Portugal: confidence levels recover and employment remains strong

A steady improvement throughout Q2

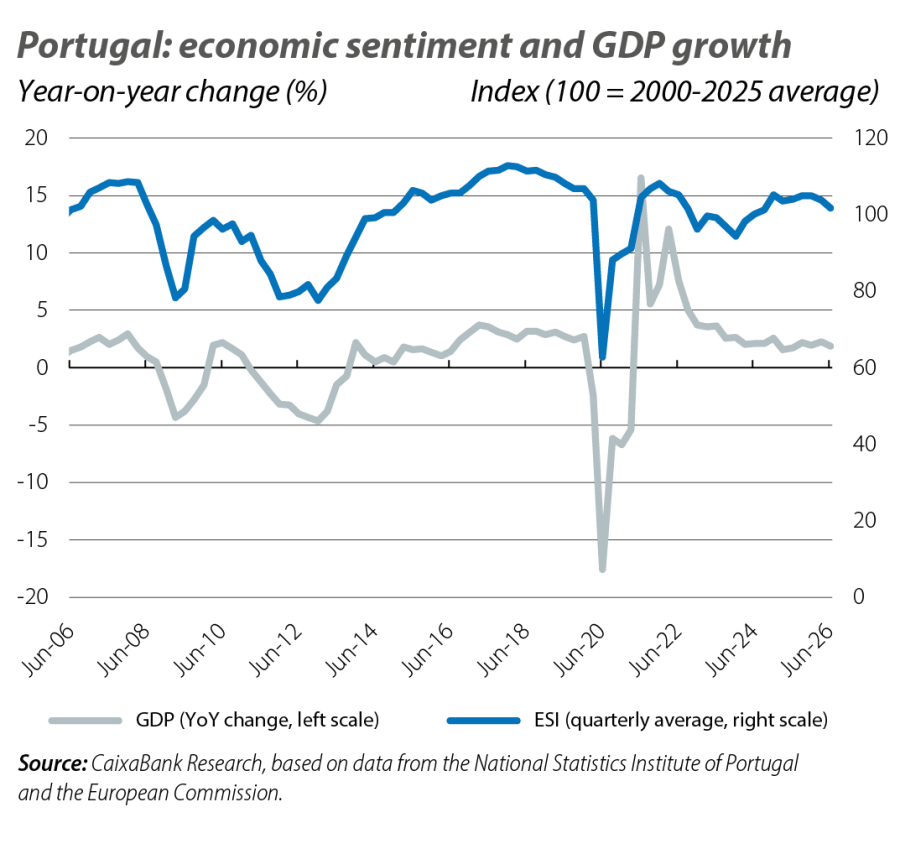

A broad recovery in key sentiment indicators has been observed since May, as uncertainty surrounding the impact of the war in Iran has steadily dissipated. In June, the European Commission’s economic sentiment indicator performed particularly well, rising to 103 points (vs. 101.7 in May). Private consumption also continues to show strength. Retail sales grew by 4.2% in the first two months of the quarter, while car registrations increased by 11.8% in Q2 (versus 10.1% in Q1). This performance was supported by the strong labour market and the growth in nominal wages, which rose by 5% in Q1. In this context, the savings rate remains close to its historical highs, at 12.3% in Q1, and investment indicators suggest a positive performance in Q2.

