Quo vadis, globalisation? (part II): the fragmentation of the global economy

In this second article on globalisation, we analyse the growing fragmentation of the world economy in recent times, focusing on the decoupling between the US and China, and its effects.

October 17th, 2023

Trade globalisation has shown great resilience following the COVID crisis and through to 2022, within the context of an underlying long-term slowdown. As we discussed in the previous Focus, this slowdown can be explained as the logical maturation of a long process involving the opening up of markets, as well as being affected by a tightening of financial conditions. Both of these trends would dismiss the thesis that we could see deglobalisation occur at the root level. In this second Focus, we analyse the evidence from recent months which, although still partial and indicative, is nonetheless relevant as it affects the main economies. Specifically, this evidence points to a growing fragmentation of globalisation, which could have wide-ranging consequences.

The successful decoupling of the US from China

Despite not making as many headlines as in the past, the US-China trade war persists, as evidenced by the high tariffs that both economies continue to impose on their counterpart.1 In addition, all the indicators suggest that the US’ decoupling-from-China policy is achieving its goals, reducing the trade deficit with China in terms of GDP while reducing the Asian country’s market share in US imports in favour of the US’ main trading partners, particularly Mexico.

- 1. See C.P. Bown and M. Kolb (2023). «Trump’s Trade War Timeline: An up-to-date guide. Peterson Institute for International Economics».

Moreover, there does not appear to be a diversion of trade flows, as there are no major signs of Chinese exports seeking alternative routes or of Chinese firms relocating in order to circumvent the tariffs. Whereas the value of Chinese products being imported by the likes of India or Vietnam has increased by more than these countries’ exports to the US, this is not the case for Mexico, Canada, Taiwan or the euro area. In terms of FDI, Chinese investment volumes in these economies have also not yet reached the levels of those trading partners with whom they have more in common.

On the other hand, not only does it appear that the US is switching suppliers but, as several recent studies point out, the country is also managing to relocate part of its production processes previously located in China to more like-minded partners, such as Mexico or Vietnam, or even to the US itself.2

- 2. See L. Alfaro and D. Chor (2023). «Global Supply Chains: The Looming «Great Reallocation»». National Bureau of Economic Research, nº w31661.

A process with little impact on both economies

Given that both of the US’ two main political parties share the goal of decoupling with China, we can expect this process to continue and for the trend of fragmentation in the global economy to increase. Moreover, to date this decoupling process is not damaging US economic growth, nor that of its exporters, which have not lost their share in global trade, unlike the Germans or the Japanese.

On the other hand, China has lost global market share since the rebound it experienced in the first year of the pandemic, although it still exceeds the level it held in 2018 and we will have to wait a little while to see the impact of its post-COVID reopening process. The country has avoided a greater impact of the trade war with the US, replacing the US market with the European one. In fact, relative to GDP, as the US was limiting its exposure to China, the EU’s exposure only increased, at least up until the end of last year. While it is true that the EU has suffered a slower post-pandemic recovery in GDP than the US, which could be distorting this trend, the fact is that China is becoming increasingly able to export high value-added products to the EU (e.g. electric vehicles).

Another derivative of the US-China decoupling process which is threatening the health of further globalisation is the aggressive industrial and subsidies policies of both countries, which could alter the conditions for competition with industry in the rest of the world.

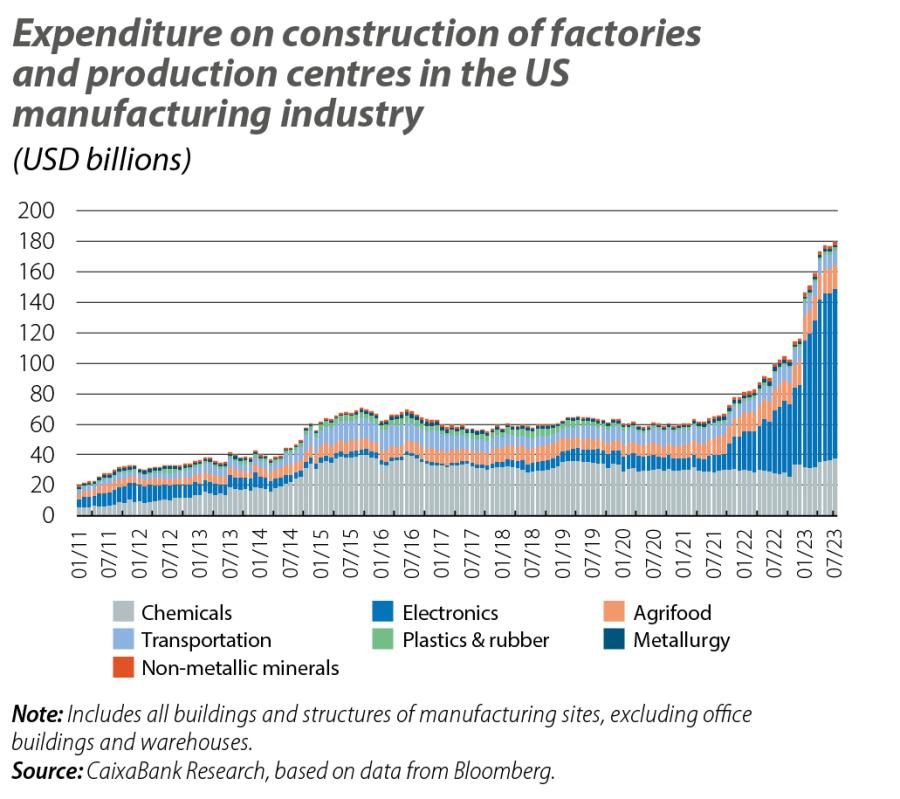

In the case of the US, the major public stimulus packages aimed at boosting green and digital industries3 are triggering a sharp increase in investment in manufacturing which, even relative to GDP, is as high as anything seen in the past two decades. This uptick in investment is being directed towards the construction of new factories in the electronics industry, which ought to favour sustained productivity growth over the coming years.

- 3. Channelled in three large packages: the Inflation Reduction Act, the Chips and Science Act and the Infrastructure Investment and Jobs Act.

In the case of China, the country’s industrial policy is focusing on boosting the production of electric vehicles, which is allowing it to gain significant market share in Europe. This is already causing trade tensions, and in fact the European Commission has just announced that it will open an investigation into public subsidies which electric vehicle manufacturers in China may be receiving and which could be distorting the EU market. If so, the EU could impose higher tariffs (currently at 10%) on Chinese vehicles, demonstrating the risks which the uncoordinated use of public subsidies for industrial development pose to globalisation (among other problems).

While the aggregate data for global trade are not yet showing signs of any radical deglobalisation, but rather a gradual slowdown due to the process of the opening up of markets running out of steam, there is nonetheless increasing evidence of a growing fragmentation of the world economy in recent quarters. Although this fragmentation could end up having beneficial effects for some of the world’s regions that have been less involved in globalisation to date, such as Latin America, thus avoiding a significant drop in the aggregate trade data, its effect is yet to be fully felt. What seems clear is that globalisation is mutating. Trade in manufacturing goods will not continue to expand in the regions where it did over the past 30 years, although the trade in services could still expand significantly. At least, it could do so if the global market remains relatively unified and connected – an assumption which an increasing number of indicators are calling into question.

Hot Topics

Geopolitics

We analyse the major geopolitical trends and how they influence the financial markets and economy.