The big data dependence of the markets and monetary policy

December 20th, 2022

In 2022, the central banks have implemented aggressive interest rate hikes in a pattern not seen since the 1980s. More stealthily, another monetary policy tool has had an equally virulent impact on the financial markets: communication. We only have to go back to 10 November 2022. At that session, the 10-year US sovereign interest rate collapsed by 30 bps, marking its biggest daily decline since 2009 and the second sharpest in the last 35 years. The cause, a seemingly harmless surprise: the US inflation figure for October, at a high 7.9% year-on-year, was 2 percentage points lower than expected by the analyst consensus. Those 2 percentage points, however small, reverberated through the international financial markets.1 After all, given the uncertainty in the current economic environment and the reorientation in central banks’ communication tools, investors are hungry for information that can help them get a sense of what monetary policy might do next.

- 1. There was a high degree of contagion to the interest rates of other countries. For example, in Germany the 10-year sovereign rate fell by more than 15 bps, while Spain’s rate dropped by 20 bps and Italy’s collapsed by almost 30 bps.

Monetary policy communication: a tool being reoriented

This communicative reorientation has gone through three phases. At the end of 2021, the central banks were still giving fairly explicit messages about what path interest rates would take, and they did so in both the short and the long term. At the beginning of 2022, under pressure due to the persistence and intensity of the inflation rally, they became explicit about their intention to aggressively raise interest rates at their upcoming meetings. Finally, in recent months, the explicitness has once again waned: the latest messages continue to point towards further rate hikes, but highlight the uncertainty of the environment and advocate a more flexible approach to decision-making.

As an example, in late 2021, the US Fed stated that it was appropriate to maintain a dovish monetary policy until the labour market reached full employment and inflation was slightly above 2%, exceeding this level for quite some time. In Europe, the ECB adopted a similar strategy: it would keep rates at historical lows until 2% inflation was projected on a sustained basis (which, according to market rate expectations, would still take 1 to 2 years to occur). In 2022, they quickly changed course, but the message on rates remained relatively explicit: the Fed raised rates in March and declared that it would continue to do so over the coming months, while the ECB began to signal the same message between June and July. Thus, they will have ended 2022 with cumulative increases of more than 400 and 200 bps, respectively. At this point, both institutions are still indicating that further rate hikes lie ahead, but that automatic pilot has been disengaged and decisions will be taken «meeting by meeting» and be «data-dependent».

All this results in less predictability – an approach that is necessary for monetary policy to respond quickly and appropriately to developments in the economic environment, but which accentuates uncertainty and helps to explain the heightened volatility in market interest rates (see first chart).2,3

- 2. Relative measures of volatility (i.e. taking into account the starting level of interest rates) have also settled in 2022 at above pre-pandemic levels (e.g. the coefficient for the fluctuation of the US rate is 90% higher than the average for the period 2017-2019).

- 3. Relative measures of volatility (i.e. taking into account the starting level of interest rates) have also settled in 2022 at above pre-pandemic levels (e.g. the coefficient for the fluctuation of the US rate is 90% higher than the average for the period 2017-2019).

Market sensitivity

The Fed and ECB are putting the evolution of the data at the forefront of their upcoming decisions, especially developments in inflation – hence the market’s hypersensitivity on 10 November. But this sensitivity is not a one-day anecdote: it has steadily increased throughout 2022.

