Some market relief despite the uncertainty

Markets remained affected by the supply shock in May, particularly in the euro area. In an uncertain geopolitical environment with mixed signals, markets welcomed the favourable signs of rapprochement between the US and Iran. As a result, May saw a reduction in oil prices and consequently a slight moderation in short-term inflation expectations.

Markets remained highly influenced by the supply shock in May

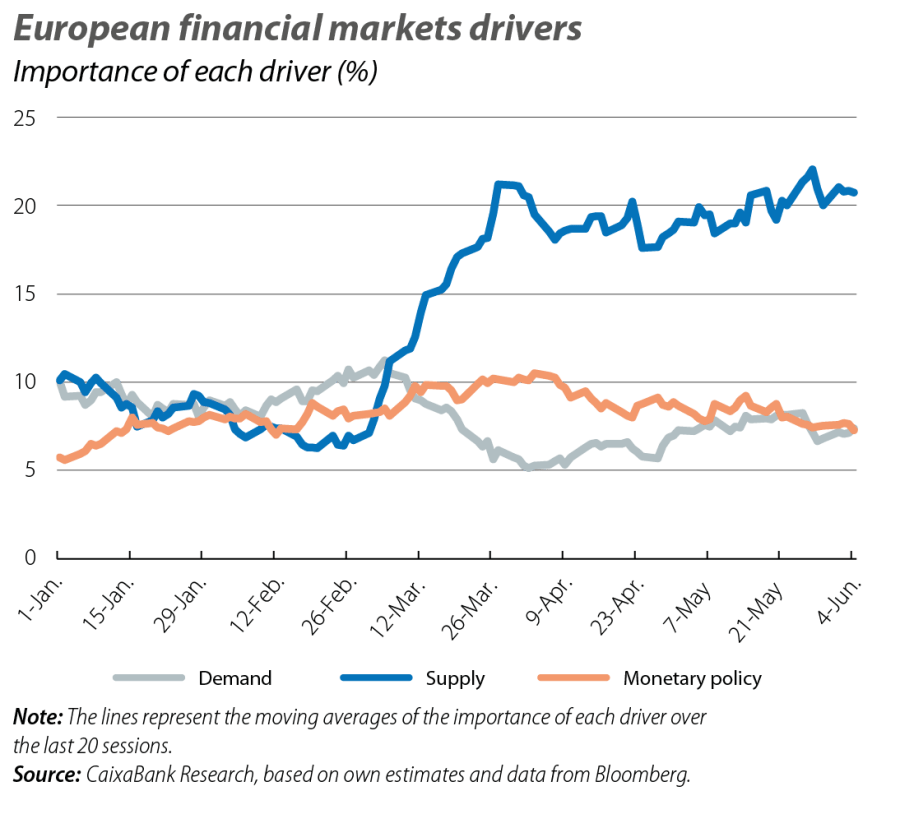

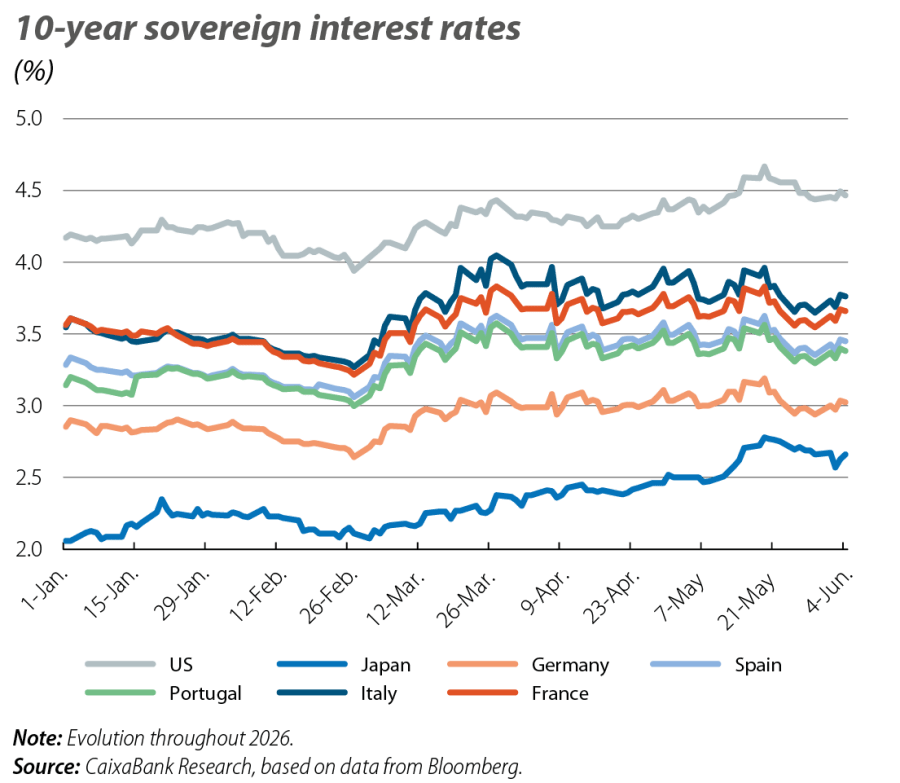

Markets remained highly influenced by the supply shock in May, particularly in the euro area. In an uncertain geopolitical environment with mixed signals, markets welcomed the favourable signs of rapprochement between the US and Iran. As a result, May saw a decrease in oil prices and consequently a slight moderation in short-term inflation expectations. European sovereign interest rates fell and this reduced risk premiums, particularly the Italian one, which was also the most stressed during the initial weeks of the conflict. In the US, however, sovereign rates rose in a month marked by the release of macroeconomic data that have shifted investors’ expectations toward a more hawkish Fed. Stock indices rose globally, with a few exceptions, supported by the tech sector. Nevertheless, the volatility priced in by the markets remained high, despite showing some relief compared to March and April.