Mixed inflation data in June

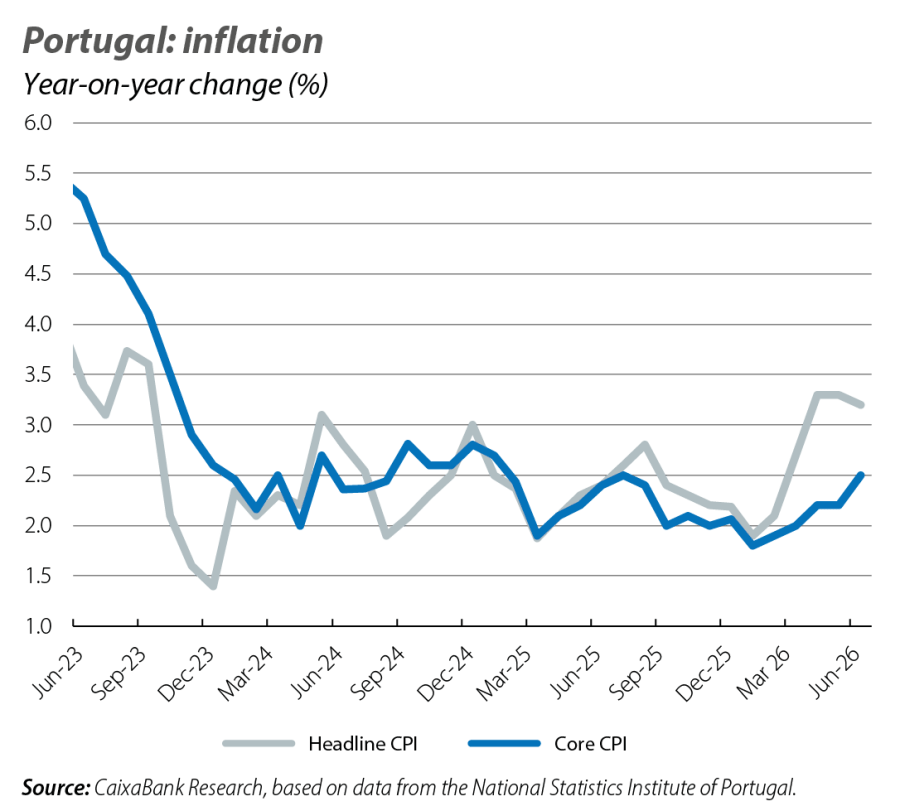

Headline inflation stood at 3.2% in June, slightly below the 3.3% recorded in May. This was due to a sharp slowdown in energy prices, which rose by 9.1% year-on-year in June (vs. 13.1% in May), following the rapid decline in global energy prices after the US and Iran signed the memorandum of understanding. Core inflation gained momentum and stood at 2.5% (vs. 2.2% in May), possibly reflecting lagged effects of the energy shock.

Employment is gaining momentum again and Q2 could be better than expected

Employment grew by 2.8% year-on-year in May, exceeding the average growth recorded in the previous four months (2.4%), and the employed population reached a new all-time high of 5,366,600 workers. The unemployment rate fell to 5.5%, representing a reduction of 0.2 pps compared to April and of 0.7 pps compared to the same month last year. These figures suggest better-than-expected labour market performance and indicate downside risks to our current unemployment rate forecast for 2026 as a whole (5.9%).

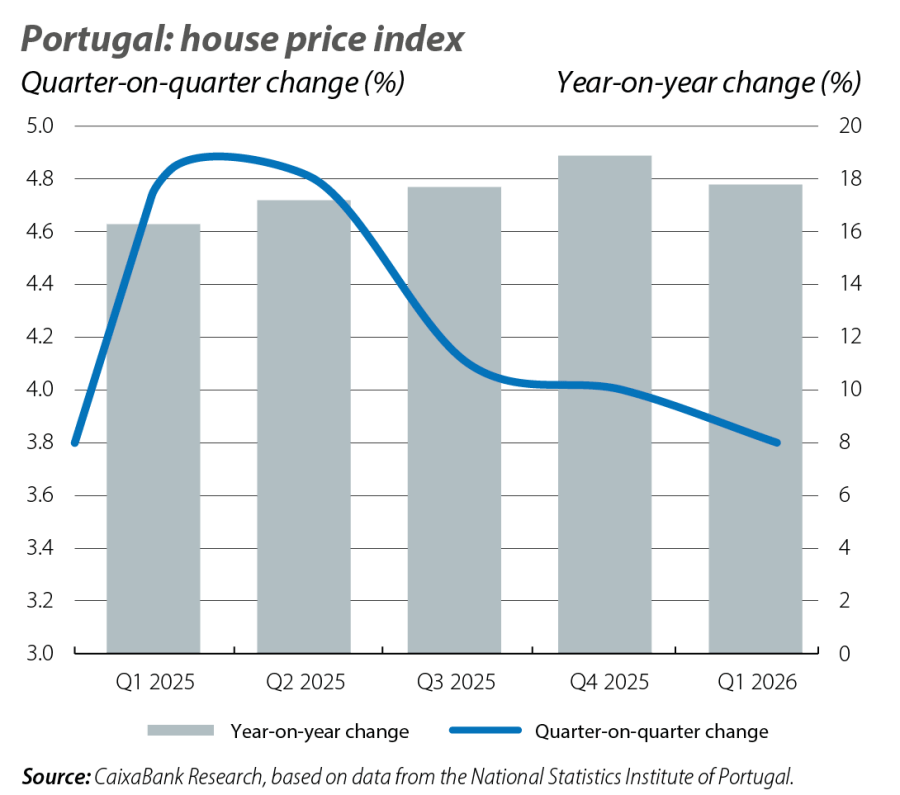

The house price index rose by 17.8% year-on-year in Q1

This figure represents a slight slowdown compared to Q4 2025 (18.9%), also reflected in the quarterly growth rate, which remained high (3.8%) but below the intensity observed in previous quarters. House sales also showed a slight moderation. During the quarter, 37,745 homes were sold, which is 8.7% fewer than in the same period last year, with a significant decline also recorded in quarterly terms (–12.4%). Expectations regarding price trends and sales have moderated, although the market fundamentals remain consistent with a strong appreciation in house prices through 2026.