The macro-financial environment behind the economic outlook

The risk map is demanding and, in addition to the prevalence of geopolitical disruptions, the financial markets have shown sensitivity to the promises, doubts and transformations of artificial intelligence (AI) and to the sustainability of public debt.

The economic outlook for the coming quarters rests on the path for financial conditions.1 The environment is supported by a stable and neutral monetary policy, which neither stimulates nor cools the economy, and a dollar that maintains the relative weakness observed in 2025. Additionally, energy prices benefit from a buffer of surplus supply and stockpiling inherited from 2025, which mitigates geopolitical pressures. However, the risk map is demanding and, in addition to the prevalence of geopolitical disruptions, the financial markets have shown sensitivity to the promises, doubts and transformations of artificial intelligence (AI) and to the sustainability of public debt. The escalation of the conflict in the Middle East, with attacks between the US, Israel and Iran, heightens uncertainty and downside risks, as we discuss at the end of this article.

- 1

See the Focuses «What to expect from the international economy in 2026» and «The Spanish economy in 2026» in this same report.

Monetary policy and interest rates

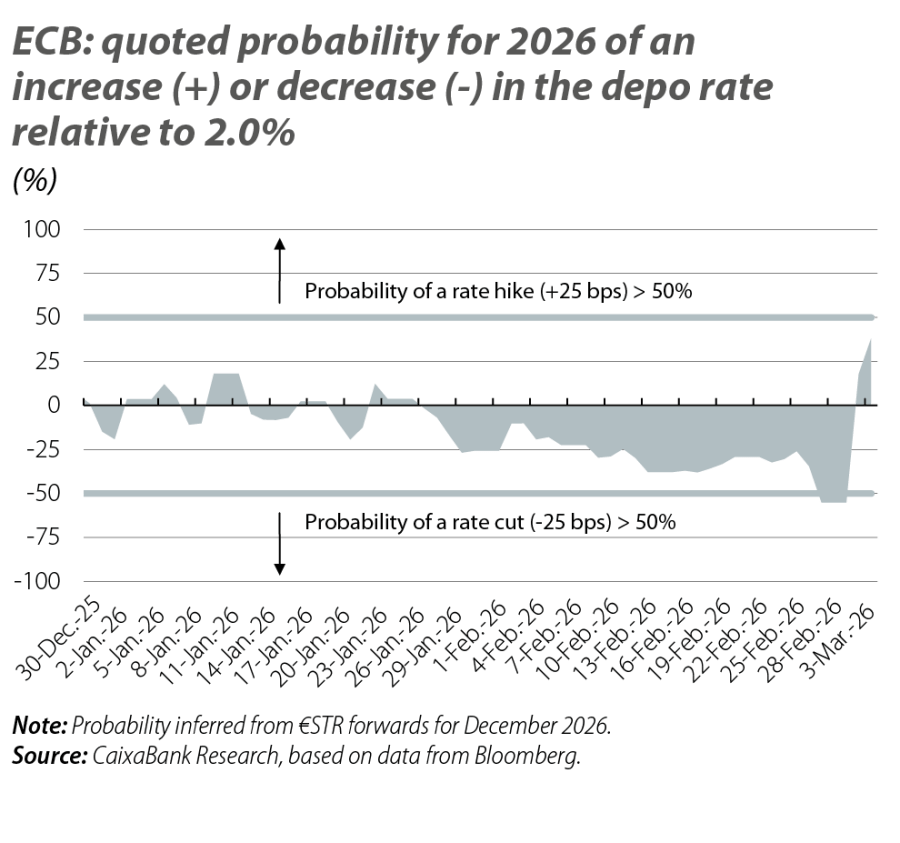

The monetary policy of the ECB and the Fed is one of the anchors of the scenario. The euro area has on-target inflation and a multi-directional balance of risks – from supply disruptions (global supply chains, extreme weather events, energy prices) to trade tensions and China’s redirection of exports towards the EU. Thus, the ECB has chosen to keep its powder dry and frequently reassess the scenario, maintaining a stable policy while the risks do not tip the economy one way or the other. Our forecasts are based on a depo rate of 2.00% in the coming quarters. This is the same rate as was being priced in by the financial markets until the escalation of the conflict in Iran triggered a shift in sentiment (see first chart).