Energy prices remain in the focus

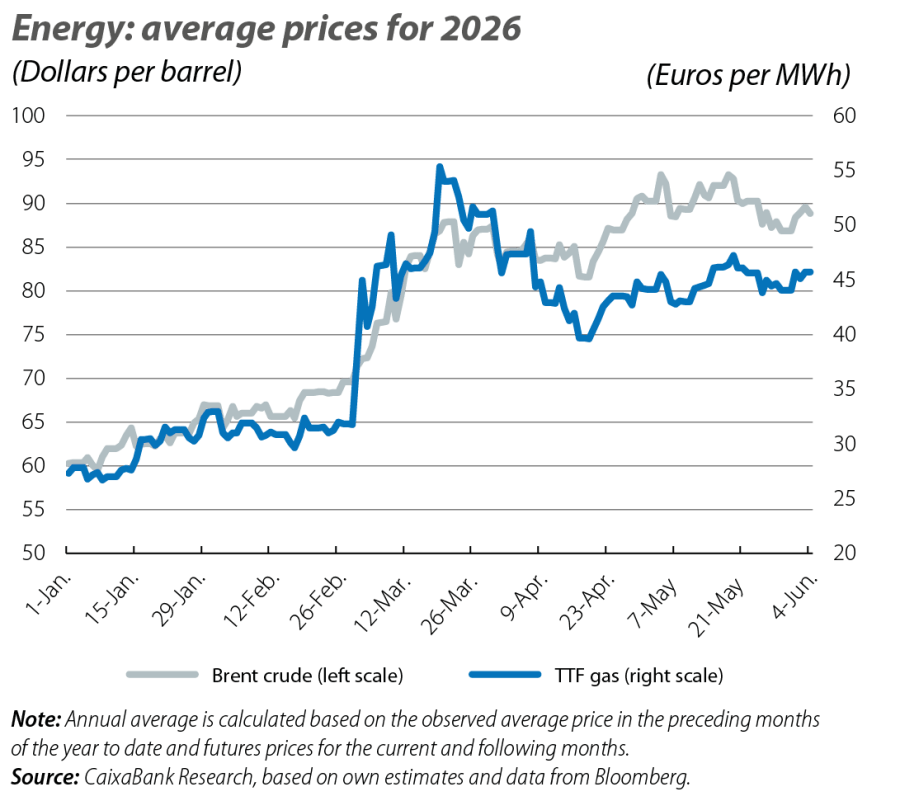

May was marked by the continuation of a fragile ceasefire in the Middle East and the ongoing closure of the Strait of Hormuz, despite the occasional traffic of a few oil tankers. Despite the uncertainty, markets were encouraged by favourable signs of a peace agreement, resulting in Brent crude opening May at around 110 dollars per barrel and closing below 100 dollars, albeit with significant volatility and a slight uptick in the final sessions of the month. However, market prices also reflected the view that restoring energy flows will be a difficult process, with futures pricing in a structurally higher 2026 year end than prior to the conflict, indicating with relative consistency a range of 80 to 85 dollars per barrel. The pattern was similar for gas prices: whereas they had been declining since the end of March, in May they were volatile within the range of 45-50 euros per MWh, and futures for the 2026 year end indicated a price of 45-47 euros per MWh (15 euros higher than before the conflict).

