Financial markets: a disconnect between risk and energy?

The conflict in the Middle East set the pace for financial markets in a month marked by very high uncertainty and as geopolitics continued to redefine the economic landscape.

Uncertainty and risk appetite diverge in April

The conflict in the Middle East set the pace for financial markets in a month marked by very high uncertainty and as geopolitics continued to redefine the economic landscape. Despite the ceasefire, the price rally in energy and other products linked to hydrocarbons and the region (such as fertilisers and fuels) was consolidated. At the same time, central banks confirmed a shift towards a gradually more restrictive monetary policy (due to either expectations of interest rate hikes or a pause in previously anticipated cuts), causing sovereign yields to remain high. However, stock markets diverged from this trend and the main stock indices once again registered gains, spurred by renewed optimism around AI firms, the reporting of strong corporate earnings and a recovery in risk appetite.

Energy remains in distress...

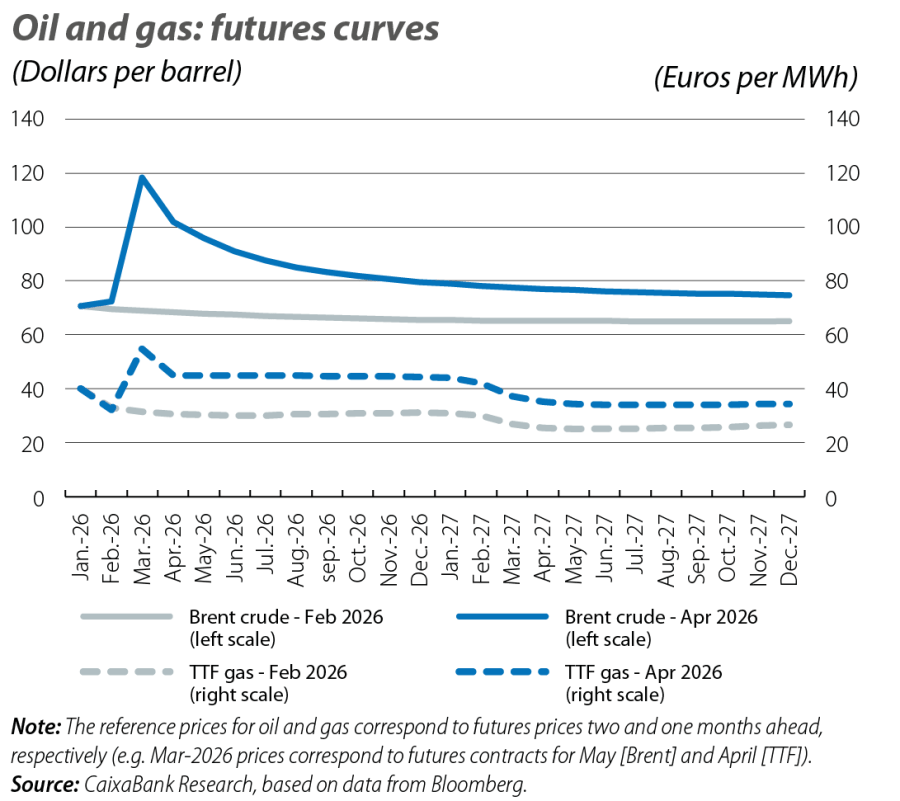

With the Strait of Hormuz closed, the International Energy Agency estimates that since March, around 10% of the global oil supply has been lost and that this decline has been cushioned mainly by previously accumulated stockpiles. The price of a barrel of Brent remained above 100 dollars for much of the past month and continued to show significant volatility, with some sessions seeing an easing of prices to just below 90 dollars per barrel while in others it exceeded 120 dollars. In the gas market, the European TTF benchmark traded in the range of 40-50 euros per MWh. For the 2026 average, futures markets continued to suggest prices at around 90 dollars per barrel of Brent and 45 euros per MWh for the TTF, 30% and 40% above pre-conflict levels, respectively. For 2027, they anticipate a moderation in prices to 75 dollars and 35 euros on average for the year (+10% vs. pre-conflict levels). Furthermore, these price tensions continued to spread to derivative products, with generic benchmarks in wholesale diesel and jet fuel markets rallying between +60% and +80% vs. pre-conflict levels. The rise in fertiliser (urea) prices was similar, with concerns that this could be passed on to food prices, which also rose in April (Bloomberg's agricultural index rose by over 3% in April and is up more than 10% in the year to date).

