Financial markets, to the rhythm of geopolitics and AI

The start of 2026 has brought volatility and mixed dynamics reflecting the markets' sensitivity to geopolitical and technological shifts. The threat of a military conflict between the US and Iran had already heightened the perception of risk before the bombings materialised and triggered a sharp increase in stress and volatility, especially in commodity markets.

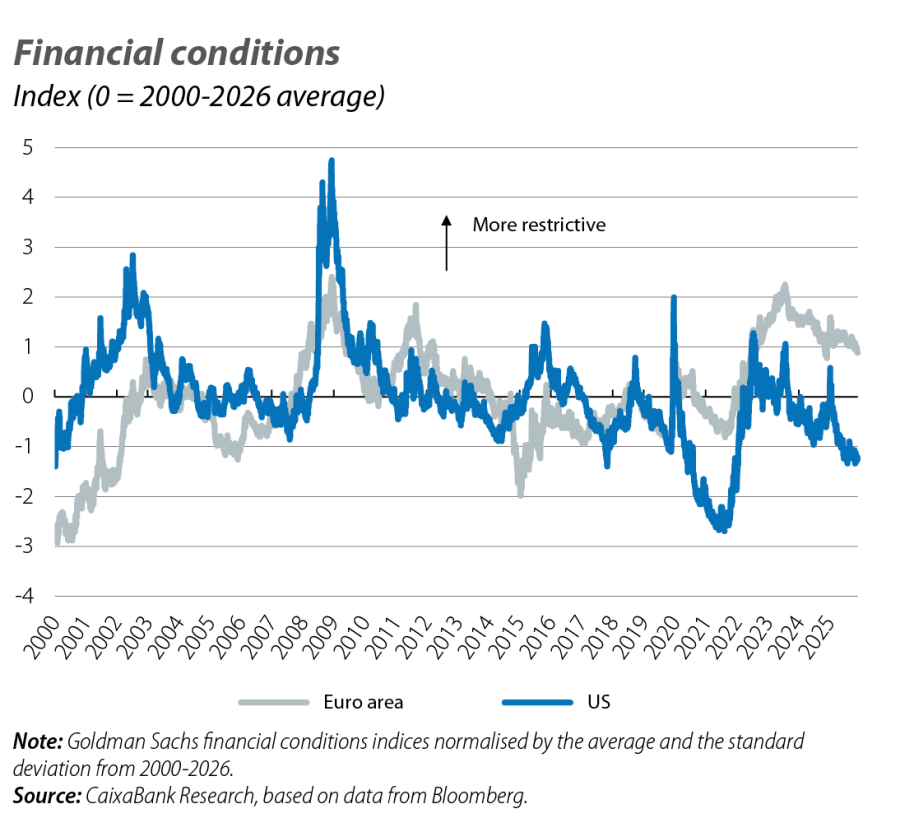

Financial conditions amid mixed dynamics

The start of 2026 has brought volatility and mixed dynamics reflecting the markets' sensitivity to geopolitical and technological shifts. The threat of a military conflict between the US and Iran had already heightened the perception of risk before the bombings materialised and triggered a sharp increase in stress and volatility, especially in commodity markets. In parallel, AI continues to influence stock markets not only due to high company valuations and the challenge of making ambitious investment plans profitable, but also due to fears of disruption to established business lines. In addition to all this, in February the US Supreme Court ruling annulled a significant portion of the tariffs imposed by the Trump administration. These catalysts drove mixed stock market performance, while commodities were pushed upwards and investor sentiment led to a slight recovery in the dollar in the currency markets and opposing dynamics between long-term interest rates on both sides of the Atlantic.