Stock markets continue to register gains

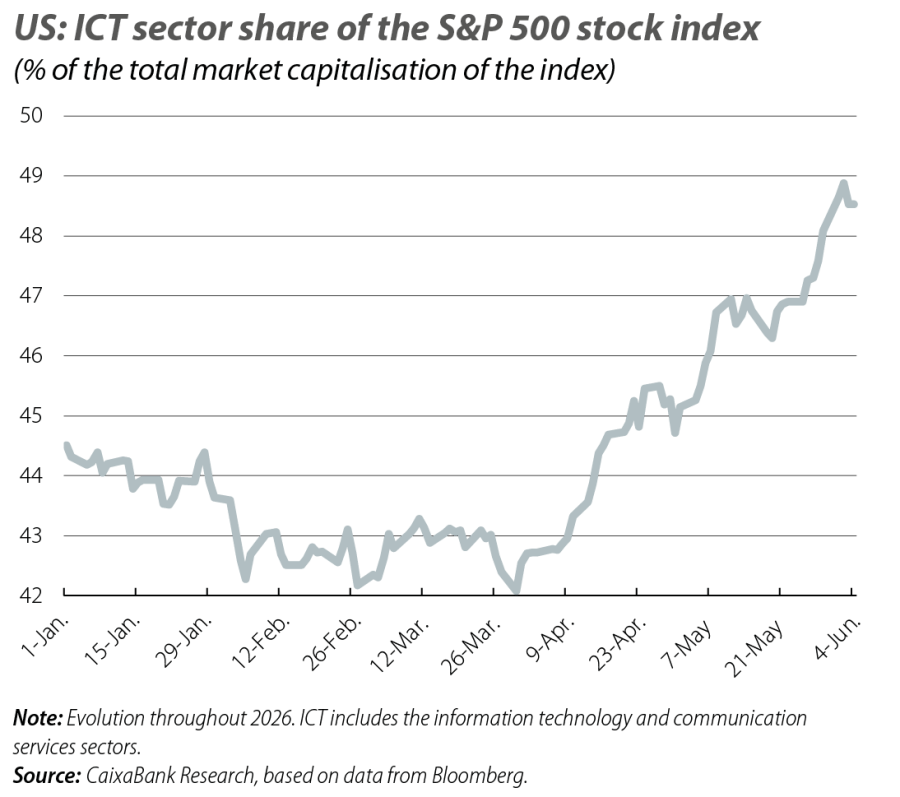

Stock markets continue to register gains, as seen in April. Driven by the rise of AI, the indices that benefited the most were those of Taiwan, South Korea, and Japan, due to their key role in chip supply chains. In the US, the S&P 500 recorded eight consecutive weeks of gains, coinciding with first quarter earnings season. However, this overall growth was mainly supported by gains among tech firms, which more than offset losses recorded in many other sectors. NVIDIA, the biggest constituent of the S&P 500, reported an 85% year-on-year increase in its Q1 profits, driven by gains from its data centres, which grew by 95% year-on-year. Thus, in the last month, the strong performance of AI firms intensified the market concentration seen in recent quarters, with the weight of tech firms in the S&P 500 rising from 42% to over 48% in just two months.

