The public accounts under scrutiny: the deficit reduction this year will be limited and significant medium-term challenges emerge

At the end of April, the government submitted to the European Commission the 2026 Annual Progress Report (APR), the document which tracks progress against the 2025-2028 fiscal and structural plan to which it committed with Brussels. In this article, we analyse the state of the public finances based on the report.

The APR forecasts higher nominal GDP growth in 2026 than estimated six months ago; it has increased from the 4.3% predicted in November to the current 5.3%. This forecast works in favour of fiscal adjustment, as public revenues growing more intensely in nominal terms facilitate deficit reduction, especially if the impact of inflation is reflected quickly in revenues but with a delay in expenses (as occurred after the outbreak of the war in Ukraine). The AIReF, 1 in contrast, forecasts that nominal GDP growth will be somewhat more moderate, at 4.8%.

- 1

See the Report on 2026 Monitoring of 2025-2028 Medium-Term Structural Fiscal Plan from May 2026.

The government still aims to reduce the deficit to 2.1% of GDP this year

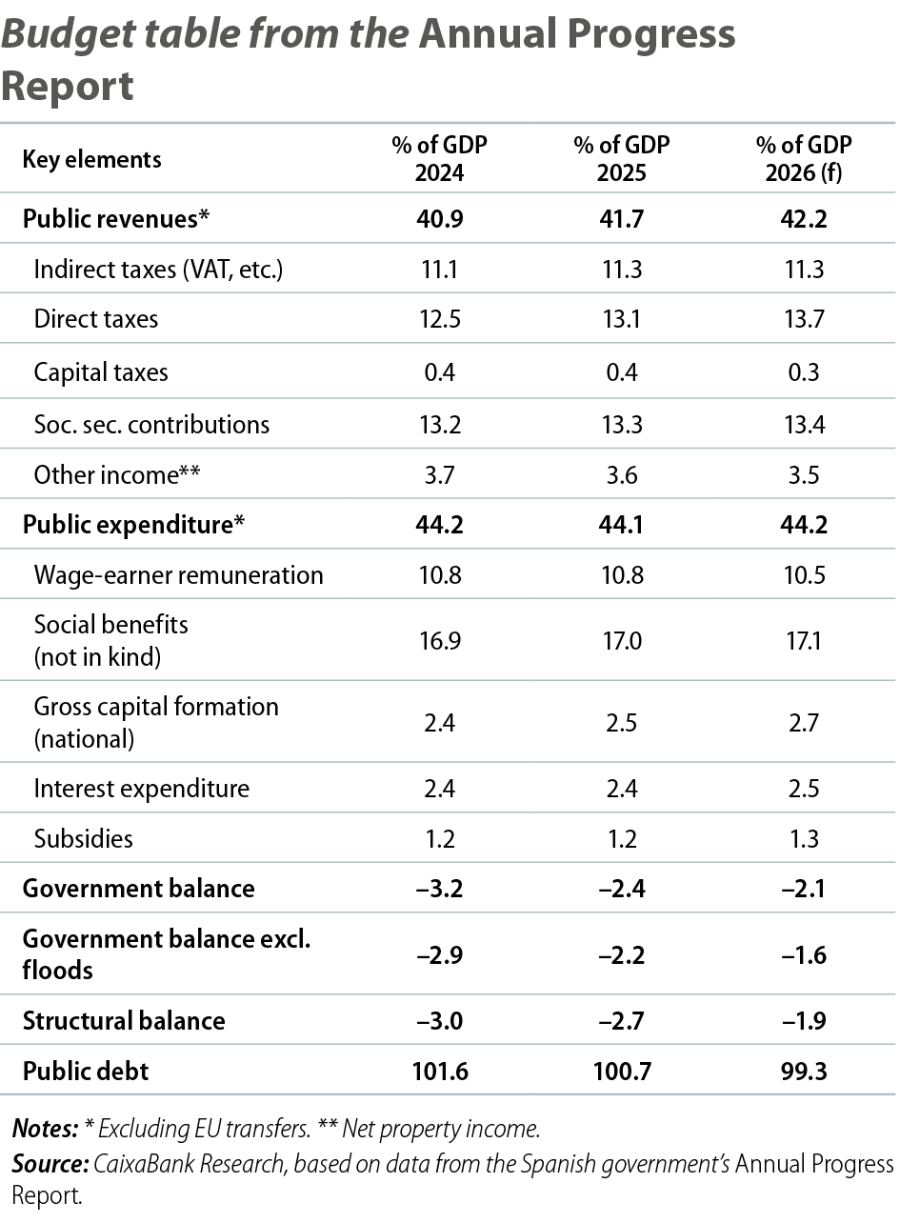

According to the APR, the public deficit is expected to decrease from 2.4% of GDP in 2025 to 2.1% in 2026. This figure includes a significant volume of exceptional expenditure: the government estimates that aid for the February storms will have a fiscal cost of 0.4% of GDP, although there is considerable uncertainty about its execution and timing. Excluding this non-recurring item, the 2026 deficit would be around 1.7% of GDP – a notable improvement compared to the 2.1% forecast in autumn. The current fiscal forecast scenario also includes energy measures intended to mitigate the economic impact of the war in the Middle East, costing around 0.25% of GDP.

The fact that the forecast for the deficit has not been revised upwards despite these unforeseen expenses is largely due to the strong results for 2025: the deficit, excluding the impact of the floods in the Valencia region, was 2.2% of GDP, compared to the initially projected 2.5%. Additionally, the 2025 deficit included 0.2% of one-off expenses related to adverse court rulings, including the income tax refunds to former members of occupational mutual insurance schemes. Another factor preventing an upward revision is the higher growth in tax revenues, especially from VAT, resulting from inflation being higher than anticipated before the war.