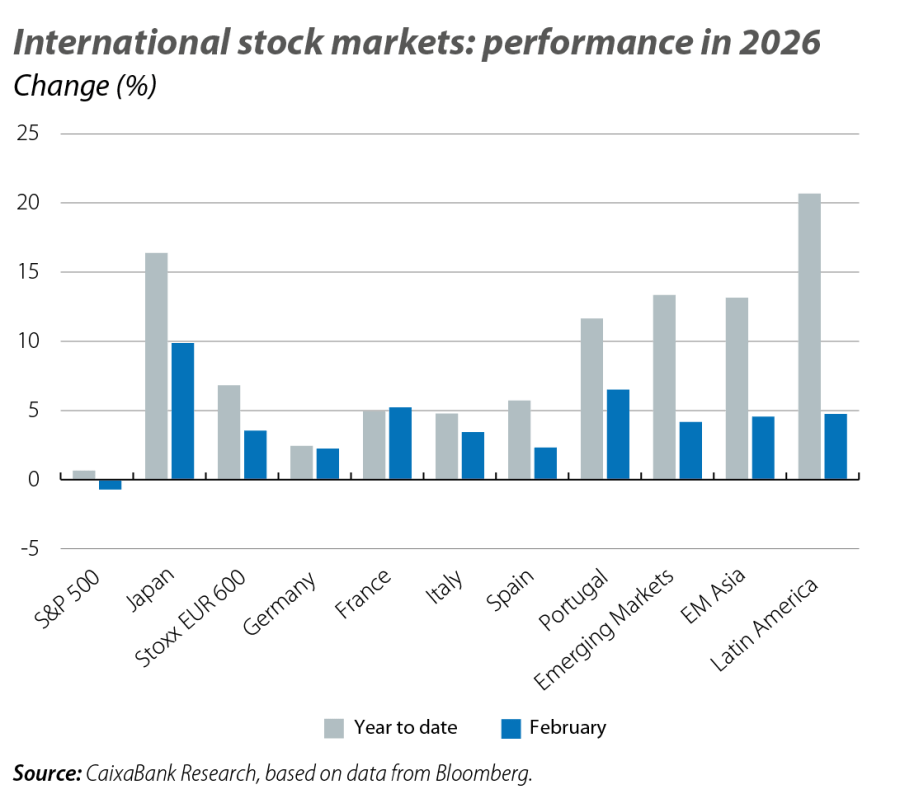

Markets on the rise… until the outbreak of conflict in Iran

February opened with uneven performance among the main international stock markets, torn between the boost from a good earnings season and doubts generated by the momentum of AI-related companies. In the US, the fear that these firms might disrupt traditional business models put pressure on established firms within the technology and communication services sectors, leaving the S&P 500 virtually flat in February. In contrast, indices in the rest of the world gained more traction: European stock markets recorded notable gains, approaching +4% overall in February, driven by more balanced growth prospects and favourable investor sentiment following the Supreme Court’s ruling. In emerging markets, the regional index for Asia was approaching gains of 7%, while the Latin American index exceeded 4%. Globally, Japan stood out in particular, where the Nikkei recorded increases of over 10%, encouraged by the electoral victory of Sanae Takaichi and her reflationary agenda. However, at the beginning of March, the bombings in Iran triggered widespread declines in global stock markets, with the European stock market retreating to levels of late 2025.