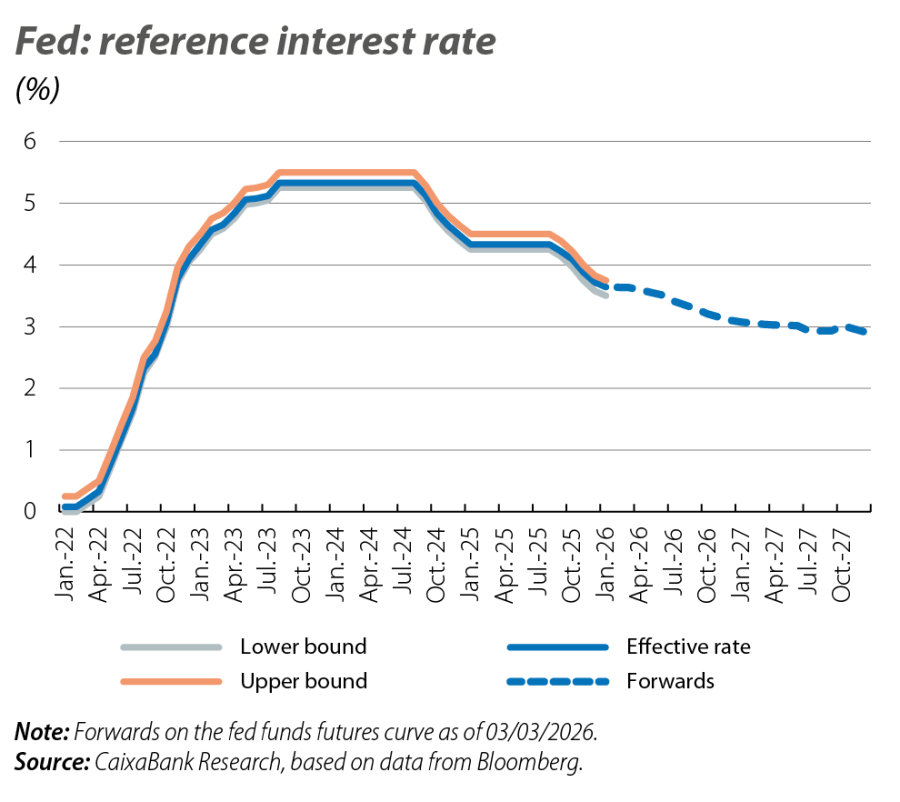

In the US, the narrative is different, but the result is relatively similar: the gradual cooling of the labour market and the moderation of inflation at the end of 2025 provide room for some additional cuts, although the robustness of growth suggests that the Fed is nearing the end of the rate-cutting cycle. Our forecast scenario foresees two more cuts, bringing the fed funds rate to the range of 3.00%-3.25%, a level that is consistent with more neutral monetary conditions. This assessment is shared by market pricing (see second chart).

In parallel, 2026 will also be a significant year on the institutional front. Jerome Powell’s term as Fed chair ends in May and his replacement has been overshadowed by the Trump administration’s pressure to lower interest rates.2 The designated successor, Kevin Warsh, has a solid profile (he was a Fed governor from 2006 to 2011) but an erratic record in his monetary policy preferences.Additionally, Governor Lisa Cook is awaiting the Supreme Court’s ruling on her attempted dismissal by the administration. On a very different level, the changeover to the presidency of the ECB is scheduled for 2027, while in 2026 the most significant end of term is that of Vice-President Luis de Guindos (ending in May) and his successor will be the current governor of the central bank of Croatia, Boris Vujčić.