Overall, the APR’s scenario is more optimistic than that of the AIReF, which estimates a deficit of 2.6% of GDP in 2026 (or 2.2% excluding storm-related expenses). This difference is mainly explained by expenditure: AIReF projects an increase of 0.35% of GDP (0.1% due to higher public sector wages and the rest due to other unspecified expenses), as well as a decrease of 0.15% in tax revenues. At CaixaBank Research, we forecast a deficit of 2.3% of GDP, in between the APR and AIReF forecasts and very close to the European Commission’s estimate of 2.4%. This is consistent with nominal GDP growth of 5.1%, also midway between the forecasts of these institutions.

The APR predicts that public spending2 will remain practically flat, going from 44.1% of GDP in 2025 to 44.2% in 2026. There will, however, be changes in its composition: defence spending is expected to increase by 0.2 pps to 1.2% of GDP;3 social transfers will grow slightly above nominal GDP, and wage-earner remuneration will grow well below that level. Interest expenditure is forecast to rise from 2.4% to 2.5% of GDP, reflecting a slightly higher interest rate environment.

As for public revenues, the APR projects an increase in their share of GDP by 0.5 percentage points this year, reaching 42.2% of GDP. This increase will be smaller than that of 2025, partly due to the tax cuts implemented in response to the energy shock. Even so, revenues will remain dynamic, especially in terms of direct taxation, which is expected to increase by around 0.6% of GDP (+22 billion euros). This growth will be driven by the strength of the labour market, higher capital gains, and various tax measures, such as the non-deflation of personal income tax and the introduction of a minimum 15% corporate tax rate for multinationals. Revenue from indirect taxes is expected to grow more moderately than that of direct taxes, so its share of GDP would remain the same as in 2025.