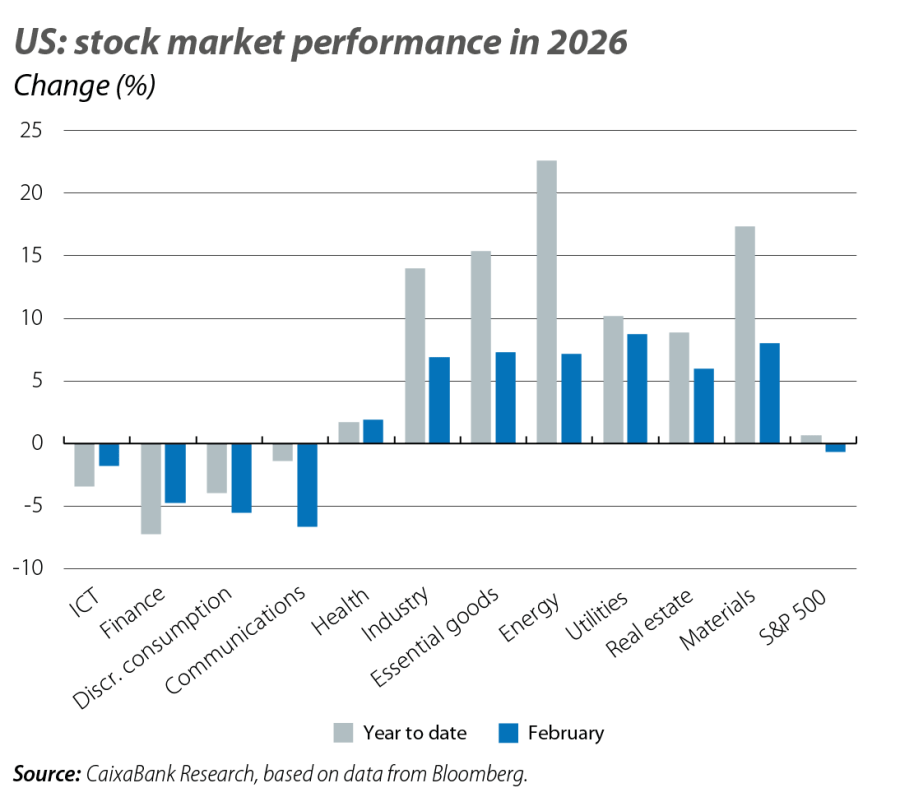

Macroeconomic dynamism supports business earnings

The earnings season in the US closed with a solid overall picture, in a context of robust performance of the American economy: around 85% of the companies in the S&P 500 exceeded sales expectations and around 75% did so in profits. The greatest impetus came from the financial and tech sectors, where the firms most closely linked to AI maintained the combination of good reported results and ambitious investment plans. In Europe, while the tone was more moderate, the balance as of the close of this report was also positive, with the tech, financial and utilities sectors standing out.