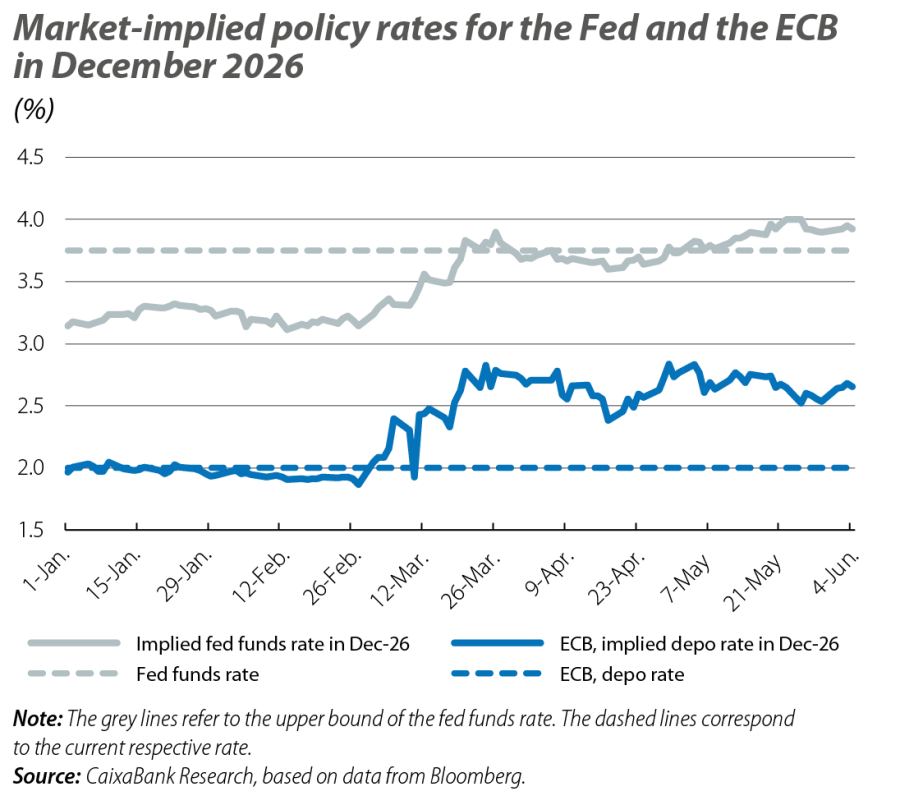

The Fed gives more hawkish signals...