… and stock markets regain their risk appetite

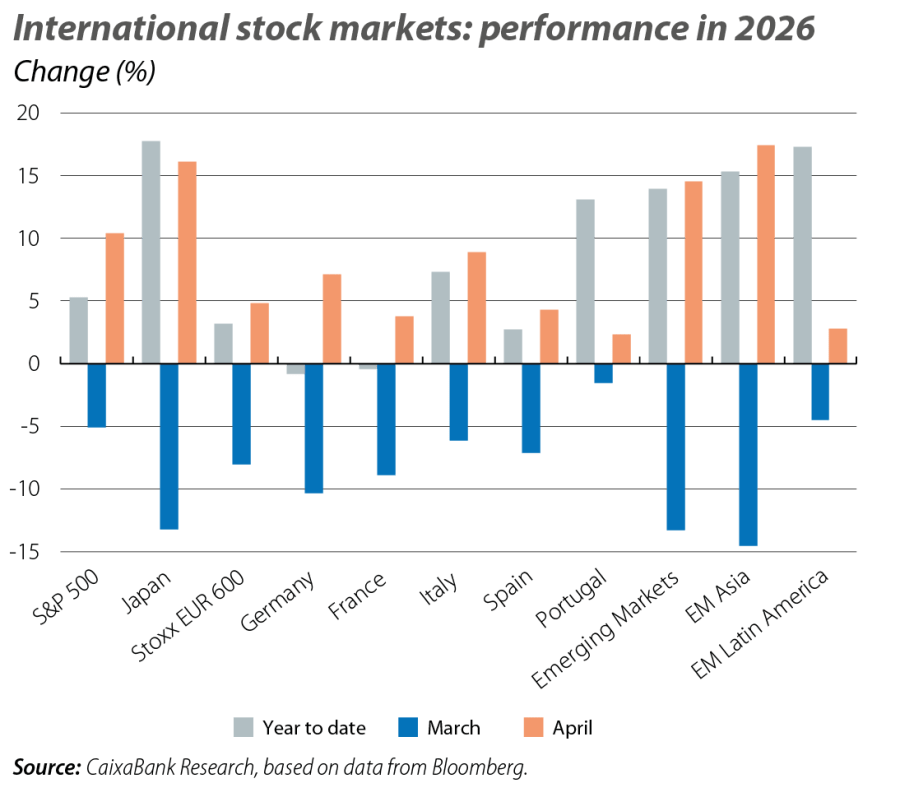

In the US, the S&P 500 reached new all-time highs thanks to the tech sector rally and the advance of cyclical sectors (consumption, industry). European stock markets also recorded a significant and widespread rebound, with the Stoxx 600 EUR returning to positive territory for the year to date. The MSCI Emerging Markets indices were also up around 15% in 2026 in both Asia and Latin America. Sentiment found support in a strong earnings season. At the close of this report, with over 60% and 50% of firms in the S&P 500 and the Stoxx 600 EUR having reported their earnings, between 70% and 80% of US firms have exceeded expectations in sales and earnings, while around 50% beat forecasts in Europe (in line with previous seasons). In parallel, analysts continue to anticipate strong earnings growth for the year ahead (of around 20% and 10% in the US and Europe, respectively).