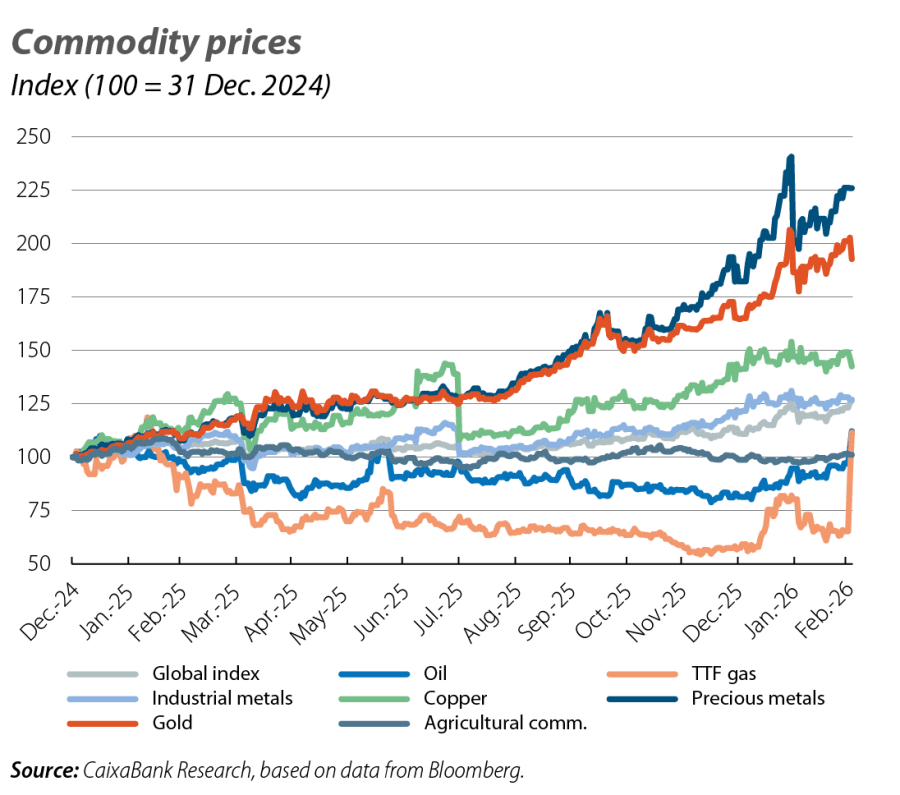

Geopolitics drives up commodities

February was a month of tense calm in energy prices. The balance between the expectation of an oversupply in the oil market and the increasing risk premium arising from geopolitics pushed the price of the Brent barrel towards the 70-dollar mark, while the TTF gas price fell towards 30 euros per MWh, aided by an increase in liquefied natural gas imports at northern European terminals and forecasts of milder temperatures for the end of the winter. However, the exchange of attacks between Iran and the US and Israel in early March exerted significant pressure on prices, with oil surpassing 100 dollars per barrel of Brent and TTF gas reaching nearly 60 euros per MWh and experiencing considerable volatility (briefly surpassing 65 euros). Futures curves became relatively less expensive, indicating an easing of tensions towards 2027.

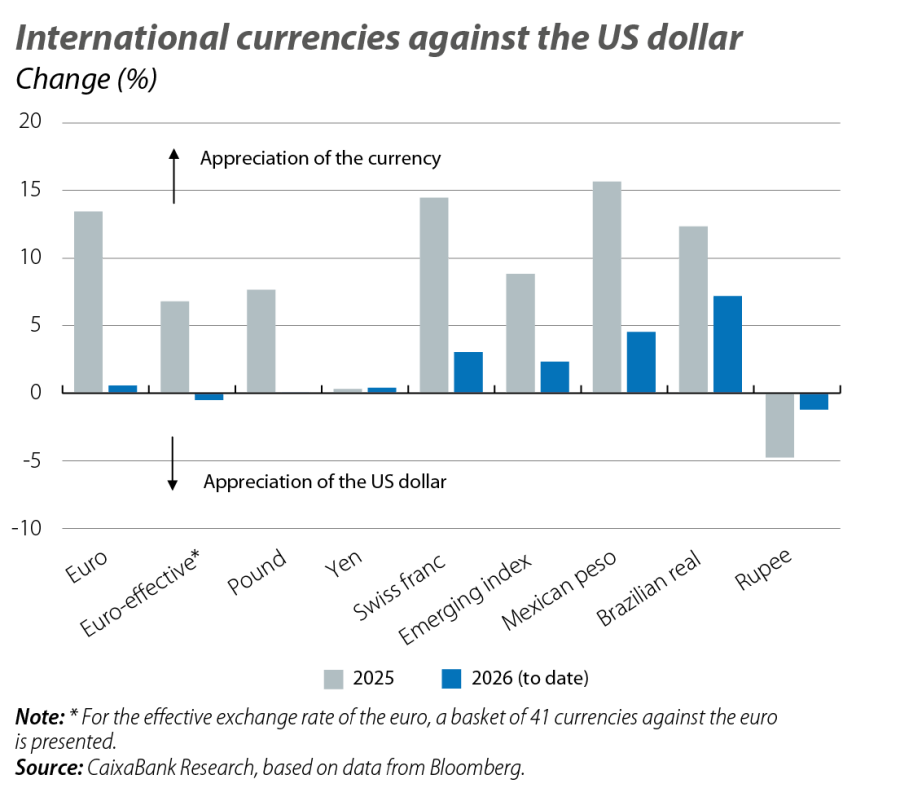

The dollar takes a breather

The behaviour of the US dollar was erratic during February, but it managed to close the month with a slight recovery. The Supreme Court’s ruling helped to ease the downward pressure that has been weighing on the currency since the tariff announcements of 2025, while the war in Iran moderately benefited it in its role as a safe-haven asset. The euro remained relatively stable, at around 1.18 dollars (weakening towards 1.15 dollars following the bombings in the Middle East), the pound hovered around 1.35 dollars and the yen also weakened. Among emerging currencies, the best performing ones were those that benefited the most from a more direct reduction of tariffs: throughout February, the Brazilian real appreciated by more than 3% against the dollar, while the Chinese yuan appreciated by just under 1% and the Indian rupee by more than 1% (capitalising on the US-India trade agreement). Nevertheless, the bombings ultimately led to a widespread weakness among emerging currencies.

