The Middle East leaves a «furious» mark on financial markets

The war triggered significant risk aversion, leading to stock market declines, spikes in volatility, a flight to safe-haven assets, and a sharp tightening in energy and other commodity prices. This increase in energy prices, in turn, led to a rise in short-term inflation expectations, resulting in a significant adjustment of monetary policy expectations and an increase in sovereign interest rates. In a context of high uncertainty regarding the duration and intensity of the conflict, markets reacted very sensitively to a constant flow of news such as political statements, episodes of military escalation and fluctuations in the rhetoric of international leaders.

Geopolitical uncertainty drives markets

March was marked by a notable increase in volatility in the global financial markets, with the conflict in the Middle East as the main catalyst. The war triggered significant risk aversion, leading to stock market declines, spikes in volatility, a flight to safe-haven assets, and a sharp tightening in energy and other commodity prices. This increase in energy prices, in turn, led to a rise in short-term inflation expectations, resulting in a significant adjustment of monetary policy expectations and an increase in sovereign interest rates. In a context of high uncertainty regarding the duration and intensity of the conflict, markets reacted very sensitively to a constant flow of news such as political statements, episodes of military escalation (Israeli attacks on energy facilities and the involvement of regional players like the Houthis) and fluctuations in the rhetoric of international leaders. The overall tone of markets was one of fragility and unstable sentiment. As a reflection of the persistence of geopolitical risks and uncertainty regarding the impacts of the conflict, at the beginning of April markets experienced sessions with recoveries (supported by expectations of a de-escalation and the announcement of a truce) and new episodes of risk aversion (amid fears of further military escalation).