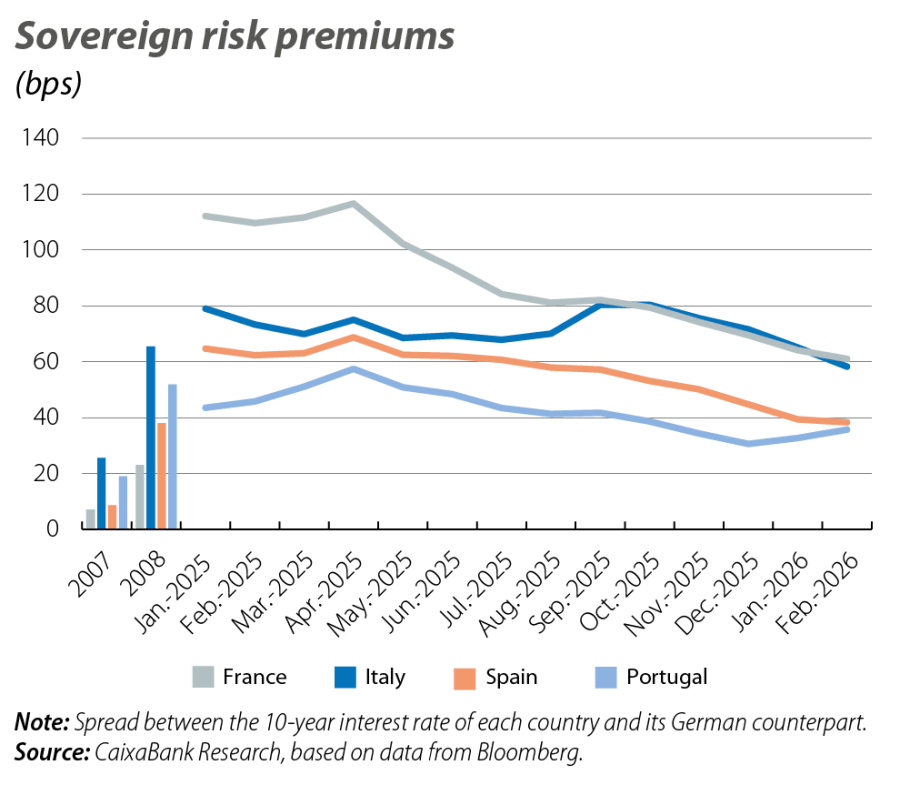

On the other hand, in the euro area, it is worth noting that sovereign risk premiums are at their lowest levels in almost 20 years (with the exception of France; see third chart). This moderation has been accompanied by an improvement in the macroeconomic fundamentals, which supports the continuation of investor sentiment being comparatively favourable for the periphery.3

- 2

Some fears were alleviated when, in December, the Fed approved the reappointment of 11 of the 12 regional Federal Reserve presidents (the exception, at the Atlanta Fed, reflects the retirement of the current president).

- 3

See the Focus «Risk premiums and macroeconomics: a robust and cross-cutting relationship» in the MR02/2026.