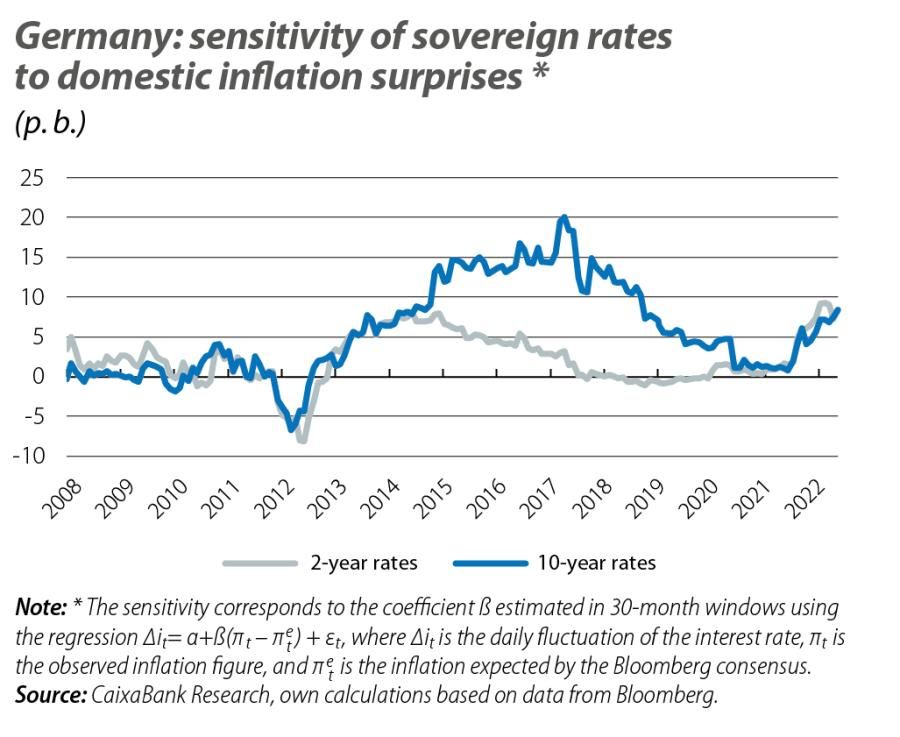

As we see in the second and third charts, the interest rates on 2- and 10-year debt in recent months have become more reactive to inflation surprises in both Germany and, above all, the US.4 Also, as the fourth chart shows, the sensitivity of German interest rates to surprises in the US inflation data has also been increasing, showing what appears to be a stronger correlation between the US treasury and the German bund.5 One consequence of this volatility in rates is that caution must be exercised when trying to infer market expectations on the basis of prices in the financial markets: beyond monetary policy expectations, these interest rates are likely to incorporate risk premia due to the uncertainty regarding the current environment.

- 4. In these exercises, the estimated sensitivity corresponds to the coefficient β of the regression Δit = α + β(πt – πet ) + εt, where Δit indicates the change in the interest rate on the sovereign bond (US and German 2- and 10-year bonds) on the day the inflation data is published, πt is the observed inflation (the flash indicator in the case of Germany) and πet is the inflation expected by the Bloomberg consensus. We estimate the regression using data from the 30 months prior to t and we show the value of the parameter β over time.

- 5. One possible interpretation of this stronger correlation is that the markets read the US signals as clues about the future of Europe.

Similarly, in the last chart we can also see how the sensitivity of other types of assets in 2022 has been very different to the average observed in other periods. Particularly pronounced is the change in the sensitivity of the US stock market to inflation surprises: not only has it increased (in absolute terms), but it has also changed sign. One possible explanation for this shift is that, whereas inflation above the consensus expectation in the period 2016-2021 could signal a more dynamic economy, and thus a better outlook for corporate earnings, a similar surprise today implies the expectation of a more restrictive monetary policy, with the associated negative impact on growth and stock-market performance.6 On the other hand, the negative sensitivity of the exchange rate is consistent with the fact that higher-than-expected inflation causes the dollar to appreciate due to the expectation of rate hikes in the US.

- 6. As for sovereign risk premia, in 2016-2021 they tended to narrow in response to higher-than-expected inflation, while in 2022 no significant response is apparent.

Finally, it is important to note that surprises in the inflation statistics impact short-term inflation expectations (identified in this case by inflation swaps for the next two years), while they do not appear to have any significant impact on medium- and long-term expectations (identified by the 5-year, 5-year inflation swap). This shows that, despite an exceptional economic and financial environment and high inflation, the central banks are managing to uphold their credibility and keep inflation expectations close to the 2% target.

Hot Topics

Macrofinance

What factors will determine the evolution of interest rates, investment sentiment and macro-financial conditions in general?