Interest rates are consolidating at higher levels

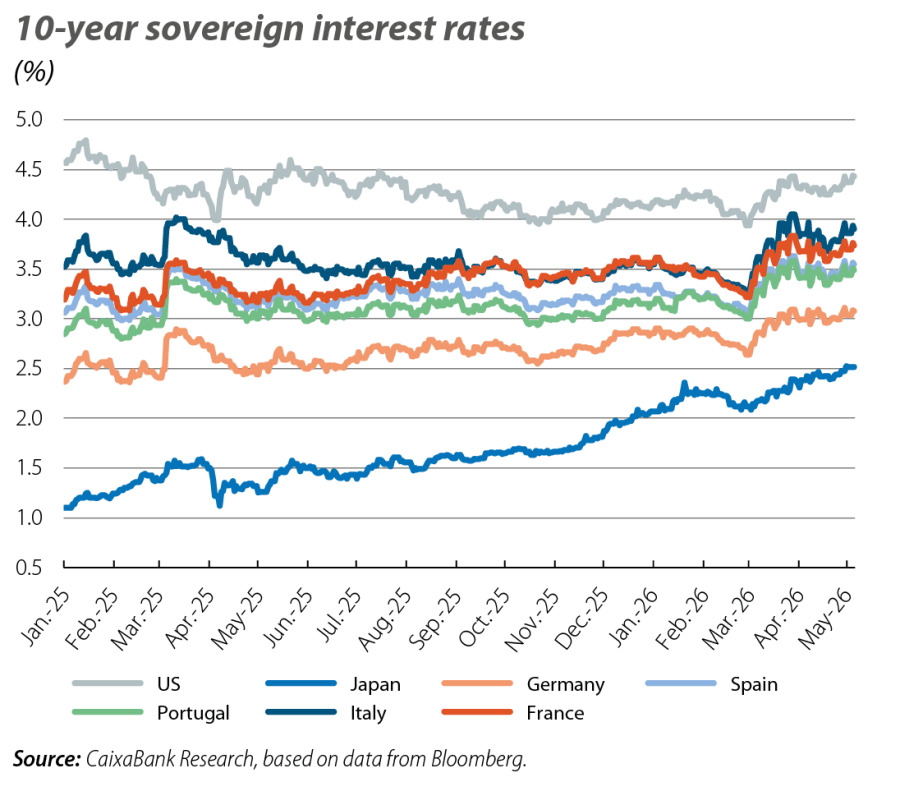

On both sides of the Atlantic, sovereign interest rates remained stressed. This was due to inflation expectations stemming from the energy shock in the Middle East (swaps were pricing in one-year inflation at around 3.5%, in both the US and the euro area), as well as the prospect of a more restrictive monetary policy than that anticipated prior to the bombings. US and German sovereign yields rose by almost 10 bps and 5 bps in the last month, with the short ends of the curves rising between 40 and 50 bps in the year to date (+20 bps at the long end). Risk premia in the periphery, in contrast, remained contained (just under 50 bps for Spain, just above 40 bps for Portugal) and Italy and France, which were initially under more strain, managed to moderately narrow their spreads relative to Germany. In the foreign exchange market, the euro regained some lost ground and appreciated to 1.17 dollars.