Exchange rate and commodities

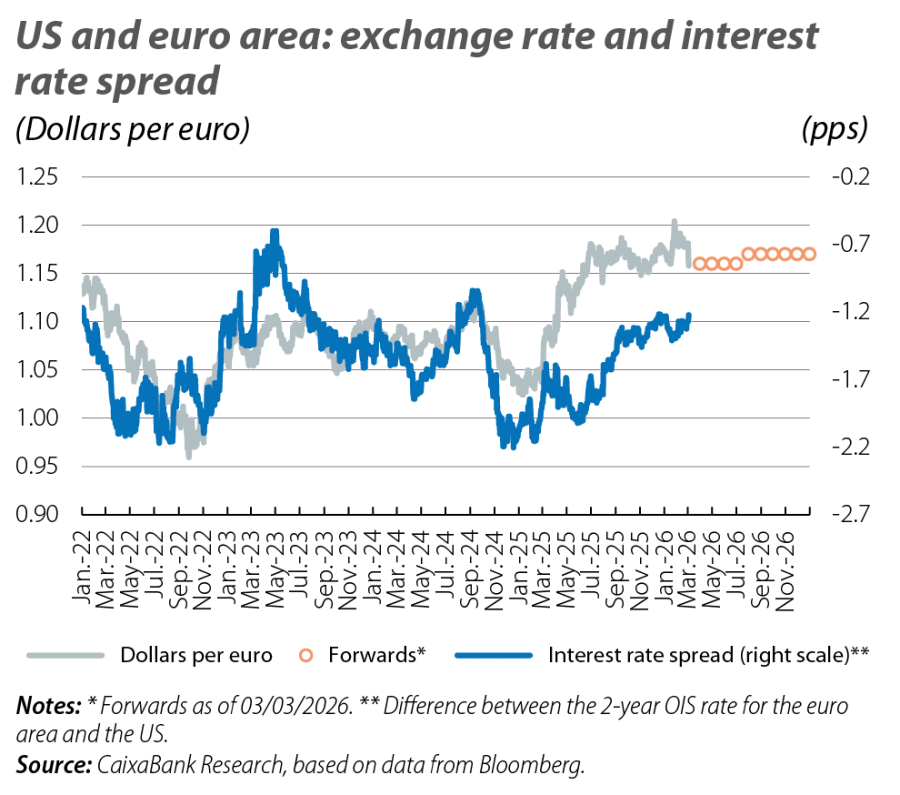

The narrowing of interest rate spreads between the euro area and the US, the expectation of a certain revitalisation of European growth and the perception of improved sentiment towards Europe support the continuation of a somewhat stronger euro/dollar exchange rate than the 2022-2024 average,4 as indicated by the markets.

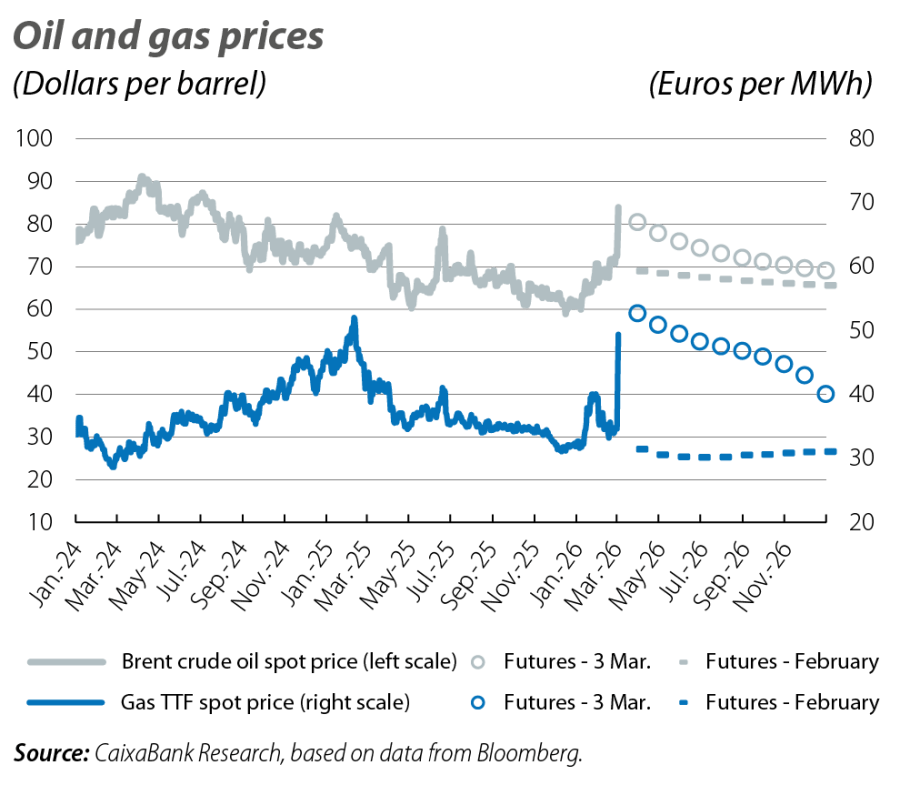

The outlook for energy prices has become more uncertain since the escalation of the conflict between Iran, Israel and the US (see fifth chart). In the background, the oil and gas markets had containment forces due to an abundance of supply, which in recent quarters has led to the accumulation of an inventory buffer that helps mitigate the impact of geopolitical shocks.