European fiscal rules: compliance to date, but medium-term challenges

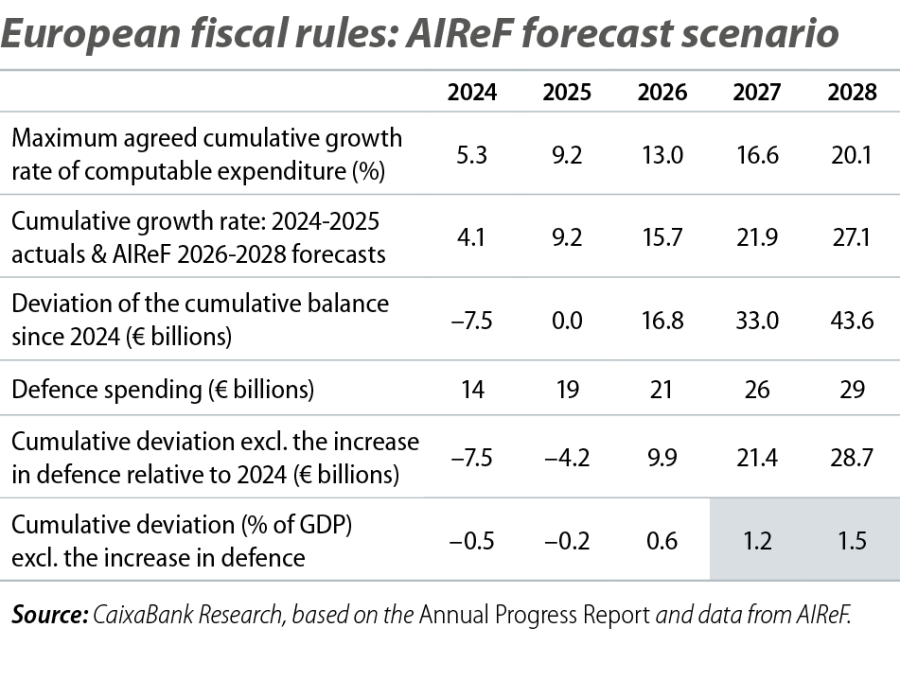

European fiscal rules focus on a spending rule. The spending rule set two years ago established a path for the maximum growth of computable primary expenditure (excluding one-offs, such as expenses associated with the floods in Valencia or other storms), 4net of revenue measures, consistent with a downward trajectory of public debt. In Spain’s case, it was agreed that an annual adjustment of at least 0.42 pps in the primary structural balance was necessary. The maximum expenditure growth path was based on the potential growth forecasts and the deflator developed in 2024, as well as the fiscal adjustment agreed to reduce the deficit and debt. It is also consistent with a sustained reduction in public debt, averaging around 1 pp of GDP per year from 2025 to 2031. The rule allows computable expenditure growth to exceed the agreed path, but only up to a limit: up to 0.3% of GDP each year and up to 0.6% of GDP cumulatively since 2024. It is important to note that the cumulative balance effectively becomes the one subject to analysis for assessing compliance with the fiscal rules. The European Commission has clarified that for countries activating the escape clause for defence spending, as Spain has just done, the focus shifts to monitoring cumulative deviations not covered by the clause itself.

Net computable expenditure grew by 4.8% year-on-year in 2025, exceeding the 3.7% limit agreed with the Commission. However, as the growth in computable expenditure in 2024 was lower than expected, the cumulative growth for 2024-2025 stood at 9.2%, exactly the percentage agreed. Thus, Spain complied with the fiscal rules in 2025.

For 2026, the APR forecasts growth in computable expenditure of 4.7% (including defence spending and subtracting tax cuts due to the conflict in Iran through new revenue measures), above the agreed 3.5%. However, AIReF has identified risks that it could reach more than 1 point higher. In cumulative terms for 2024-2026, excluding the increase in defence spending from 2024 onwards following the activation of the escape clause, expenditure growth would be 13.3%. This is slightly above the agreed level of 13.0%, but within the tolerated deviation limit of 0.6% of GDP. AIReF agrees that the limits will be respected this year. However, it warns that, in the absence of policy changes, the threshold will be exceeded by 0.6% of GDP in 2027 and by 0.9% in 2028. This would necessitate additional measures, either to boost revenues or to reduce expenditure.

Finally, public debt is expected to continue to decrease, going from 100.7% of GDP in 2025 to 99.3% in 2026, according to the APR. This improvement includes the pending disbursements of NGEU loans from the Recovery and Resilience Facility, which are equivalent to 0.4% of GDP in 2026 and will limit the pace of debt reduction.

In summary, Spain is making progress in reducing the deficit and is complying with the European rules, but with narrow margins and thanks to macroeconomic dynamism. However, the AIReF warns of risks of non-compliance from 2027 onwards.5 Therefore, in the medium term, the credibility of the fiscal strategy will depend on the ability to implement a structural adjustment in an environment with growing pressures on public spending, stemming from demographics and defence spending.

- 4

Computable expenditure includes public expenditure net of interest expenses, discretionary revenue measures, expenditure on EU programmes fully offset by income from EU funds, national expenditure on co-financing of EU-funded programmes, cyclical elements of unemployment benefit expenditure, and one-off and other temporary measures.

- 5

The government does not provide fiscal forecasts beyond 2026.