Energy prices surge

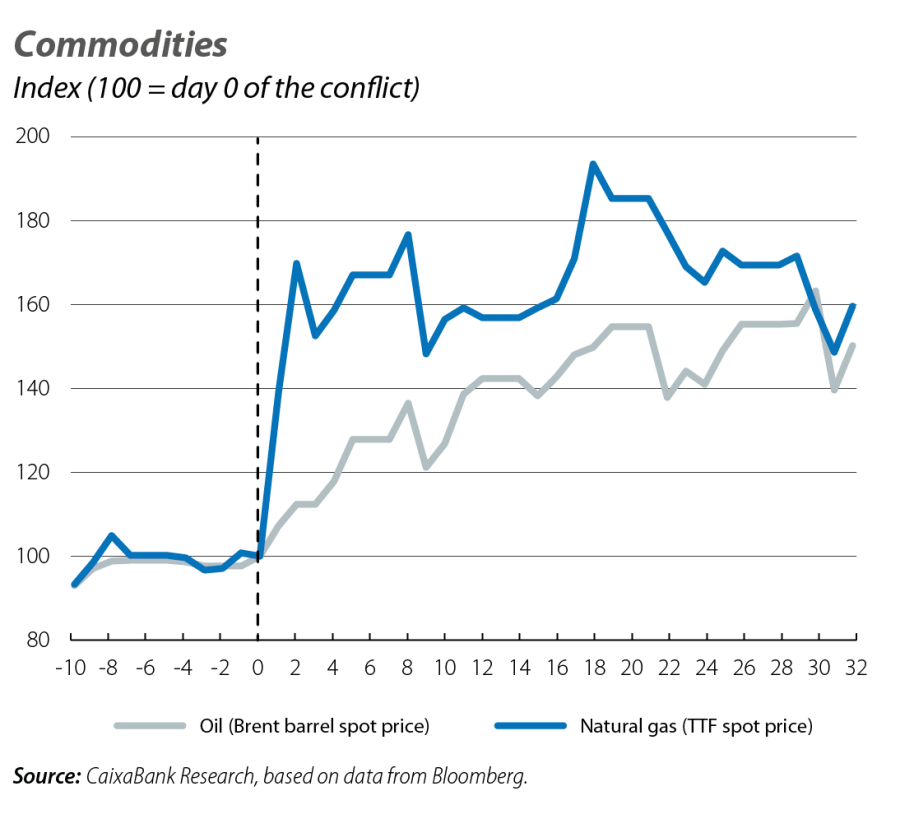

The most immediate transmission channel of the conflict to financial markets has been through energy commodities. The Middle East is a critical focal point for both the production and the global transportation of hydrocarbons, with the Strait of Hormuz playing a particularly key role, as approximately 20% of the world's crude oil and natural gas pass through it, creating significant tensions regarding supply expectations. In this context, the price of Brent surged by over 60% since the start of the conflict, at times reaching close to 120 dollars per barrel, the highest level since 2022 in the aftermath of the invasion of Ukraine. TTF gas in Europe, also recorded a significant increase of over 70%, reaching peaks slightly above 60 euros/MWh during moments of greatest tension. At the end of March, futures markets continued to price in a scenario of structurally higher prices than before the conflict, with year-end estimates close to 80 dollars per barrel for Brent and 50 euros/MWh for gas, well above previous levels (68 dollars and 32 euros/MWh, respectively).

The increase in energy costs also affected derivative products. In the US, the price of gasoline rose to 4 dollars per gallon, an increase of nearly 35% in just one month. Other derivatives such as fertilisers, especially urea from the Middle East, also recorded sharp increases of up to 55%, which could have