- 4

The gap that has opened up between the actual EUR/USD exchange rate and that predicted by interest-rate differentials is an indication of relatively favourable sentiment towards Europe. The depreciation is more significant if one considers that, according to conventional prediction, the dollar should have appreciated in response to an increase in tariffs (see fourth chart and Ostry et al. (2025), «Trading blows: The exchange-rate response to tariffs and retaliations», Bank of England, Staff Working Paper.

Risks

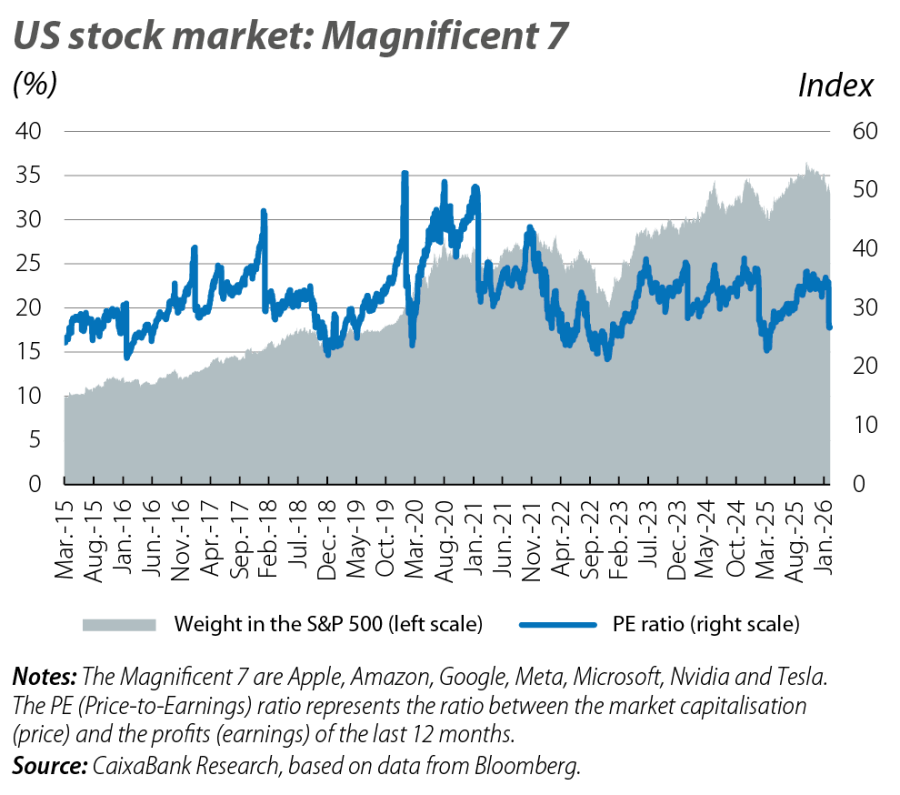

This environment outlines financial conditions with a stability that should not be unfavourable for economic performance. However, the perception of risk continues to manifest episodically in the markets. Geopolitical conflicts remain at the forefront as a source of supply-side disruptions. In early March, oil and gas came under severe stress following attacks involving Iran, the US and Israel, with futures – amid high volatility – pointing to prices for 2026 as a whole significantly higher than those quoted in mid-February. Two additional features stood out: (i) futures prices anticipated some easing over the following quarters, and (ii) they fluctuated with considerable volatility (for oil, futures for 2026 as a whole swung between increases of 10% and 25%, and between 30% and 70% for gas). If the path reflected in these futures persists then the outlook for international economic activity would lose some momentum. However, with the support of the accumulated global energy stocks and anchored inflation expectations, the outlook ought not to suffer any profound change nor will it necessarily substantially alter monetary policy strategies, which are generally starting from neutral or slightly restrictive levels. A scenario with persistently higher energy prices would raise the risk of more significant disruptions, deeper tensions in financial markets and indirect effects on inflation, and could spur a more pronounced hawkish shift in monetary policy. On the other hand, in the risk map, it is important not to overlook the importance of monitoring public debt dynamics in several advanced economies (the United Kingdom, France, Japan, and even the US have experienced some turbulence in their long-term interest rates) nor the financial risks surrounding AI, both in terms of its ability to meet expectations and its potential to disrupt established economic structures, in a context of high valuations and significant stock market concentration (see last chart).