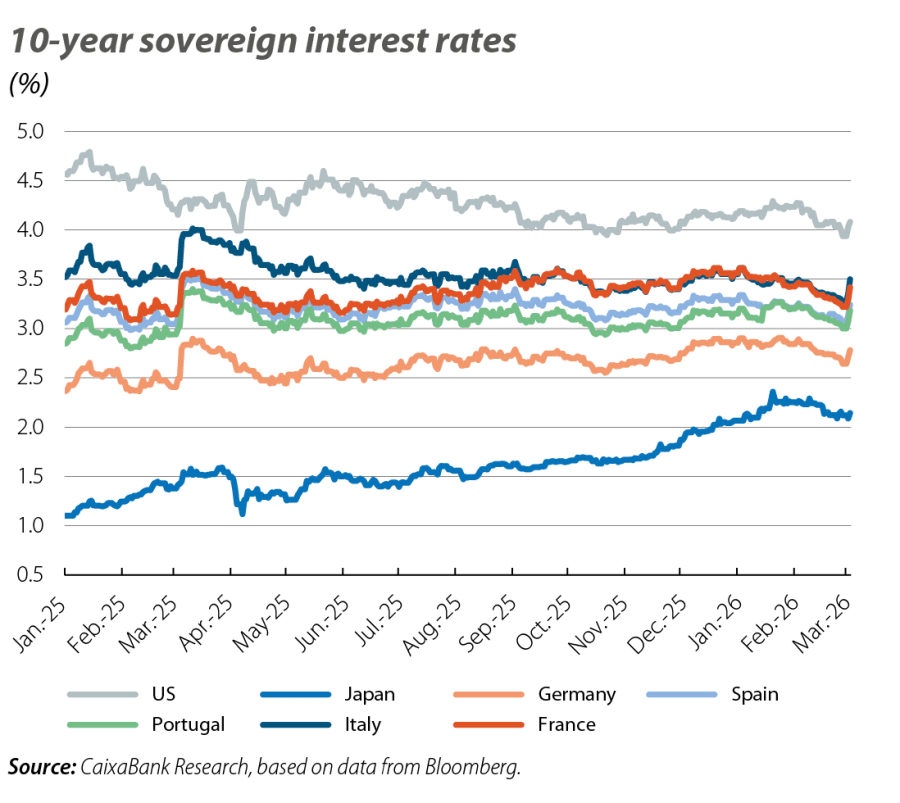

Fluctuations in interest rates

In a February without monetary policy meetings among the major central banks, investors initially bet on a decline in sovereign rates in both the US and the euro area. However, the stress triggered by energy prices following the bombings in the Middle East pushed rates up due to a surge in inflation expectations and a hawkish revision of the monetary policy outlook on the part of investors. Net, sovereign interest rates remained stable in the US (rising at the short end of the curve and falling at the long end), while in the euro area rates registered an increase (more notably in the periphery than in Germany). The money markets abandoned their dovish bias for the ECB and began to price in the possibility of the ECB raising rates in 2026 (as of the close of this report, the markets were debating between one and two rate hikes). The markets also reduced their confidence in rate cuts by the Fed (although they are still pricing in two cuts for the remainder of the year). In fact, the minutes of the Fed's January meeting revealed a more restrictive tone than had been perceived, and pointed to greater concern about inflation risks. The minutes also revealed that almost all Fed members consider the current level of rates to be in neutral territory. In the euro area, the ECB demonstrated greater continuity in its communication and various interventions continued to emphasise the strategy of not over-calibrating decisions to every small change in the data, given the uncertainty of the environment.