additional implications for agricultural prices in the coming quarters. Among other commodities, the tension was more moderate. Industrial metals, such as aluminium, recorded more contained increases (of around 10%), while agricultural commodities rose by less than 5%. Precious metals showed weaker performance, with declines of around 10%, reflecting both the strengthening the dollar and a slight correction in gold and silver following last year's strong rally.

Markets anticipate more restrictive central banks

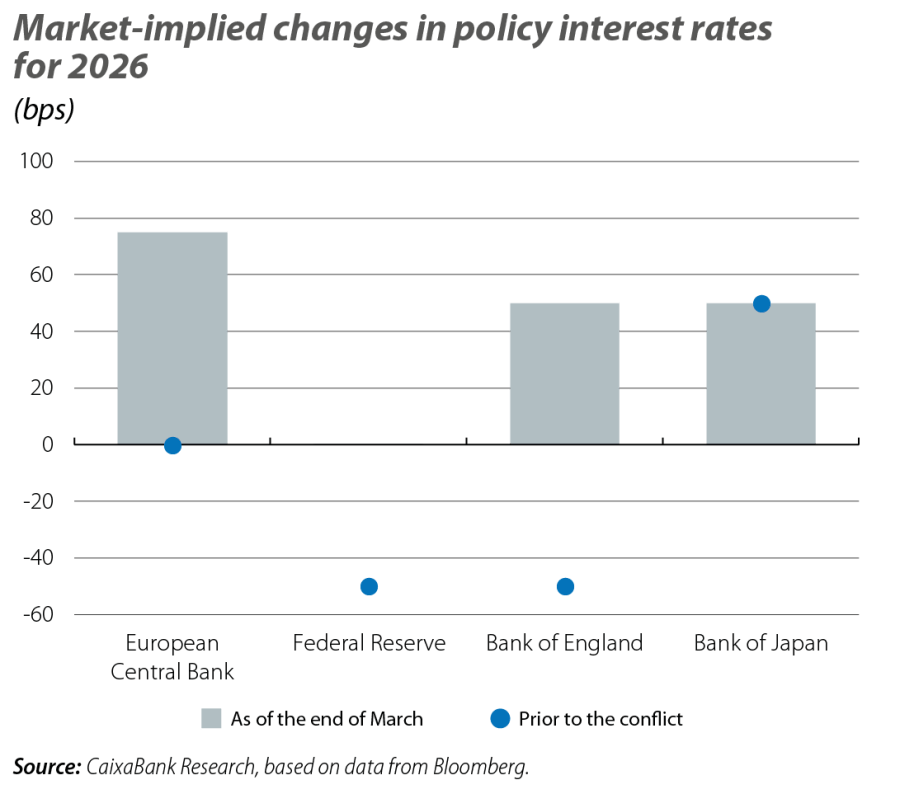

The ECB kept interest rates unchanged at 2.00% at its March meeting, but explicitly acknowledged the inflationary risks arising from increased energy costs resulting with the conflict. In this regard, the institution adopted a more hawkish tone and indicated the possibility of tightening the monetary policy stance if a significant pass-through of energy costs to the overall price basket is observed. The ECB emphasised that it is starting from a neutral stance, which gives it room for manoeuvre, and reiterated its data-dependent approach. As a result, by the end of March, markets began to anticipate three rate hikes throughout 2026 (depo rate at 2.75%) compared to the expectation of stability from the beginning of the year. This adjustment was reflected in interbank interest rates, with the 12-month Euribor rising by some 60 basis points to 2.9%, the highest since September 2024.