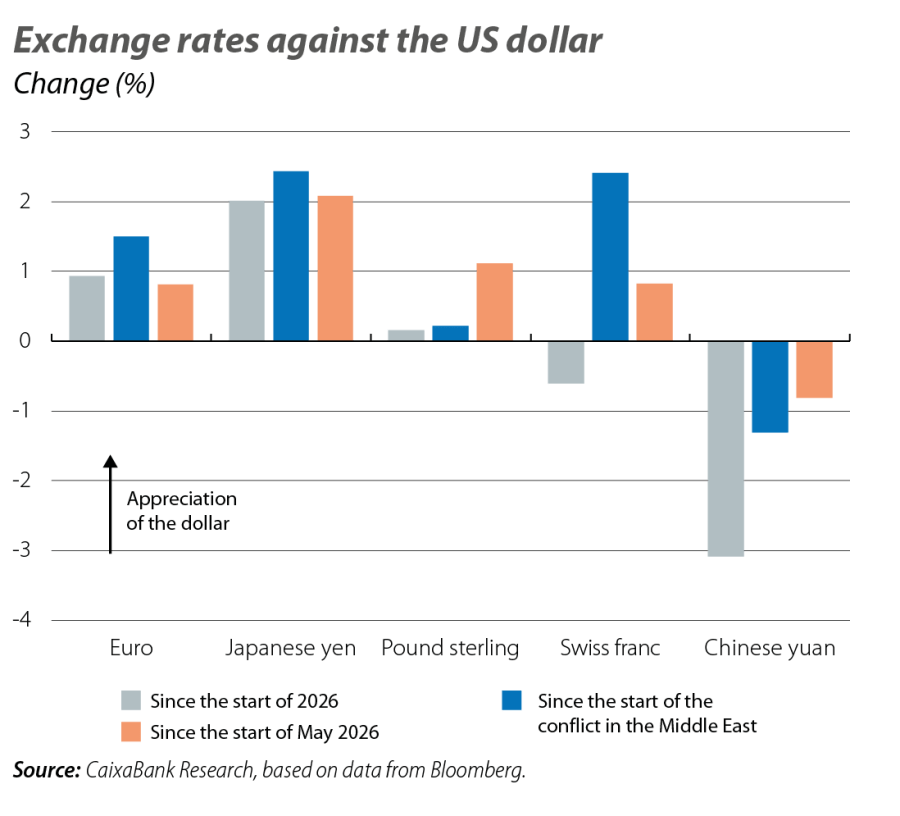

Up until early May, markets were pricing in a stable fed funds rate through to the end of the year. This was based on the energy price shock having a limited impact on US economic activity, given its position as a producer and net exporter. However, the latest macroeconomic data releases have revealed a resilient labour market and substantially higher production and import prices than analysts had anticipated. This has led investors to believe that the Fed could raise interest rates – a possibility to which financial markets were assigning a 75% probability at the close of this report. This shift in expectations led to the dollar appreciating against most major currencies. On the other hand, these adjustments are occurring amid a changing context for the bank: Kevin Warsh was officially sworn in as Fed chair. Warsh has mentioned his intention to reduce the size of the Fed’s balance sheet and to reform the bank’s communication policy (measures like eliminating the publication of the dot-plot, among others) as well as reducing the frequency of FOMC meetings. In any case, these communications have not been interpreted by the market as any short-term shift in the Fed’s direction.

… while expectations for the ECB consolidate

Dominated by the supply shock triggered by the conflict in the Middle East and its inflationary impact on the euro area, financial markets in May consolidated expectations that the ECB will implement between two and three rate hikes in 2026. This included assigning a probability of over 90% to the first 25 bp increase being announced at the meeting on June 11. Despite this, euro area sovereign interest rates fell from the levels reached at the end of April, and risk premiums narrowed, particularly that of Italy, which has shown the most sensitivity to news regarding the conflict.

Japan is once again under the spotlight

Japan is once again under the spotlight, after the Japanese Ministry of Finance intervened in the yen when the USD/JPY exchange rate hit the 160 mark at the end of last month. Since then, the currency has shown the same pattern as in previous episodes: a gradual depreciation indicating a structural weakness. Markets are factoring in a couple of interest rate hikes by the Bank of Japan, something they had already priced in prior to the start of the conflict in the Middle East. The first hike is expected to occur at the next meeting, also scheduled for June. In the United Kingdom, investors were torn between the possibility of a tightening of monetary policy due to rising inflation and the deteriorating economic outlook, with the labour market experiencing unemployment rates of around 5%, levels not seen since the COVID crisis. In May, financial markets were anticipating two interest rate hikes by the Bank of England (BoE), compared to the three expected a month ago, while the consensus among analysts was that the BoE would keep rates stable for the remainder of the year. Norges Bank in Norway was ahead of other banks and raised the interest rate by 25 bps to 4.25%.