Change at the helm of the Fed, but no changes in rates

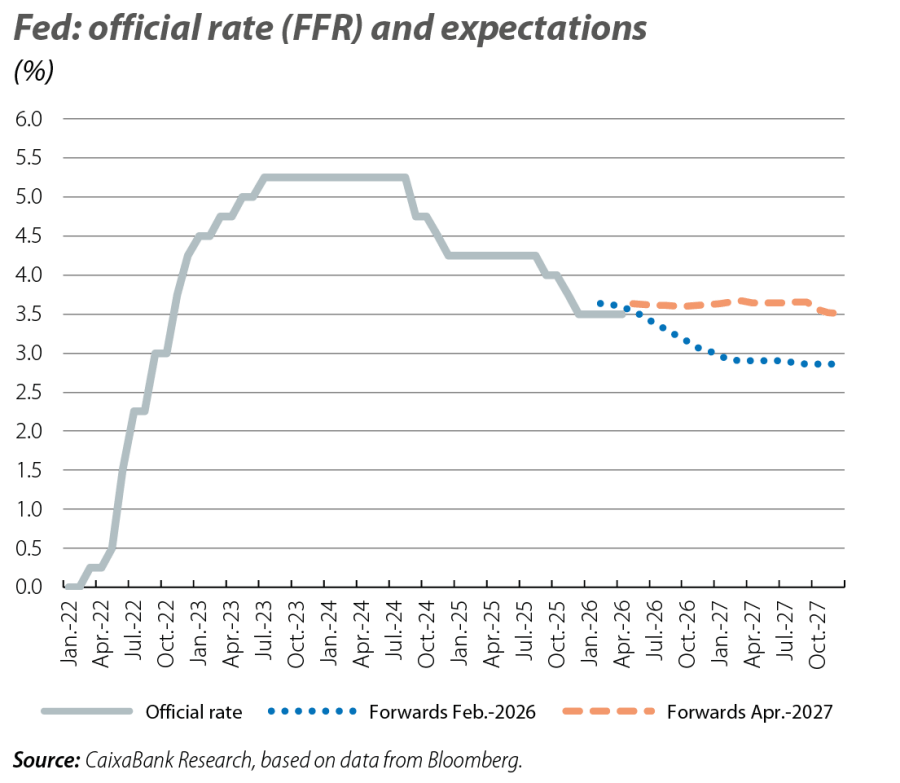

The Fed kept interest rates unchanged in April (fed funds rate in the 3.50%-3.75% range). This decision was expected, but the central bank struck a notably more cautious tone. The Fed expressed greater concern about inflation and indicated a reduced willingness to resume rate cuts (at the close of this report, markets were assigning less than a 10% probability to a rate cut in 2026). The meeting was marked by Jerome Powell’s departure as chair. Departing from tradition, Powell will remain as a governor of the Fed until the legal attacks against the institution, which he considers a threat to its independence, are resolved in a final and transparent manner. His successor should be Kevin Warsh, pending his final confirmation by the Senate. The central banks of Japan and England adhered to expectations and kept rates at 0.75% and 3.75%, respectively. In both cases, hawkish signals dominated, with dissent in favour of raising rates, and markets are pointing to 25-bp hikes at their June and July meetings, respectively.

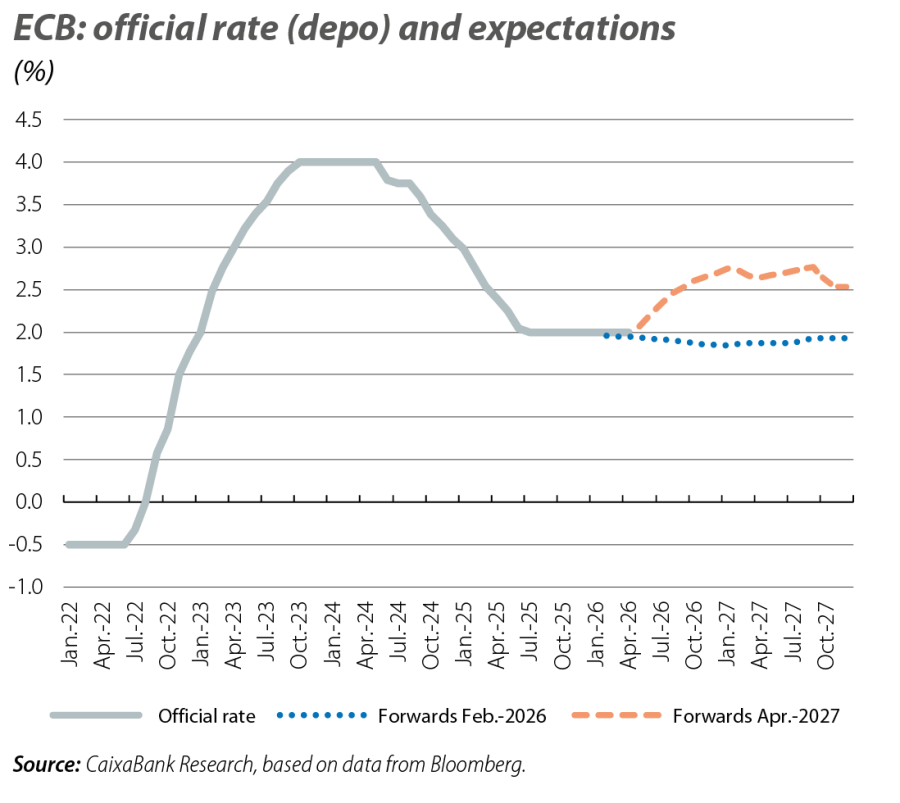

The ECB hints at a rate hike in June

The ECB kept interest rates unchanged in April (depo rate at 2.00%). The decision was unanimous, although President Lagarde herself acknowledged that a rate increase had been discussed. The ECB maintained a balanced tone in its communication, highlighting both the upside risks to inflation and the downside risks to activity stemming from the conflict in the Middle East. In an uncertain environment, it advocated maintaining a «meeting-by-meeting» and «data-dependent» approach, «not pre-committing to a particular rate path». However, the communication also hinted at a high likelihood of raising rates in June. The ECB highlighted that the war in the Middle East will drive inflation «materially above 2% in the near term». The direct effects on inflation are visible (in April, energy raised inflation to 3.0%) and there are signs of some indirect effects. With all this, Lagarde acknowledged that they will reassess the situation in the coming weeks, admitting that she is clear about the direction of monetary policy while expressing no discomfort with regard to financial market expectations (which in the last month continued to price in between two and three 25-bp hikes in the depo rate for the whole of 2026).