In the US, the Fed adopted a more cautious stance towards the conflict. While acknowledging the risks associated with rising energy costs, it considered premature to assess their macroeconomic impact and chose to focus its communication on the balance of domestic risks. In particular, the Fed expressed concern about the trend in goods inflation, affected by tariffs, and signs of weakness in the labour market. Chair Jerome Powell indicated that, in principle, they would be willing to «look through» a temporary energy shock, provided that long-term inflation expectations remain well anchored. However, the overall tone was cautious and he avoided committing to a specific path for rates. Markets made a hawkish reading of these messages and postponed the next rate cut to mid-2027, once the impact of the energy shock has dissipated, thus anticipating a Fed in «pause» mode during 2026. The shift in expectations extended to other economies. In the United Kingdom, the change was particularly notable and investors shifted from anticipating two rate cuts to two and three hikes for 2026. In Japan, meanwhile, expectations of at least two rate hikes were reinforced.

Sovereign rates reflect inflation risks and the shift in monetary policy expectations

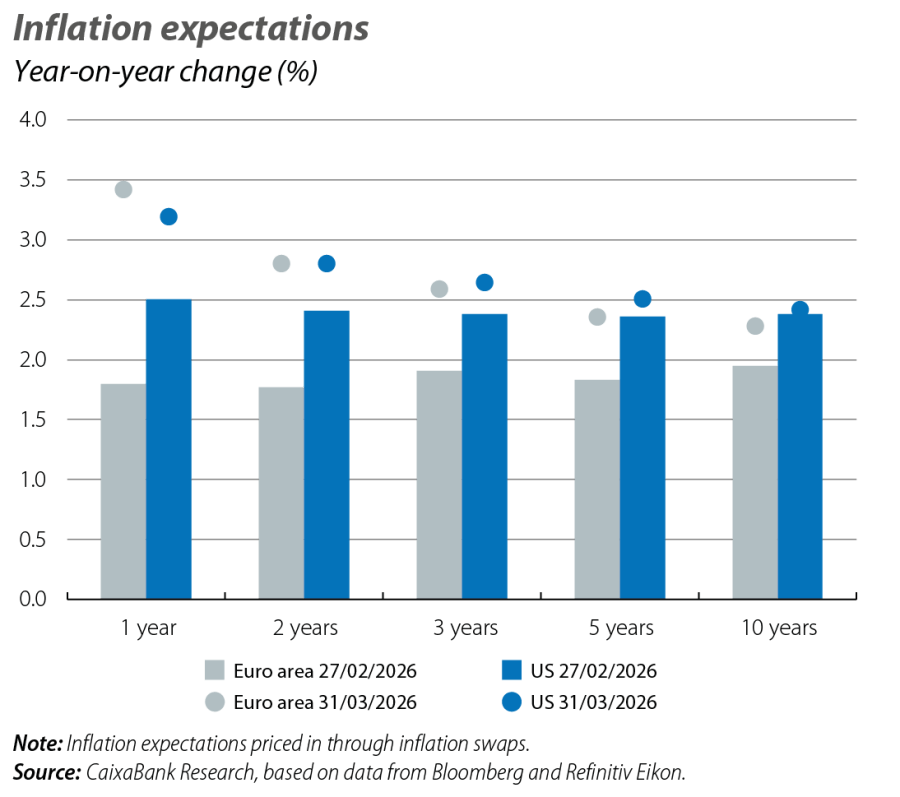

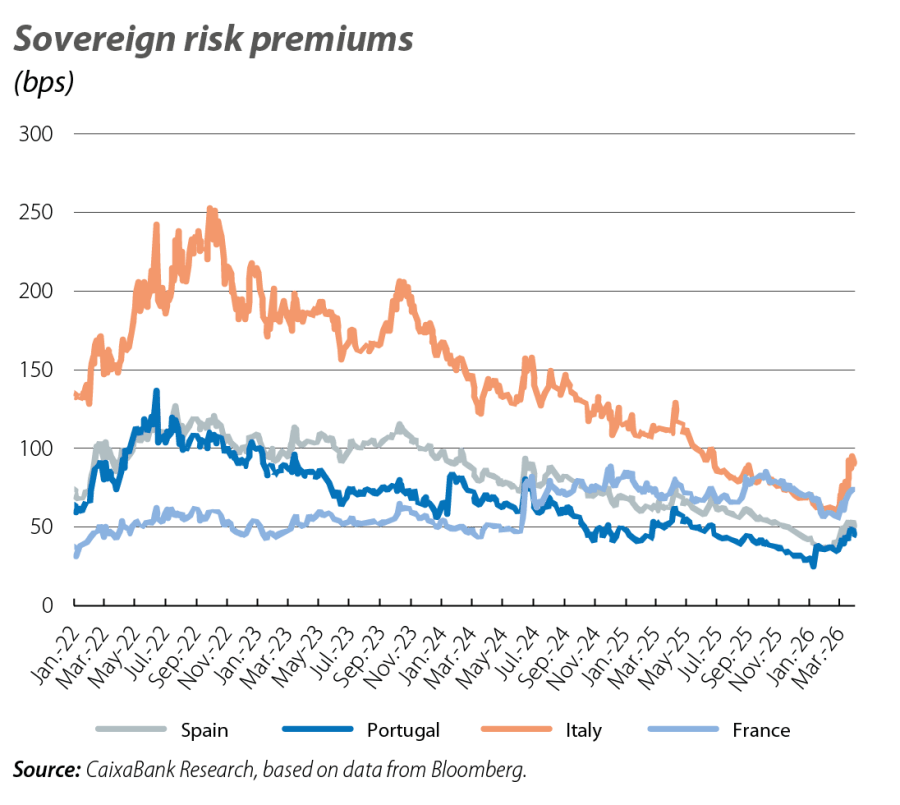

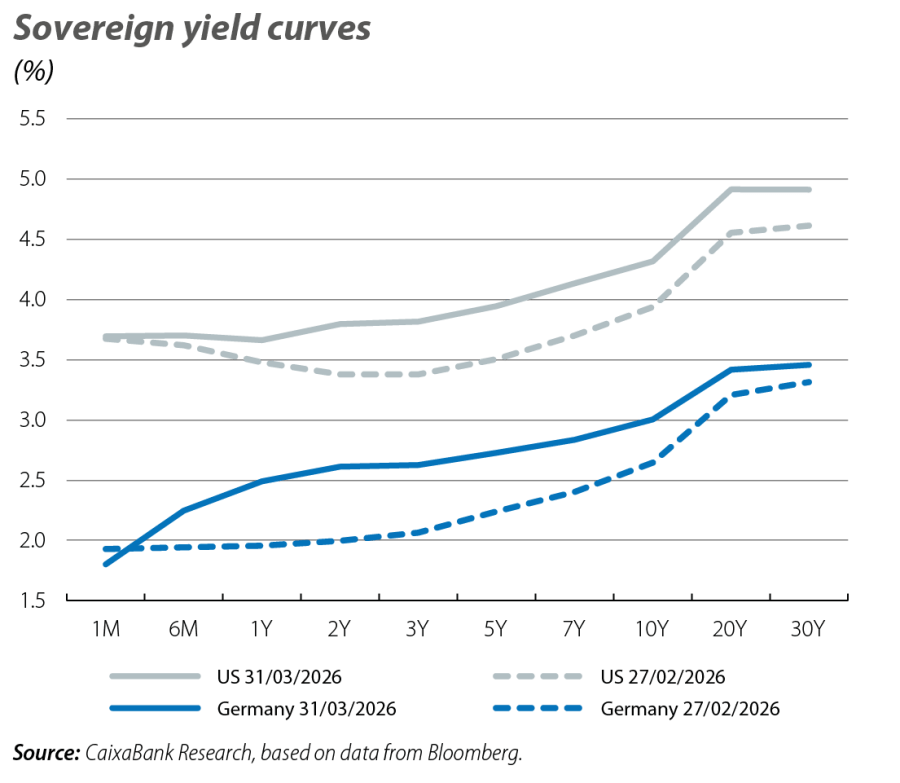

Sovereign debt markets clearly reflected the combined impact of rising energy costs and the tightening of monetary policy expectations. In general terms, interest rates rose significantly, with particularly pronounced movements at the short end of the curves. In Germany and the US, short-term rates rose by approximately 60 and 40 basis points, respectively, during March. Euro area peripheral risk premia periphery also tightened, especially in Italy (given the country's greater energy dependence), but their levels nevertheless remained contained, particularly in Spain and Portugal (by end of March stood at 50 bps and 45 bps, respectively). Of particular note was the rebound in long-term US rates (also around 40 bps): while long-term inflation expectations have remained relatively anchored, the increase in nominal rates is largely explained by a rise in real rates. This suggests that investors are demanding higher returns to compensate for future uncertainty, whether due to increased inflationary volatility or a world of greater uncertainty, amid a backdrop of deteriorating public finances.

