burden was 13.4% of income for those in debt, and the proportion of households with high financial burdens (over 40% of their income) fell to 7.9% in 2024: both are the lowest levels in recent decades. This encouraging picture is also evident when we focus on young households with some form of debt: the financial burden for households under 35 was 12.2% in 2024 (16.7% in 2002 and 13.2% in 2022) and only around 4% of indebted young households allocate more than 40% of their income to debt repayments.

In conclusion, the 2024 EFF confirms that the financial position of Spanish households has improved in aggregate terms: incomes have grown significantly, wealth continues to recover, indebtedness has decreased, and the financial burden is at a minimum. However, generational inequalities persist. The wealth gap between young and older households – largely shaped over the past two decades by differing access to housing – remains virtually unchanged in 2024. Until an environment offering more opportunities for young people and more affordable housing is established, new generations will remain far from matching the wealth of previous ones, and Spain will continue to exhibit significant intergenerational financial gaps.

Demographics

How does demographics affect economic growth, the reallocation of the model of production, the labour market and productivity?

Inequality & inclusive growth

We analyze the causes and consequences of inequality and what policies can foster inclusive economic growth that is distributed equitably in society.