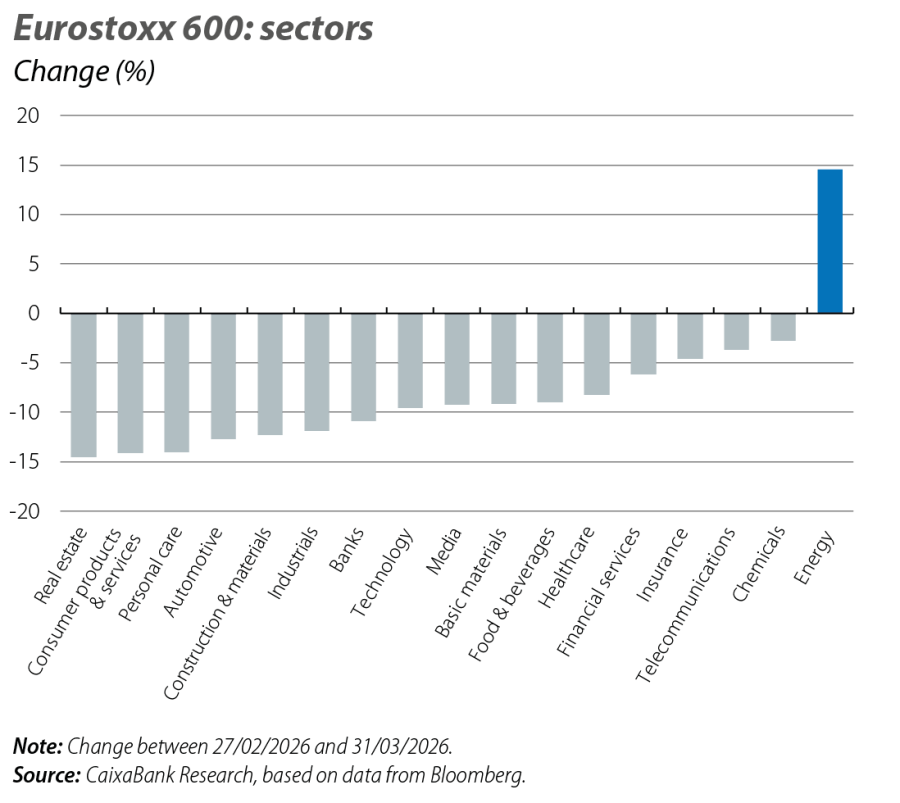

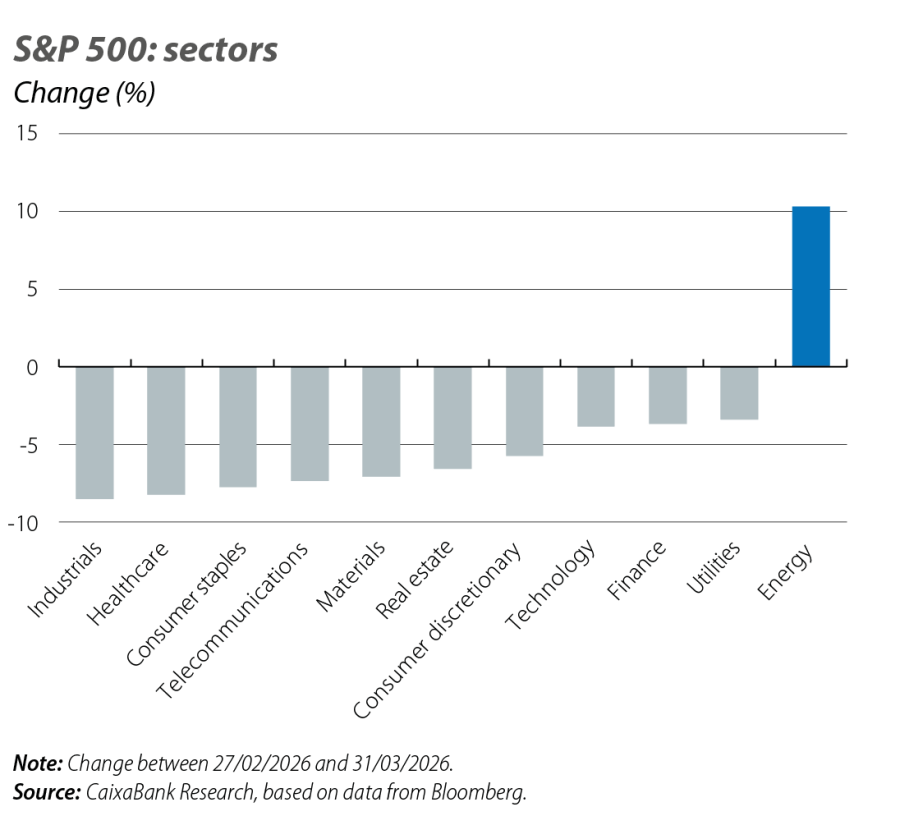

Only the energy sector escapes stock market declines

The increase in geopolitical uncertainty and the tightening of financial conditions resulted in widespread declines in global stock markets. Advanced and emerging economies acummulated declines of 10% by the end of March, and most indices accumulate losses year to date. The declines were particularly pronounced in Asia, given its high energy dependence on the Middle East. At the sectoral level, almost all sectors recorded setbacks, with notable declines in more cyclical sectors such as industry, tourism and real estate. Other sectors showed relative resilience, including defensive sectors such as utilities, as well as the US tech sector. The major tech firms, which were already experiencing a period of correction prior to the conflict due to high valuations and doubts around the profitability of their massive investments in AI, showed a relatively more robust performance compared to other sectors, supported by their lower direct exposure to the energy cycle. The only sector with positive performance was the energy sector, due to the expectation of greater profits resulting from the rebound in commodity prices.

The dollar regains some of its appeal as a safe-haven asset

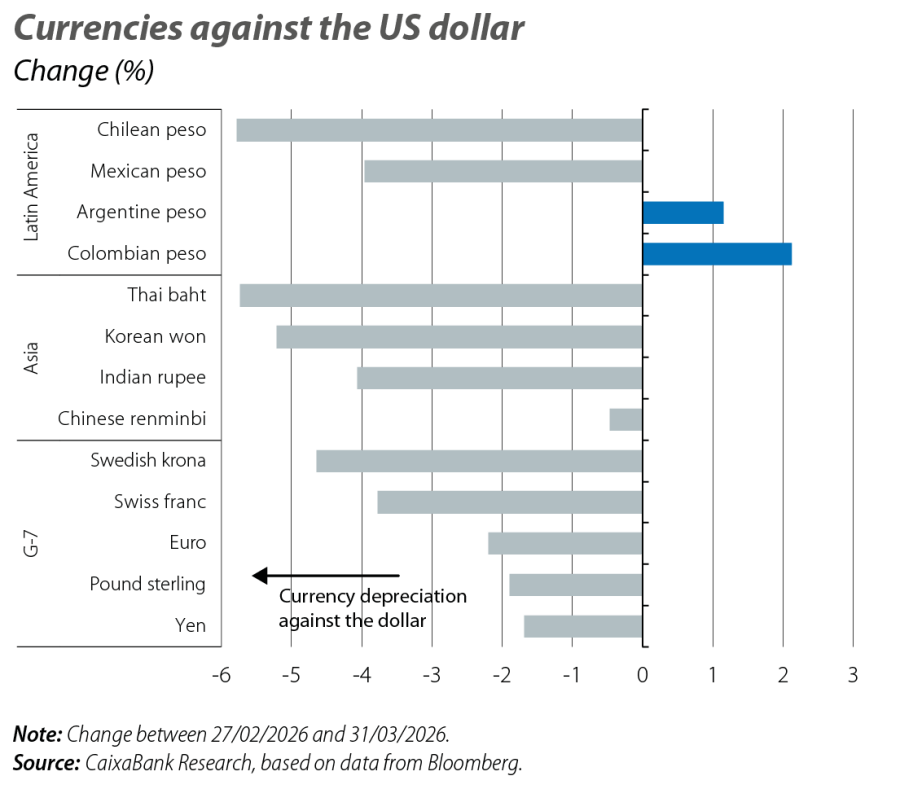

In currency markets, the dollar was the main beneficiary of risk aversion sentiment. After weakening for most of 2025, the US dollar regained ground against its main counterparts, driven by its safe-haven status and the relatively lower exposure of the US economy to the conflict. Within the G-10, the pound sterling and the Japanese yen showed relatively better performance, with moderate depreciations, while the euro traded around 1.15 during the month, down from the pre-conflict levels of 1.18. Currencies such as the Swedish krona recorded sharper declines. In Asia, the currencies most exposed and dependent on Gulf energy flows, such as the South Korean won or the Taiwanese dollar, depreciated by more than 4%, while the Chinese renminbi remained relatively stable (China accumulated significant crude oil reserves and is better positioned in terms of supply in the current context). In Latin America, divergences were observed depending on countries’ exposure to commodities. The Colombian peso, supported by its status as a crude oil exporter, strengthened, while other currencies such as the Chilean peso registered declines.

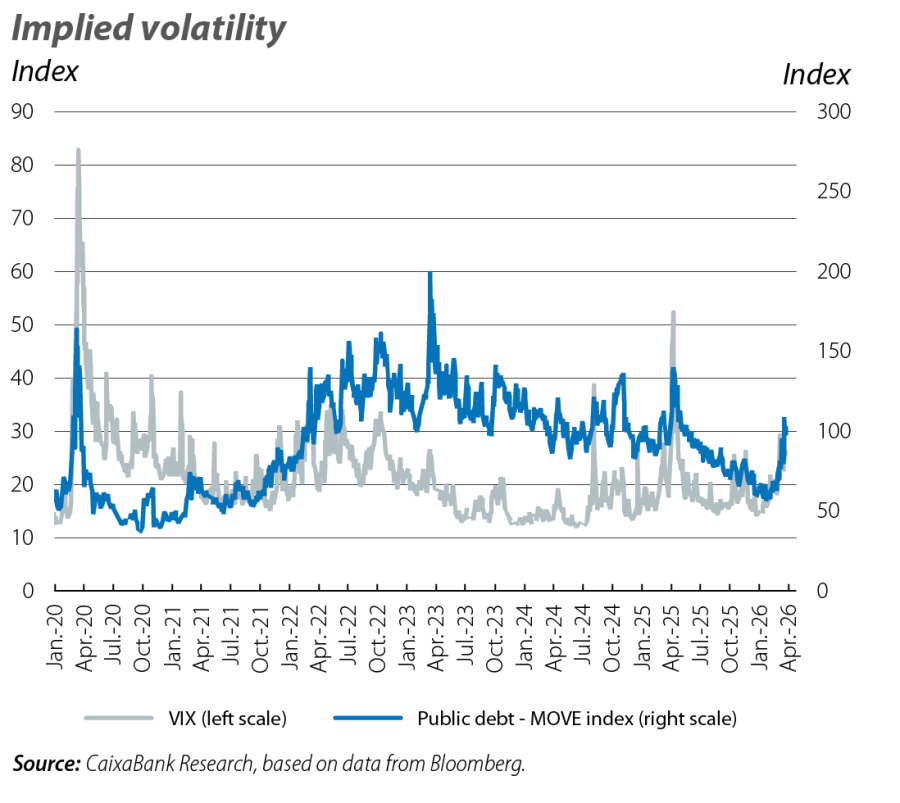

High volatility in an uncertain environment

Overall, March was characterised by a highly volatile environment, with indicators such as the VIX exceeding 30 points at the moments of greatest tension – levels not seen since «Liberation Day» in April 2025. In the coming months, the evolution of the conflict will continue to be the main driver of financial markets. In particular, the duration, intensity and aftermath of the tensions will be key for assessing the impact on energy and its transmission to the rest of prices, the global economy and, therefore, the path of monetary policy and financial conditions. Meanwhile, markets will continue to navigate an environment of high uncertainty that increases the propensity to experience episodes of volatility.